Bitcoin price is set further away from Bitcoin holders

Bitcoin spent the end of March looking calm on the surface, but in an unusually crowded range underneath.

By Monday, Bitcoin was trading around $67,000, after what had already been one of the year’s biggest derivatives events and a week of institutional withdrawals from spot ETFs.

This combination deserves more attention than ever. Traditional analysis divides movements into separate buckets. Option expirations belong in one box, ETF flows in another box, and prices in a third box.

But the reality is that Bitcoin’s short-term price formation is moving away from people who hold Bitcoin because they want it, and closer to people who hold Bitcoin exposure to hedge, roll, allocate, or mitigate risk within the wrapper.

This shift changes how we should read the market. It also changes what Bitcoin movements actually represent.

Price discovery has moved to a Bitcoin wrapper

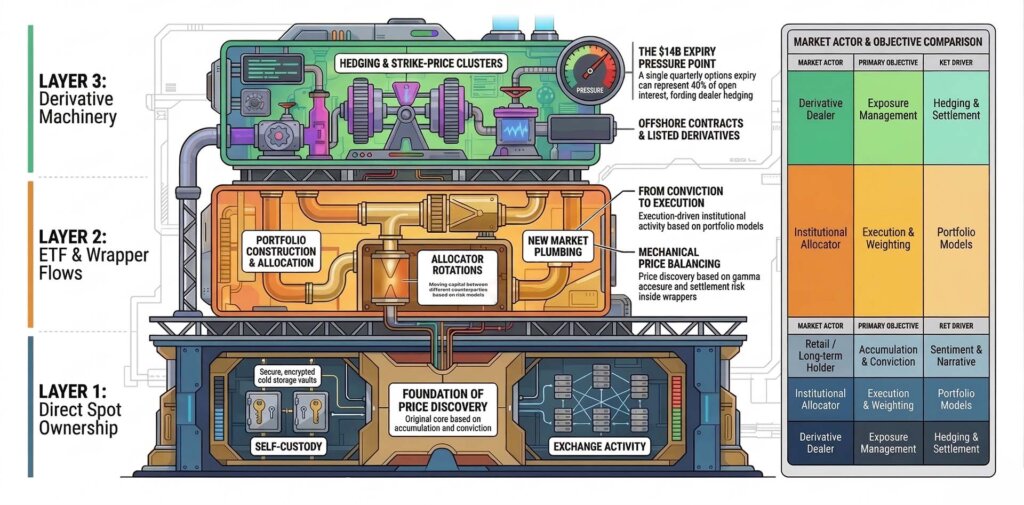

The first pressure point came from derivatives. Ahead of Friday’s expiration date, crypto slate Reported that approximately $14 billion of Bitcoin options are scheduled to be rolled off on Deribit. This represents nearly 40% of the exchange’s open interest.

The event collided with the biggest quarterly expiry of the year and a market already under geopolitical stress. However, the more important point lies one layer below.

If maturity is large enough relative to open interest, prices can begin to reflect the needs of dealers and other intermediaries who manage exposure until settlement. Pricing becomes a balancing process.

This distinction sounds technical until it involves how people interpret every move on a chart. Retail investors still tend to read Bitcoin through the lens of belief. They assume that a rise means more buyers want the asset, a fall means less confidence, and a sideways range means the market is waiting for news.

In markets shaped by large publicly traded products, publicly traded options, and financial institutions’ balance sheet decisions, these measurements are less reliable. Quiet sessions can involve a large amount of mechanical activity. A sharp move could reflect a hedging adjustment before reflecting a directional view of Bitcoin itself.

That’s why the $14 billion expiry is more than just a note on volatility. The expiration date was confirmed at 08:00 UTC on March 27th, extinguishing approximately 40% of Deribit’s open positions.

This size raises a simple question for spot holders. If a significant portion of short-term prices is driven by hedging and settlement behavior around exchange-traded contracts, how much of what people call Bitcoin demand is actually derivative maintenance?

The question becomes clearer when ETF flows reenter the picture. Farside Investors’ Spot Bitcoin ETF tracker maintains a continuous scorecard for US commodities, and the broader pattern out to 2026 is one of recurring outflow pressure.

Billions of dollars have flown out of this category this year. This flow pressure creates a second layer of distance between Bitcoin price and the intentions of Bitcoin holders.

While an ETF stock is a Bitcoin exposure, the trading decisions behind it could belong to an allocator rotating between products, a risk manager reducing total exposure, or a portfolio rebalancing that has little to do with the network’s long-term view, financial theory of assets, or self-custody.

When you combine these two channels, the market starts to look different.

The first channel is options, where maturity-related positioning can shape short-term movements as traders and dealers manage exercise exposure, gamma, and settlement risk.

The second channel is ETFs, whose flows reflect portfolio construction decisions in traditional finance as much as they reflect demand for Bitcoin itself.

One channel relies on hedging machinery. The other one depends on the demand for rappers. Both are a layer removed from the old mental model of Bitcoin’s price being primarily set by direct buyers and sellers in the spot market.

