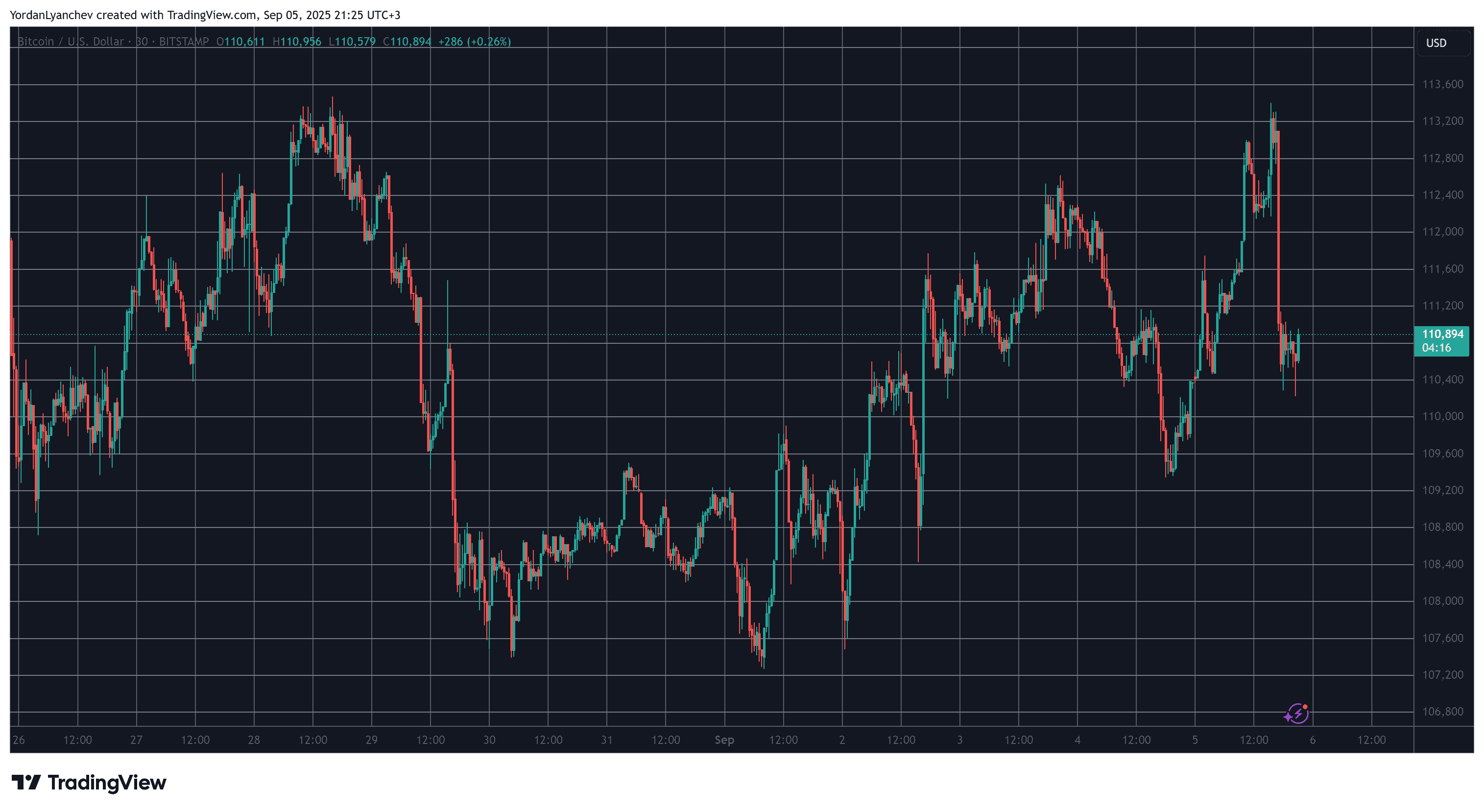

The gradually price recovery of Bitcoin, which peaked assets every week earlier today, was the end of a screeching as the assets were heavily rejected on that line.

