Bitcoin may trade around the clock, but its liquidity is no longer the case. The asset, which was supposed to be more resilient after absorbing billions of dollars in institutional capital through ETFs, has instead formed a dual personality, appearing deep and orderly during New York trading hours but becoming considerably more fragile when the desks of Wall Street go dark.

Kaiko’s latest data released this week quantifies what many traders have been feeling for some time. In other words, the same ETF-driven maturation that deepened Bitcoin’s weekday market is hollowing out weekend trading, creating a two-tier trading environment where smaller participants absorb a disproportionate share of the risk.

According to Kaidaka’s analysis, since the Spot Bitcoin ETF was launched in January 2024, institutional investor participation has been concentrated during U.S. weekday trading hours, and their share of trading volume during those hours has risen to about 47%.

Currently, weekday trading volumes are consistently twice that of weekends, and the gap widened throughout 2025 and into 2026 as institutional allocations increased. The promise of a 24/7 unified market, which was supposed to be the feature that distinguishes cryptocurrencies from everything else in the financial world, is actually weakening. Because while Bitcoin is still open every Saturday and Sunday, the capital that provides that depth is not.

BTC still trades 24/7, but serious liquidity is becoming more selective

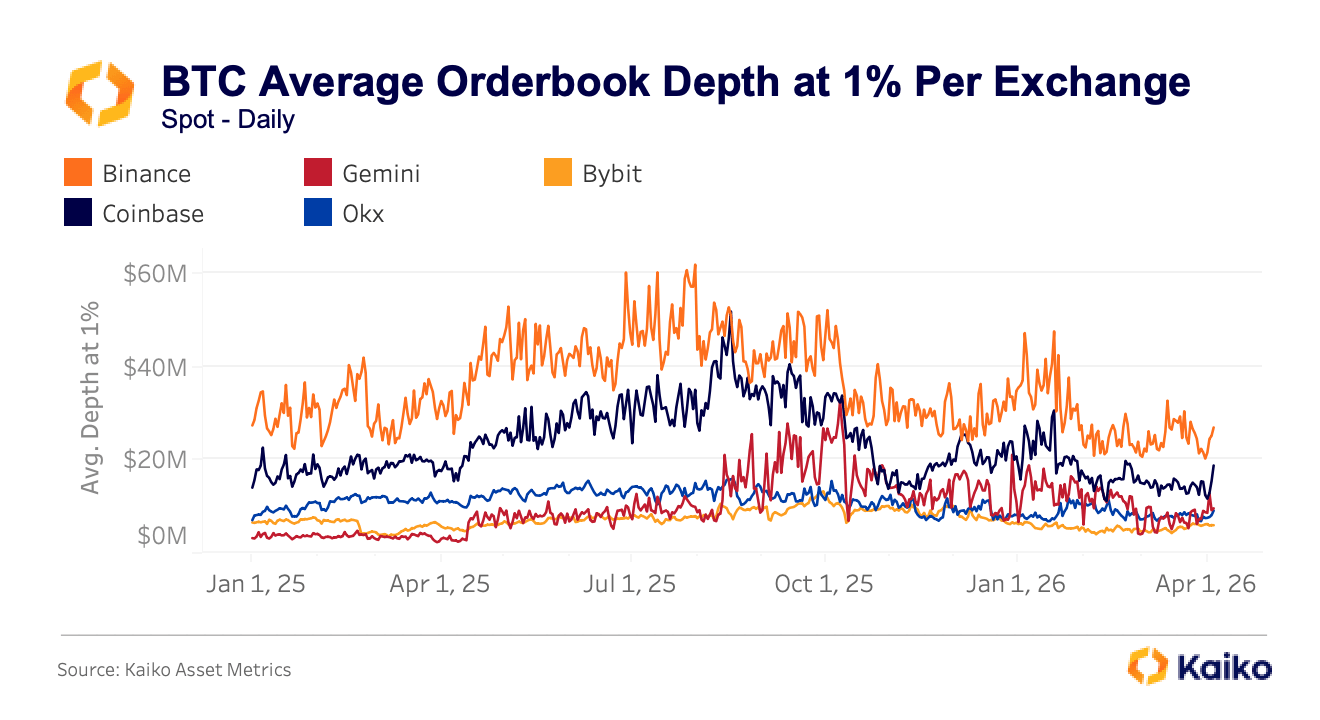

This change is seen in what traders refer to as order book depth, or the total amount of buy and sell orders that are within a certain range of the current price. This is an important measure of liquidity and serves as a rough measure of how much buy or sell the market can absorb before the price starts to move against you.

