This is a segment of the 0xResearch newsletter. Subscribe to read the full edition.

When you ask the average crypto person what problems the industry is facing today, it quickly shows up as a general complaint, saying, “Too many chains, lack of apps.”

This complaint is impressive alongside the early Internet era.

During the dot-com boom of the late 90s and early 2000s, skeptics likewise criticized overinvestment of excess infrastructure, particularly in fiber optics.

Telecommunications companies (Global Crossing, Worldcom, AT&T) have spent billions of dollars laying submarine cables and long-range fiber networks based on the belief that internet traffic will grow exponentially.

Even internet pioneers criticized Bob Metcalf for this perceived overinvestment, claiming that there was simply not enough demand.

In the luxuries of hindsight, we now know that Metcalf was wrong (Metcalf literally ate his words in 2006 after he admitted his mistake).

The explosive surplus of bandwidth makes amazing products like YouTube, cloud computing, Netflix and more possible today.

Netflix, for example, was a mail-based DVD rental business for many years before it slowly began its transition to streaming in 2007.

In short, the bet that “we build it, demand comes” ultimately proved true for the internet, but it took ten years, but it required bankruptcy for internet infrastructure companies like Global Crossing.

Ethereum is now chipping on similar bets.

With each rollup-centered roadmap, today’s Ethereum L1 actually gives up the running fee for the L2S.

However, Ethereum plans to benefit from data availability (DA) fees through future upgrades to ultimately expand its DA supply. The idea is that Ethereum DA will eventually become very abundant and induce ultimate user demand.

Just like early Internet builders, Ethereum researcher Justin Drake believes, “If we build it, there will be demand.”

Drake’s Moonshot mathematics looks like this: At 10 million TP, each transaction pays Ethereum $0.001 in DA fee, making it $1 billion per day for Ethereum.

(This assumes that L2 uses Ethereum L1 for the DA, as opposed to alternative DA layers such as Celestia and Eigenlayer.

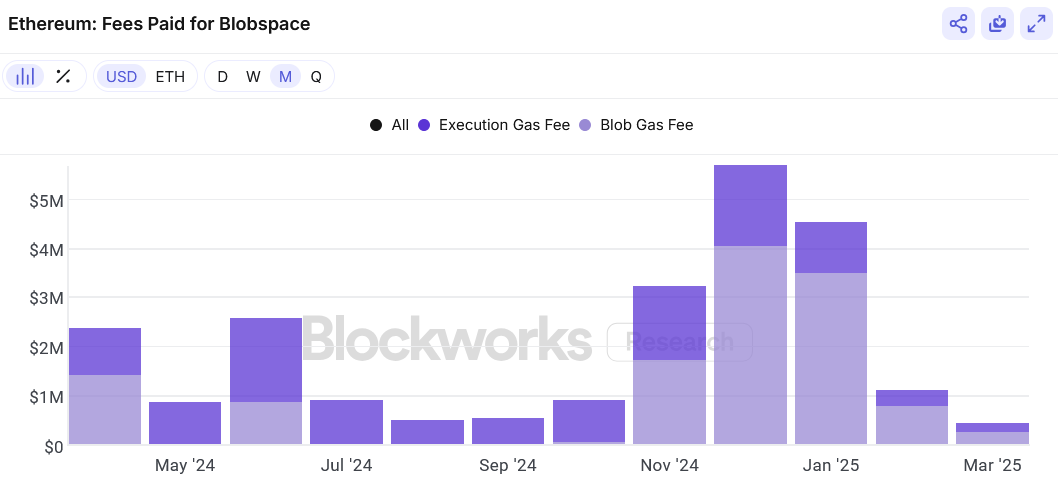

Considering today’s DA consumption, it’s a bold paper. Ethereum’s Blob gas fee reached just $272,000 in March.

Ethereum Bulls may believe that Web3 will revive just like Web2’s history, but Ethereum does not exist in the silo and faces tough competition from other chains.

Also, there is little speculation yet about the type of on-chain application that governs blockchain use. It is necessary in the world that What is the availability of a lot of data?

But I’m off track. The claim that “too many chains” may ultimately be true. But it was in the early days of the Internet, so it’s too early to tell it.

If true, the market will help to curb wasteful spending even more. Suitable Case: L1 Premium is rapidly compressed.

The L1’s $300 million increase from $500 million has ended. The L1/L2 blockchain in 2024 ranged from $14 million (early) to $100 million (belachine) and $225 million (Monad).