The stablecoin debate in Washington is becoming increasingly contested over a single issue: who gets to maintain on-chain deposit insurance.

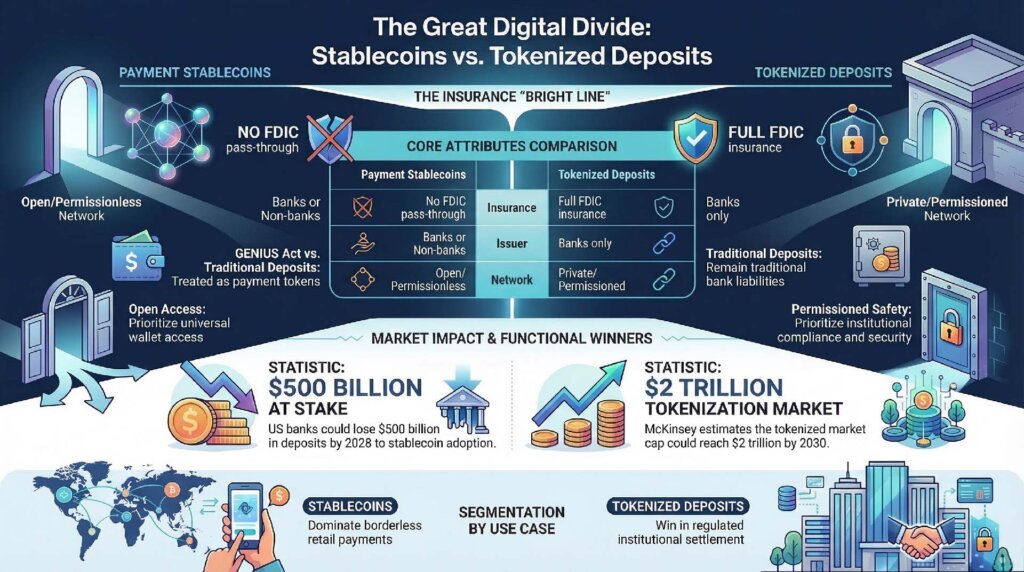

FDIC Chairman Travis Hill suggested that while payment stablecoins under the GENIUS Act should not be subject to pass-through insurance, tokenized deposits that meet the legal definition of a deposit will retain insurance treatment similar to traditional bank accounts.

The difference may be decisive.

While stablecoins cannot do that, the competitive balance changes if banks can offer on-chain dollars that maintain deposit insurance. Stablecoins may still dominate open networks, but banks will retain the core advantage that has always underpinned the financial system: insured money.

In that scenario, the stablecoin battle will no longer be just a matter of technology and distribution. The deciding factor will be whether users prefer an open, programmable dollar with no insurance, or a bank-issued token that is fully responsible for the existing safety net.

Hill said in a March 11 speech at the ABA Washington Summit that the agency plans to propose that payment stablecoins covered by the GENIUS Act be exempt from pass-through insurance.

In the same section of his speech, he said the FDIC plans to clarify that tokenized deposits that meet the statutory definition of a deposit should receive the same regulatory and deposit insurance treatment as non-tokenized deposits.

Hill also said the agency would like to comment on how existing pass-through rules should apply to tokenized deposit arrangements involving third parties.

The FDIC Chairman’s speech effectively depicts a two-tier map of on-chain dollars.

Under this map, stablecoins for payments could be regulated and widely used, but lack federal insurance distribution rights and pass-through insurance if Hill’s proposal is upheld.

On the other hand, tokenized deposits, if eligible, mean they can remain within the legal category of bank deposits and retain the core benefit of bank money: access to existing deposit insurance schemes.

The disagreement has spurred a broader legislative battle in Washington over transparency laws, with banks and crypto companies clashing over whether stablecoins should be allowed to offer yield.