Kaiko tracks 1% depth from the halfway point. This means all remaining orders within 1% above or below the current Bitcoin price. This number varies greatly depending on where you trade. Binance consistently offers a depth of around $30 million at that level, while Coinbase ranges from $16 million to $20 million.

Trading volumes on secondary exchanges such as Gemini, Bybit, and OKX are typically $10 million to $15 million, creating a 2x to 3x difference and directly leading to price deterioration for those who meaningfully place orders on the wrong platform.

This difference is not stable under stress and in fact tends to blow out almost exactly at the most costly times. During the tariff-driven sell-off last October, Bitcoin spot prices diverged significantly between venues within minutes, with Binance lagging at $102,318, OKX at $102,142, and Bybit at $101,675, with the $643 spread lasting for minutes rather than seconds as would be expected if normal automated arbitrage mechanisms were effectively closing the gap.

This pattern was repeated during geopolitical escalation in the Middle East in March 2026, when BTC-USDT trading costs on Bybit spiked 230% from normal levels, and similar spikes occurred on OKX and Binance. Both episodes began over the weekend, when institutional participants had already exited and orders were at their thinnest.

When Wall Street closes, the difference between ‘price’ and yours can widen rapidly

This has very real and concrete consequences. Bitcoin price fell below $78,000 on Saturday afternoon, February 1st, and within 24 hours, more than 335,000 traders had liquidated approximately $2.2 billion.

This drawdown was not due to a fundamental collapse specific to cryptocurrencies, but rather was amplified by structurally illiquidity over the weekend. This means that the market is not reacting to bad news about Bitcoin, but rather to the mechanical reality that there are fewer participants to absorb selling pressure.

A subsequent Van Eck analysis, which extensively analyzed February’s crash, found that Bitcoin’s one-day price movement on February 5 ranked as one of the asset’s fastest on record, measured by statistical measures of speed and size. Stochastic models predict such extreme events to be rare, but they have now surfaced twice in five months.

Traders who buy and sell on secondary venues on Saturday nights or during periods of heightened volatility may not receive prices close to the consensus Bitcoin price they believe they are trading.

The gap between quoted and executed prices tends to widen when the effects of bad executions are most severe, and the asymmetry is most severe for participants who lack the institutional infrastructure to wait for better terms.

It is clear that retail traders are still participating in cryptocurrencies, but Kaiko’s research suggests that they are being relegated to thinner, less protected parts of cryptocurrencies. From a time perspective, retail trade is more risky during after-hours, weekends, and periods when ETF flows are low and institutional market-making recedes.

Geographically, retail still dominates the market, which bears no resemblance to US ETF-driven Bitcoin trading, with South Korea continuing to rely heavily on retail participation and altcoin trading volumes, while Turkish crypto activity reflects macro stress hedging and stablecoin demand rather than the surge in institutional activity in the US.

There is also an asset aspect to the split.

Institutional capital, channeled through ETFs and prime brokerage arrangements, has standardized Bitcoin trading above all other cryptocurrencies, concentrating sophisticated market making and deep liquidity in BTC, leaving the rest of the space (altcoins, local currency pairs, small platforms) with thin coverage and less professional support. Speculative and fragmented activity persists in abundance across a broader range of markets, rather than in the same exchanges or time zones in which financial institutions are established.

Market quality differs even for the same Bitcoin

What emerges from this data is becoming increasingly difficult to deny. Two Bitcoin markets may now be operating in parallel. A deeper, more efficient, institutional-style weekday market, accessible through ETFs and major venues, and a thinner, more volatile after-hours market, where smaller traders are likely to be present and who are more likely to bear the costs of poor execution.

In theory, Bitcoin is the same asset for everyone, but in reality, the quality of the market you encounter depends largely on when and where you trade.

None of this is an argument that ETFs destroyed Bitcoin. Institutional investor participation has brought real benefits, including deepening aggregate liquidity, lower average spreads in normal times, and a degree of legitimacy that did not exist in previous cycles.

Cumulative net inflows into U.S. Spot Bitcoin ETFs have remained at around $53 billion to $54 billion since their inception, even after large outflows in early 2026, allowing them to absorb large amounts of capital and survive true volatility without collapsing.

But the same forces that improved Bitcoin’s best times appear to have revealed how uneven the market becomes when participants retreat, bringing maturity to some sessions while leaving others vulnerable.

(Tag translation) Bitcoin