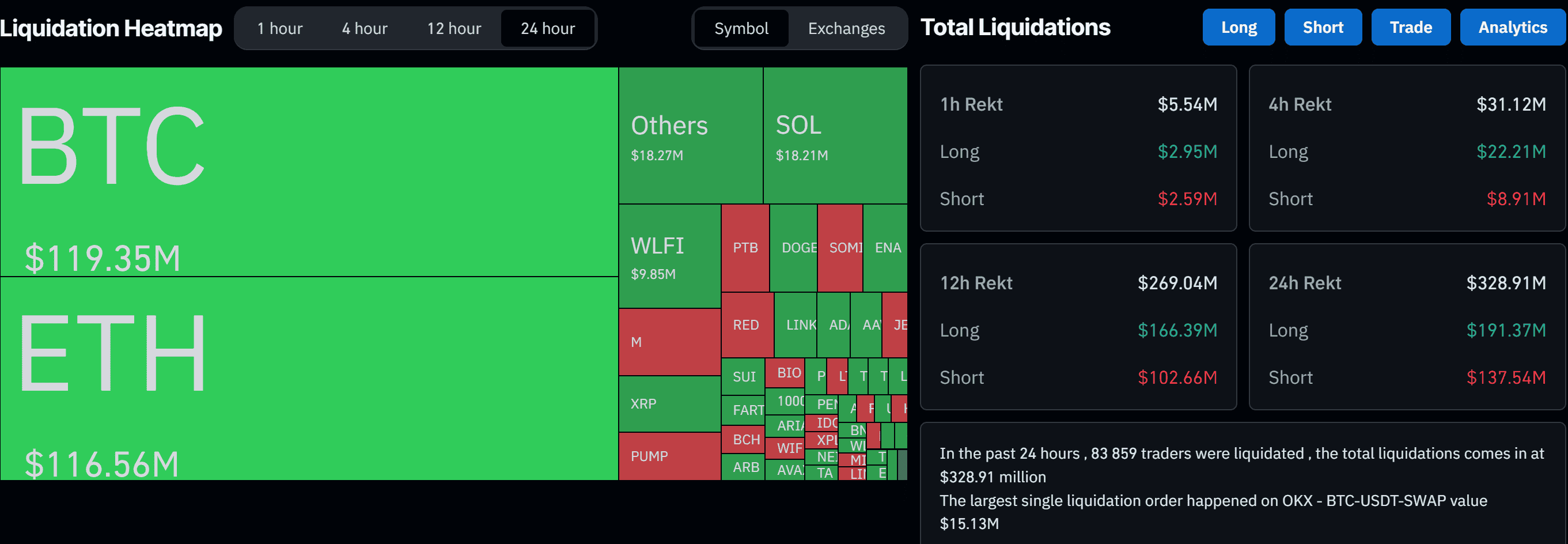

Altcoins followed suits that have destroyed past traders, with over 80,000 such market participants being liquidated in the past day.

Major cryptocurrencies have had tough weeks, and their prices have dropped to $107,000 on several occasions, but the Bulls were ultimately able to defend their vital support. Additionally, they reversed the trajectory of BTC over the past few days, reaching price pumps of $113,500 per week earlier today.

This impressive increase came after the latest US Employment Report. This showed that the US economy could be in a much tougher state than many believe.

This was seen as the bullish development of high-risk assets like BTC. This is because the FOMC meeting in September suggested that the US Federal Reserve could put pressure on further lowering interest rates.

But that’s because Bitcoin’s rise halted, assets were rejected there, pushing three or more grounds south within an hour. Many Altcoins mimicked the BTC’s dive, dropping from their daily highs, including ETH.

Coinglass data shows that this volatility has undermined over 83,000 traders who have been destroyed in the last 24 hours. One biggest wipeout position was made on OKX, worth over $15 million.

The total liquidation amount rose to $330 million on a daily basis. It follows BTC length of $119 million and ETH $116 million.