This layer change has practical implications for those who hold small amounts of BTC, own ETFs in their brokerage accounts, or treat Bitcoin as a signal asset. Many believe they are keeping an eye on demand for this asset. They are also increasingly focused on the demand for packaging around assets.

Why mild price movements can cause more market stress than meets the eye

This helps explain a pattern that many people have felt during the past few sessions, without naming it exactly. Bitcoin around $67,000 may seem stubborn. It can also seem oddly quiet considering the amount of surrounding macro noise and flow pressure.

The intraday range was within the emotional expectations people typically have for end-of-quarter maturities of this size. This kind of restrained movement often attracts lazy words about indecision.

A large expiration event can compress the movement as the market gravitates toward areas with the densest derivative exposure, then releases that compression after settlement when the hedge structure is reset.

When open interest is concentrated around a large strike, the market can spend its time focusing on levels where there is minimal pain or imbalance toward settlement. This dynamic is shaped more by positioning than beliefs.

Once that framework is established, some common complaints become more meaningful. While ETF funds are outflowing, Bitcoin can be maintained. Bitcoin could decline after a long period of positive adoption news. Bitcoin may seem insensitive to the narratives that once would have driven bigger moves.

These results appear contradictory when the market considers it a direct referendum on Bitcoin’s conviction. If you look at the market as a hierarchical structure where direct holders, ETF allocators, option traders, and dealers all belong to the same pool, each with different motivations and time horizons, they appear perfectly consistent.

The deeper meaning is psychological. Casual Bitcoin observers still tend to assume that asset movements are told by a single voice. That assumption was always incomplete. It’s much weaker now.

Markets have become more understandable in some ways, but less intuitive in others. There is more data, more regulated vehicles, and more institutional entry points.

At the same time, the chain of causation between a Bitcoin and someone who wants it has become longer. There are more intermediaries along the way, more wrappers surrounding exposure, and more reasons for capital to touch Bitcoin without sharing the worldview that built the asset’s initial holder base.

Many still consider Bitcoin to be the only large asset where ownership and beliefs align more closely than in traditional markets. That relationship has weakened.

Individuals who directly own Bitcoin in self-custody and funds that own or release Bitcoin exposure through ETFs are part of the same price formation process, but they bring very different behaviors to that process. Add a large options market to the mix, and day-to-day movements become even more disconnected from the simple question of who believes in Bitcoin.

The next challenge continues beyond maturity and ETF withdrawals.

That doesn’t make Bitcoin any less relevant. It changes the map. Added layers to price detection. The first layer is direct spot ownership and exchange activity. The second is the creation, redemption, and secondary market trading of ETFs. The third is listed and offshore derivatives, especially around large maturities. The fourth is macro capital, which uses Bitcoin as one expression of a broader portfolio view.

Any session can be dominated by a single layer or by interactions between multiple layers simultaneously.

Later this month, we provided a clear example of that hierarchy. High maturities, visible ETF pressure, geopolitical stress, and spot prices hovering around the mid-$60,000s have created an unusual mix of noise and restraint.

This combination points to an unpleasant conclusion for those who still frame their every move with emotion. Short-term Bitcoin prices are increasingly shaped by market mechanisms.

The market plumbing is where much of the real price formation takes place once the asset grows large enough to attract listed vehicles, listed options, and organized balance sheet management. Bitcoin has reached that stage. The changes here are not about validity, but about interpretation.

Retail trade can still move the market, and long-term holders remain important to the supply structure. Their influence now shares the field with a much larger group that is not aimed at accumulation, ideology, or even belief in direction. Their purpose is execution.

Working capital behaves differently. I buy it because a portfolio model says it makes me gain weight. It was sold after the risk committee directed us to reduce our exposure. There is too much open interest when exercising the right, so we hedge. It rotates because the calendar asks for rotation. Before reacting to the Bitcoin whitepaper, react to the correlation and liquidity conditions.

This is a very different kind of pricing component than what many people still imagine when they open a Bitcoin chart.

The next test takes place during the post-expiration session and during sustained ETF flow pressure. If Bitcoin starts trading in a freer direction after the quarter’s biggest options event passes, it will strengthen the view that the hedging machine was squeezing the move toward settlement.

If ETF withdrawals continue to shape the demand structure, it will strengthen the second part of the theory: Bitcoin’s wrapper has more influence over price discovery than many holders fully realize.

For those with some capital in the market, the key adjustments are conceptual before they are tactical.

Looking at the Bitcoin chart immediately raises questions. What are Bitcoin buyers and sellers thinking now? That question is still relevant. It doesn’t go far enough anymore.

More useful questions lie deeper. Who are the holders, allocators, and hedgers that are shaping prices in today’s markets?

This is a different way of looking at Bitcoin, and once you see it, it’s hard to unsee it.

There are still old financial and cultural arguments surrounding this property. Currently, its short-term price formation follows a more traditional market structure.

Bitcoin holders will remain in the market. They no longer sit at the center of every movement.

(Tag translation) Bitcoin