Same blockchain rail but different legal realities

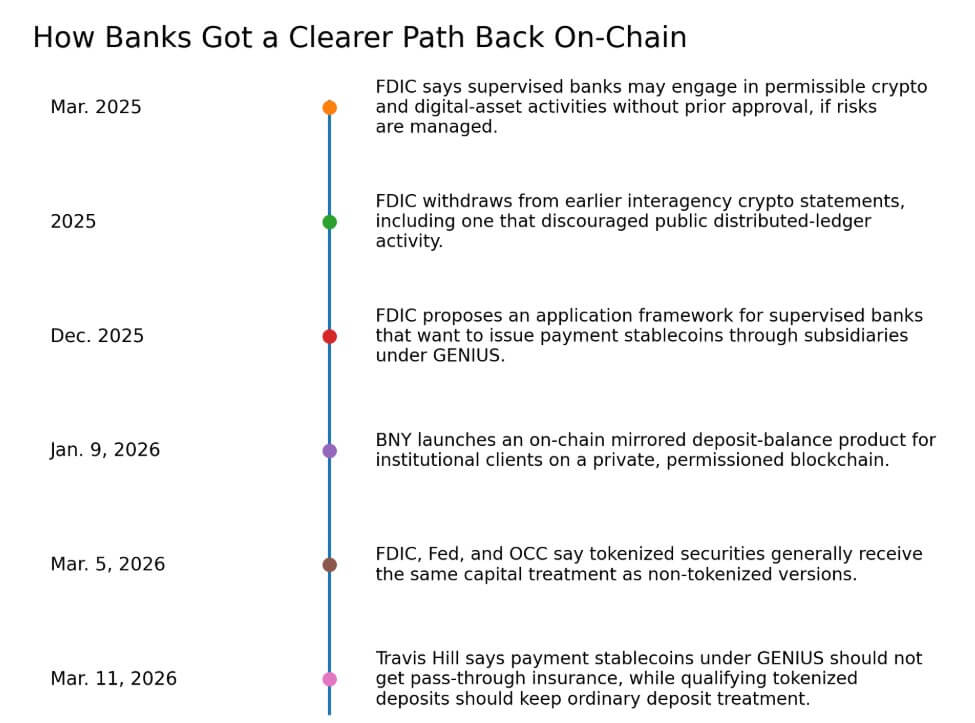

This is part of broader deregulation. In March 2025, the FDIC stated that institutions supervised by the FDIC may engage in permissible crypto- and digital asset activities without prior approval, as long as the risks are properly managed.

In 2025, the FDIC also retracted several interagency cryptographic statements, including one suggesting that public distributed ledger activities may be inconsistent with safe and sound banking practices.

Then, in December 2025, the FDIC proposed an application framework for FDIC-supervised banks that wish to issue payment stablecoins through GENIUS subsidiaries.

In March 2026, the FDIC, Federal Reserve, and OCC also clarified that tokenized securities generally receive the same capital treatment as non-tokenized securities.

Taken together, these moves provide a clearer path for banks to return to blockchain-based finance.

The US currently divides its on-chain dollars into at least two buckets.

Payment stablecoins are attractive because they are designed for payments and settlements, can be issued by banks or non-banks under GENIUS, and run on open blockchain networks.

Hill draws a clear line when it comes to insurance.

Tokenized deposits are subject to traditional deposit regulations and given a different legal basis if they meet the definition of a deposit. The competition will be stablecoins and on-chain, portable bank money.

The banking industry’s concerns are specific. A February 2026 New York Fed staff report argued that stablecoins could not only erode banks’ deposit franchises, but also transmit liquidity stress to the banking system, forcing partner banks to hold more reserves and reducing lending.

Standard Chartered estimates that if stablecoin adoption accelerates, U.S. banks could lose about $500 billion in deposits by the end of 2028.

Mr. Hill’s nice features give banks a way to compete with stablecoins in the form of on-chain money that still counts as bank funding.

What tokenized deposits look like today

BNY announced on January 9 that it has taken the first step in its strategy to tokenize deposits by allowing customers to mirror their deposit balances on-chain on its digital asset platform.

BNY also revealed what type of product this is. It runs on a private, permissioned blockchain and starts with a collateral and margin workflow use case, representing a participating customer’s existing demand deposit claims against the bank.

The likely near-term winner of tokenized deposits is institutional payments.

This development takes place within the ever-growing tokenized financial market. McKinsey predicts that tokenized market capitalization could reach around $2 trillion by 2030 in a base case, with a range of $1 trillion to $4 trillion, excluding stablecoins to avoid double counting.

McKinsey also identifies cash reserves as a top candidate.

At the same time, a March 2026 IMF document revealed that a shock to stablecoin demand could push down short-term government bond yields, weakening the US dollar and spilling over into crypto and stock markets.

The digital dollar form is becoming a macro-related market infrastructure.

What Stablecoins Still Have

The New York Fed study argues that the real benefit of stablecoins lies in their use in global, open-access, permissionless systems.

According to the same study, the market capitalization of stablecoins recently exceeded $260 billion, and the annual trading volume of organic stablecoins increased from $3.29 trillion in 2021 to $5.68 trillion in 2024.

Stablecoins still have distribution, reach, and composability advantages that bank tokens can have a hard time matching, especially if the bank product is initially launched in a private or permissioned environment.

The second New York Fed staff report, published in February 2026, provides a framework for understanding the endgame. We find that the optimal outcome depends on regulatory costs and bank incentives.

The bull case for banks and tokenized deposits assumes that Mr. Hill’s proposal becomes effectively final as described.

As more banks launch tokenized deposit products, combining programmability with deposit status and existing compliance infrastructure, these tokenized deposits will become the preferred on-chain cash leg for regulated tokenized securities and funds.

This result is reinforced by the March 5th capital neutrality measures for tokenized securities and the recent introduction of banking products such as BNY.

The stablecoin bull case assumes that insurance distinctions are less important than network effects.

Stablecoins continue to win in a landscape dominated by universal wallet access, composability, 24/7 transferability, and cross-border usage.

Banks are still participating, but through stablecoin subsidiaries under GENIUS rather than deposit token products, especially where tokenized deposits are largely permitted and institutional-only.

Future market segmentation

If both stablecoins and tokenized deposits can be moved on-chain, and only one category can maintain the treatment of regular deposits, the market could begin to segment by function.

Open, borderless, internet-native payments are likely to lean toward stablecoin-centric solutions. Institutional payments, collateral movement, and regulated tokenized asset markets could tilt towards tokenized deposits.

Describing the upcoming proposal, Hill said the FDIC is particularly interested in comments regarding stablecoin pass-through issues and tokenized deposit arrangements involving third parties.

Hill ties the treatment of deposits to whether the product actually meets the statutory definition of a deposit, and the FDIC is still seeking comment on the third-party structure. Design risk is real.

Banks can compete by keeping deposit status on-chain. Stablecoins could dominate open networks, and tokenized deposits could dominate regulated payments.

The outcome will depend on whether the insurance benefits outweigh the network benefits and whether banks can build deposit products that work across the same open systems in which stablecoins already operate.