Record $409 million in one day shows how the strategy is rapidly expanding its Bitcoin accumulation with STRC

March 10th, Strategies Floating Rate Series A Preferred ($STRC) conducted its most significant trading session since its launch.

The heading numbers are:

- $409 million in daily trading volume – record high

- 30-day volatility 3% — lowest since issuance

- 1 Month VWAP of $99.78 — Highest Recurring Average Ever

Record date of $STRC.

$409 million – daily trading volume (highest ever)

3% – 30D volatility (lowest in history)

$99.78 – 1 million VWAP (highest ever) pic.twitter.com/UuQJvU17I1— Strategy (@Strategy) March 10, 2026

At first glance, these appear to be milestones that new financial products pass as they mature. The market discovers the product, liquidity increases, volatility compresses, and price action begins to stabilize.

But taken together, the data suggest that something more interesting may be going on.

The STRC is beginning to behave more like a capital market instrument with real institutional liquidity than a financial experiment.

The difference is important for executives who are closely monitoring the evolution of their companies’ Bitcoin strategies. The conversation gradually shifts from one thing to the next. Should companies own Bitcoin? To something more structural: How capital markets are beginning to organize around it.

STRC occupies an unusual position within Strategy’s capital structure, acting as the connective tissue between two financial ecosystems that rarely overlap comfortably.

On one side sits traditional income investors. Income-oriented allocators who prefer pension funds, insurance portfolios, stable products, predictable distributions, and securities that behave in a reasonably orderly manner.

On the other side is Strategy, Inc. (MSTR), whose balance sheet is heavily concentrated in Bitcoin, an asset notorious for its long-term asymmetry and equally famous for its short-term volatility.

Reconciling these two realities requires more than simply issuing preferred stock.

STRC is configured as follows: Floating Rate Series A Perpetual Preferred Stockdesigned for close trading. $100 per value while paying Current monthly dividend yield is approximately 11.5% per year. Dividend rates can be adjusted periodically to maintain demand and keep securities near par.

In reality, this device performs a translation function. This translates the economics of a Bitcoin-centric balance sheet into a structure that traditional debt capital can value without directly considering Bitcoin volatility.

Financial markets tend to reward this type of translation layer. When two large pools of capital speak different languages, bridging institutions often end up controlling the flow between them.

The most revealing statistic from the March 10 trade was not just the volume, but what the strategy was able to do with its liquidity.

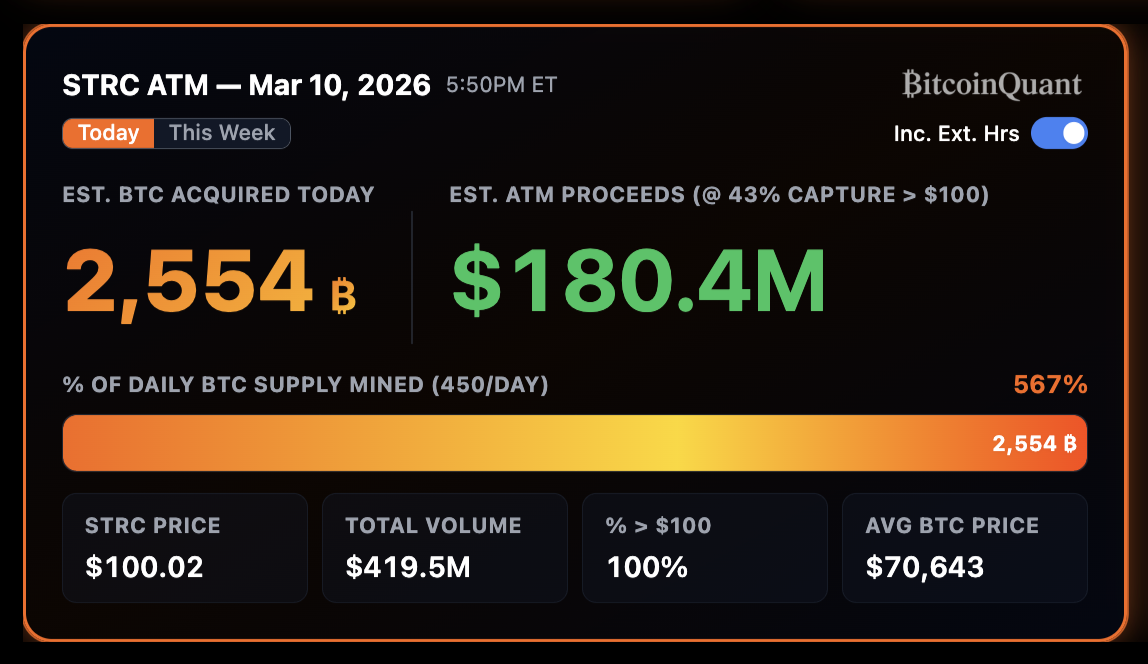

Source: BitcoinQuant.co

Based on available estimates, trading activity for the day was approximately ATM revenue was $180.4 million.capital that can eventually be put into purchasing additional Bitcoins. At prevailing market prices, that capital is approximately equivalent to: 2,554 $BTC obtained.

