U.S. mortgage lender Rate has launched a nationwide program that allows eligible borrowers to use verified cryptocurrency holdings to meet underwriting requirements without liquidating assets, marking a formal step toward integrating digital assets into traditional home financing.

The product, called RateFi, will work within the framework of lenders’ existing non-conforming mortgages, allowing borrowers to count verified crypto assets as qualifying reserves and, in some cases, as a source of income.

Kate Amor, EVP and Head of Enterprise Products at Rate, told Cointelegraph that for underwriting purposes, RateFi values digital asset holdings through a proprietary valuation framework that takes into account market price, liquidity, and asset-specific volatility. This approach allows us to consider borrower eligibility without liquidating specific crypto assets while applying traditional mortgage risk criteria.

However, digital assets used for down payments or closing costs still need to be converted into cash.

The company said the rollout comes as more than 10% of Americans report holding digital assets, but most traditional mortgage programs do not accept cryptocurrencies as eligible collateral unless they are first liquidated.

The liquidation or sale of assets often triggers taxable events and other tax consequences, and limits borrowers to asset-backed loan structures.

Amor said RateFi is designed to work with a select set of established, liquid, large-cap cryptocurrencies and major USD-backed stablecoins, but did not reveal the specific assets supported.

Eligible crypto assets must be stored at an approved custodian or centralized exchange, and the borrower must provide proof of ownership and asset seasoning, typically through monthly statements.

Amor told Cointelegraph that pressure on housing affordability is a key factor driving interest in crypto-enabled housing finance solutions. she said:

Younger generations are in their peak homebuying years, making traditional paths to ownership increasingly unaffordable, but they are also the most active participants in the digital asset economy.

He added that the program is “about recognizing how wealth is actually built today and modernizing access to homeownership accordingly, not promoting cryptocurrencies for their own sake. For many young Americans, cryptocurrencies have become a cornerstone of their financial planning.”

Lehto said the program applies standard anti-money laundering (AML) and know-your-customer (KYC) certifications and is available through existing digital mortgage platforms.

Related: Bitcoin-backed home loans emerge in Australia amid housing crisis

Cryptoassets face US housing price crisis

Affordable housing remains a major economic challenge for the United States, especially for young Americans, and has received increasing attention from the Trump administration and lawmakers in recent months.

In the absence of legislation to open crypto-backed mortgage lending to the broader U.S. market, policymakers are beginning to consider how digital assets can be incorporated into the housing finance framework.

In June 2025, Federal Housing Finance Agency Administrator William J. Pruitt directed government-backed mortgage purchasers Fannie Mae and Freddie Mac to draft a proposal to treat virtual currency as a reserve asset in the risk assessment of single-family mortgages.

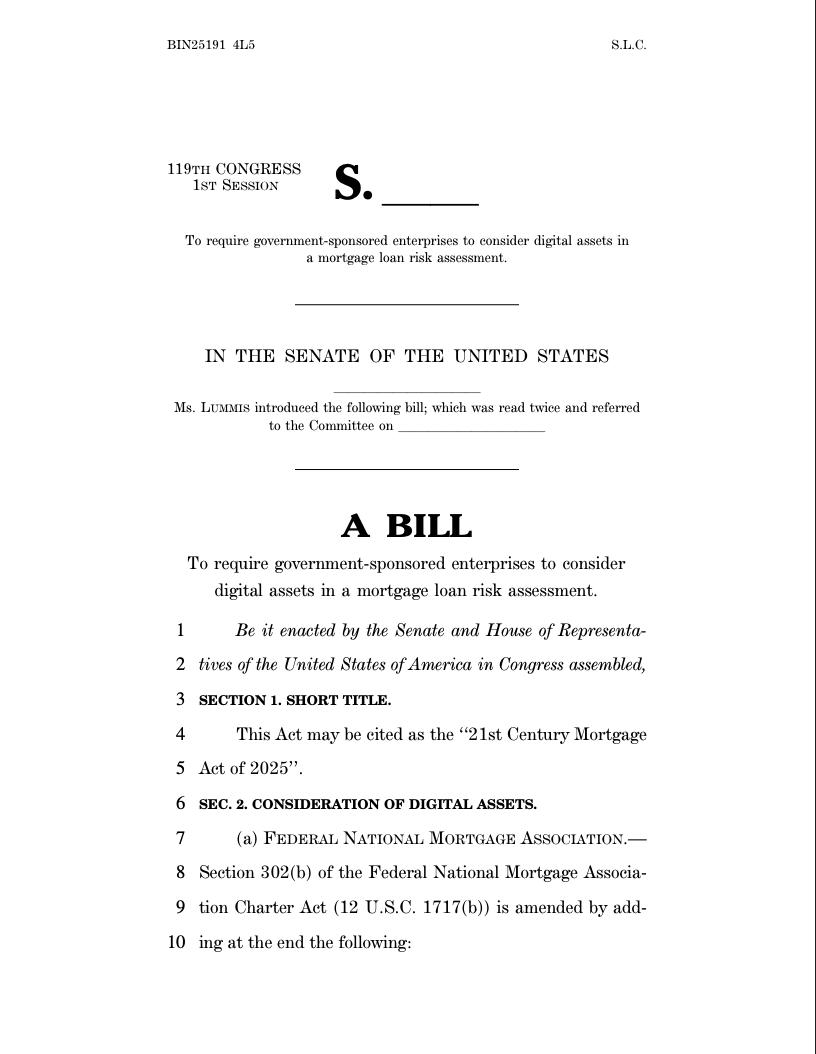

In July, Sen. Cynthia Lummis introduced the 21st Century Mortgage Act to codify that directive.

Mortgage law in the 21st century. sauce: Senator Cynthia Lummis

A niche market for crypto-backed real estate loans already exists. While lenders such as Nexo offer loans backed by more than 40 digital assets, Ledn offers a Bitcoin-backed mortgage product that allows borrowers to pledge Bitcoin (BTC) as collateral.

A January survey of 1,000 Americans published in the OKX Insights series found a significant generational gap in attitudes toward digital assets, with younger respondents far more likely to believe that cryptocurrencies are trustworthy and central to the future of finance.

magazine: Cliff bought two homes with Bitcoin mortgages. Clever…or insane?