Iran’s announcement on Friday that the Strait of Hormuz would open during the current ceasefire triggered one of the sharpest oil reversals this year.

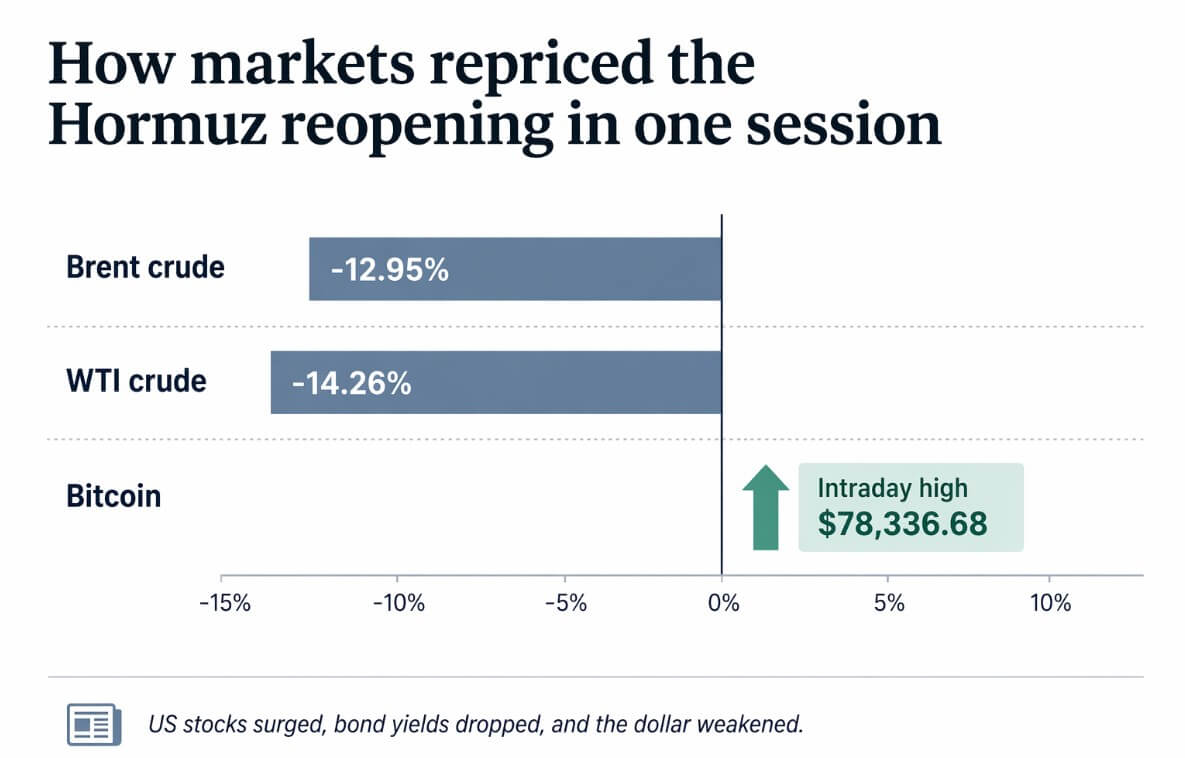

Brent crude oil fell 12.95% to $86.52, and WTI fell 14.26% to $81.19, both the lowest since March 11th and the biggest single-day decline since April 8th. U.S. stocks soared, bond yields fell, the dollar weakened and Bitcoin hit an intraday high of $78,336.

Traders stripped the war premium they had spent weeks building into oil prices and repriced risk assets accordingly.

Yesterday, the strait opened on Iranian terms. Merchant ships required permission from Iran’s Ports and Maritime Authority and the Revolutionary Guards and had to take safe passageways designated by Iran, but the U.S. blockade of Iranian shipping will remain in full until a broader diplomatic solution is reached.

That window is already getting narrower. As of April 18, after the US lifted the blockade, Iran announced it had closed the strait again, and markets were on a countdown to the April 22 cease-fire deadline.

Only eight oil and gas tankers moved during the reopening, underscoring how far the route is from anything resembling normal traffic.

For a short period of time, IMO was unable to confirm whether the arrangement met freedom of navigation criteria.

Shipping lines are waiting for legal and safety clarity before resuming normal sailings, and the US Navy said the mine threat in parts of Hormuz is not fully understood.

A Pakistani-flagged tanker carrying around 440,000 barrels of UAE crude oil left the Gulf on April 17, giving concrete data that the transit is possible.

That short test never became normalized. The Associated Press reported that only eight oil and gas tankers passed through during the brief reopening period before Iran reimposed restrictions, leaving Bitcoin with just four days to see if the ceasefire would restore actual shipping by April 22.

Bitcoin is currently caught between a market pricing in a rapid reopening and a strait that will close again as of April 18th, ahead of the April 22nd cease-fire deadline.

arithmetic of fear

According to EIA data, the average daily oil flow through the Strait in 2024 is 20 million barrels, about 20% of global oil liquids consumption, with 84% of crude oil and condensate and 83% of LNG flowing to Asian markets.

This is the specific criteria behind the market countdown. Unless traffic is restored by April 22, the route, which transports about a fifth of the world’s petroleum liquids, will remain crippled.

Since the conflict began, the war has removed more than 500 million barrels of crude oil and condensate from the global market, resulting in approximately $50 billion in lost production. In comparison, global onshore crude oil inventories fell by about 45 million barrels in April alone.