To understand the significance of this number, it helps to consider Bitcoin’s supply mechanism. The world’s mining industry is currently approx. 450 $BTC per day.

In other words, the capital formation generated through STRC trading activity during a single session is roughly represented. 567% of Bitcoin supply newly mined daily.

This highlights the structural asymmetry at the heart of Bitcoin and capital market interactions. The supply of Bitcoin expands according to a fixed schedule governed by code. In contrast, capital market demand expands in response to financial innovation and investors’ willingness to allocate capital to new products.

Even when these two systems match up, the supply side does not coordinate. The demand side simply scales.

Volume alone rarely tells the whole story about a financial product. A more interesting signal is often how that volume interacts with volatility.

In the case of STRC, this combination is surprising. record trading volume and Extremely low price volatility. This combination usually indicates a change in investor demographics.

Speculative trading can certainly increase volume, but it is unlikely to compress volatility. This is most likely to happen when: Income-oriented capital begins to participateA type of capital that prefers stability and locks in securities that trade infrequently and are close to their fundamental value.

STRC’s 30-day volatility has compressed to around 3% while liquidity has expanded significantly, suggesting that STRC may be accomplishing exactly what the structure was designed for. It is starting to behave more like a derivative than a highly volatile equity derivative. Profitable products with predictable price trends.

If this momentum continues, STRC could represent the early stages of something financial markets have never seen before on a large scale. Income security linked to Bitcoin with institutional liquidity.

Viewed through a different lens, STRC is beginning to exhibit characteristics that product manufacturers can readily recognize. Product-market fit.

Although this phrase is usually associated with software startups, the underlying concept applies equally to financial products. Product-market fit occurs when a product effectively solves a real demand problem and adoption begins to accelerate organically. Liquidity deepens. Price trends will be stable. The system then begins to draw capital through it, rather than relying on continued promotion.

Several signals suggest that STRC may be approaching that threshold.

Volatility continues to decline while trading volumes expand rapidly. Security remains remarkably close to target $100 per valuesuggesting that the dividend adjustment mechanism is working as designed. And perhaps most importantly, the investor base appears to be moving toward income-oriented capital, a type of capital that tends to stabilize rather than magnify market volatility.

The most obvious evidence of this dynamic came during the March 10th session.

The capital raised through the STRC transaction will be translated into estimated amounts. 2,554 $BTC obtainedequivalent to 567% of the daily global Bitcoin supply was mined.

This number is not so much about the number itself as it is about what it means. If a financial instrument can direct that level of capital to a scarce asset in a single session, it suggests that the market may have discovered a structure it actually wants to use.

In other words, the product is working.

Financial markets rarely value smart engineering alone. A structure will survive if it meets real investor demand. If STRC continues to attract liquidity while maintaining price stability, it could indicate that Strategy has identified a structure that can unite two large pools of capital: traditional income investors and Bitcoin-based corporate balance sheets.

When such a correction occurs, the market tends to extend it quickly.

For CFOs and corporate boards evaluating Bitcoin financial strategies, the importance of STRC extends beyond a single preferred security structure.

This is a glimpse into how Bitcoin will begin to restructure corporate capital structures themselves.

Traditionally, companies have raised capital through a familiar toolkit: common equity for growth investors, debt for credit markets, and preferred securities for income-oriented capital. Each component serves different classes of investors with different risk appetites.

Bitcoin treasury companies are starting to experiment with more integration.

These structures direct different forms of capital into a shared strategic reserve, rather than funding a business alone. Income investors can participate through preferred products. Equity investors may seek leveraged upside through common stock. However, the proceeds from both ultimately flow towards the same underlying asset.

Once this dynamic takes hold, Bitcoin will no longer function simply as a balance sheet holder; Assets on which the capital structure itself is organized.

The March 10 trading may ultimately be remembered as more than just a record day for a single security.

This may mark the moment Bitcoin begins to move from the fringes of corporate finance to something more structural. Reserve assets that can support entirely new types of securities.

Financial markets have always evolved through means of transforming unfamiliar ideas into familiar forms. Exchange-traded funds did that for commodities. Mortgage securities did that for real estate credit. Structured products did that for complex derivatives.

STRC is trying to do something similar in its own way.

It packages the economics of Bitcoin vaults into a format that traditional capital markets can understand, price, and trade.

Whether this model ultimately scales remains to be seen. Markets tend to test new financial structures thoroughly before making them permanent. But if liquidity deepens further and volatility remains subdued, the impact will extend far beyond a single preferred security.

What matters most is not the transaction milestone itself, but what it represents. Capital markets appear to be discovering new ways to fund Bitcoin accumulation. If this trend holds, it could reshape the way financial institutions access finite assets and deploy capital.

Disclaimer: This content was created on behalf of: Bitcoin for corporations For informational purposes only. It reflects the author’s own analysis and opinions and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to buy, sell, or subscribe to any securities or financial products.

This post first appeared in Bitcoin Magazine and was written by Nick Ward.