As recently as April 7, EIA expected the average price of Brent to be $115 in the second quarter. On April 13, Morgan Stanley kept Brent crude oil prices unchanged at $110 in the second quarter and $100 in the third quarter, modeling only a modest export recovery through October.

Brent’s stock price, at $86.52, is well below a key benchmark published within the past two weeks. The market is leading the way to a return to normalcy that neither the EIA nor Wall Street expected.

This asymmetry creates a financial premium that may dissipate faster. The IEA director general said it could take about two years for energy production across the Middle East to return to pre-war levels.

Why reopening is still fragile

Iran’s operational message on April 17 largely mirrors the deputy foreign minister’s statement on April 9 that ships were able to navigate with Iranian coordination, but actual traffic was less than 10% of normal. That’s about seven ships per day compared to the usual 140.

Although the diplomatic probability distribution changed, the passing rules remained roughly the same. The 10-day ceasefire and the return of US-Iranian diplomacy have reaffirmed markets to the same basic operating framework as détente.

| problem | Current situation | why is it important |

|---|---|---|

| commercial walkway | Permitted with Iranian coordination | Passage is possible, but with conditions. |

| authorization | Port and Maritime Authority + IRGC approval required | Shows that Iranian control remains central |

| routing | Safe lane designated by Iran | Not equivalent to normal freedom of navigation |

| IMO standard | Not yet confirmed | Legal/institutional ambiguity remains |

| my risk | not yet fully understood | Physical risks still impede normal traffic |

| Insurance company/shipper | waiting for clarification | Normalization of operations has not been achieved |

| us blockade | still valid | Broad settlement still unresolved |

| traffic level | below normal | Reopening is not yet routine |

Although the Lebanese ceasefire has become part of the diplomatic backdrop, the Israeli military presence in southern Lebanon and the disarmament of Hezbollah remain unresolved.

The blockade will remain in effect until a broader agreement is reached, and even if ships do start moving, any material relief will follow diplomatic headlines weeks later, as it takes ships about 21 days to travel from the Gulf to Rotterdam.

Insurance premiums have not yet normalized, authorities have not lowered mine alerts, and no major liner has publicly announced that the route will be cleared.

Bitcoin transmission channel

Today’s Bitcoin movements occur through specific macrochains. The drop in oil prices has lowered the near-term inflation outlook and shifted expectations around the Federal Reserve’s interest rate path.

Traders went from setting prices on hold until 2027 to cutting prices until December 2026, sharply reducing the amount of expected tightening.

The March FOMC meeting minutes already noted that rising oil prices are expected to push up inflation in 2026, and that there is a risk that the prolonged conflict in the Middle East will further sustain spillovers into core inflation.

As oil prices fell, that hawkish risk was partially eliminated. Bonds rose, the dollar fell, stocks rose, and Bitcoin moved in tandem with widespread risk-on price repricing.

Bitcoin has functioned as a liquidity-sensitive risk asset over the past few months, with its trajectory following Fed expectations, technology market sentiment, and the magnitude of the financial backdrop.

Sustained easing that reduces inflation and keeps oil prices low long enough to reinstate the Fed’s rate-cutting policy would be a real macro tailwind for Bitcoin.

The road ahead

Although the rhetoric deteriorated rapidly after the initial announcement, negotiations have not yet formally broken down and a ceasefire remains in place.

If this spreads to a broader rapprochement between the US and Iran, traffic along the lanes approaches internationally recognized standards, mine warnings fade, and insurers soften their stance, oil bailouts could extend beyond today’s prices.

EIA had already seen the market as oversupplied before the dispute began. A durable restart could see more premium outflow than most traders currently expect, sending Brent into the mid-$70s to mid-$80s.

In this situation, expectations for Fed rate cuts would move further, the dollar would remain under pressure, and Bitcoin would have the cleanest macro tailwind in the current cycle.

Citi’s 12-month bull market of $165,000 represents the outer bounds of what a sustained macro thaw of that size can support.

| scenario | shipping reality | brent mountains | Fed involvement | Impact of Bitcoin |

|---|---|---|---|---|

| Ceasefire will be maintained and transport will be normalized. | Ship numbers increase, mine warnings fade, insurance companies relax | Mid $70s to mid $80s | cut pulled forward | The strongest macro tailwind for BTC |

| Ceasefire nominally holds, but normalization fails | Controlled routes, decreasing number of ships, and insurance companies continue to be cautious | $100–$115 | High profits over a long period of time | BTC loses de-escalation premium |

A cheaper negative outcome would be a ceasefire that is nominally preserved but never normalizes shipping.

Mine warnings continue, politically controlled routes keep insurance companies on alert, tanker numbers remain well below the 140-vessel-per-day standard, and operational realities never match the diplomatic headlines.

In this scenario, oil prices rebound toward the $100 to $115 range that influenced EIA and sell-side forecasts until just last week.

Inflation easing stalls before the Fed’s calculations are reached, interest rate cut expectations recede and Bitcoin abandons its de-escalation premium.

Citi’s recession downside case of $58,000 marks the limit for Bitcoin to re-enter a prolonged tight macro regime.

These two paths will only become clearer depending on the number of ships, the actions of insurance companies, and whether the wording of the U.S. blockade changes in the next 72 hours.

Due to the 10-day ceasefire period, this deal has a built-in expiration date.

Things to watch include whether the number of ships remains well above April 9 levels, whether the IMO formally approves the transit agreement, whether the US-Iran talks lead to any amendments to the blockade language, and whether Bitcoin continues to price oil bailout as the Fed’s bailout narrative.

(Tag translation) Bitcoin