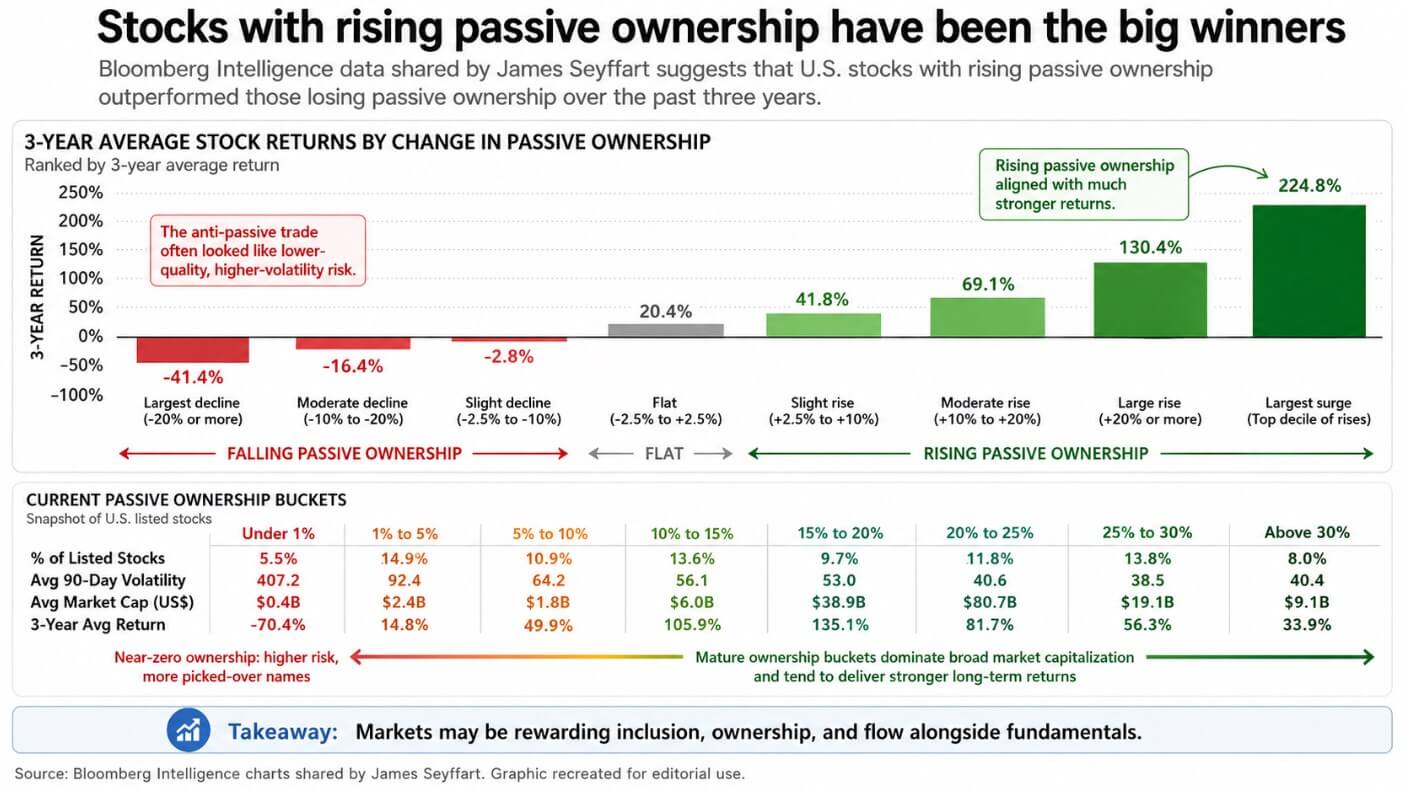

Passive investing has become one of the most powerful forces reshaping the stock market, and the proof is in the earnings data.

Over the past three years, stocks that have gained passive ownership have dramatically outnumbered those that have lost passive ownership, according to Bloomberg Intelligence data compiled by ETF analyst James Seifert.

The market has rewarded inclusivity, ownership and flow, along with fundamentals. The most unpleasant implication of this chart is that anti-passive trading is much like a junk withdrawal of small, volatile, newly listed, low-quality stocks left behind by structural flows.

Ownership concentration increases over time and inventory within passive machinery tends to remain there.

Bitcoin is currently building a similar infrastructure. The SEC approved the spot listing of Bitcoin ETFs in January 2024, and the two years since have rewritten how institutional capital reaches BTC.

The U.S. Spot Bitcoin ETF had cumulative net inflows of approximately $58.4 billion as of late April 28, and BlackRock’s IBIT has approximately $61.9 billion in net assets.

Euronext will list BlackRock’s iShares Bitcoin ETP in Europe in March 2025, saying it will allow investors to access Bitcoin without the complexity of direct trading and holding.

Deutsche Börse Clearstream has expanded its institutional cryptocurrency storage and payment services to include Bitcoin in addition to traditional assets.

Bitcoin became a wrapper investment accessible through standard brokerage rails, and that access reshaped who could own Bitcoin.

Rappers change the market

Regular inflows into funds with the same name create a persistent price-insensitive bid that worsens over time, which is what drives the outperformance of passive stocks.

Bitcoin ETFs function according to investor demand, with purchases arriving as creation flows and sales liquidated through redemptions on any timeline, independent of reconstitution schedules or index instructions.

BlackRock’s December 2024 Portfolio Note lists a 1% to 2% Bitcoin allocation as a reasonable range for a multi-asset portfolio for investors who accept the risk of sharp price declines and believe in broader adoption.

When the world’s largest asset managers frame volatile assets from an allocation sizing perspective, that becomes something that advisors can discuss from a portfolio construction perspective.

The 2025 Fed Note found that crypto ETP bid-to-bid spreads are comparable to spreads for other ETFs and similarly sized ETPs. The group argued that NAV premiums for crypto funds should be monitored as a measure of how interconnected crypto and stock markets are.

This flow confirms that plumbing work is being done, as U.S. spot Bitcoin ETFs added about $2 billion in net inflows from April 14 to April 24, based on daily totals from Pharcyde Investors. And on April 27, there was a one-day outflow of $263.2 million.

In two weeks, the same vehicle demonstrated both the ability to build a structural bid and the ability to reverse it with methodical speed.

Allocation calculations are the driver

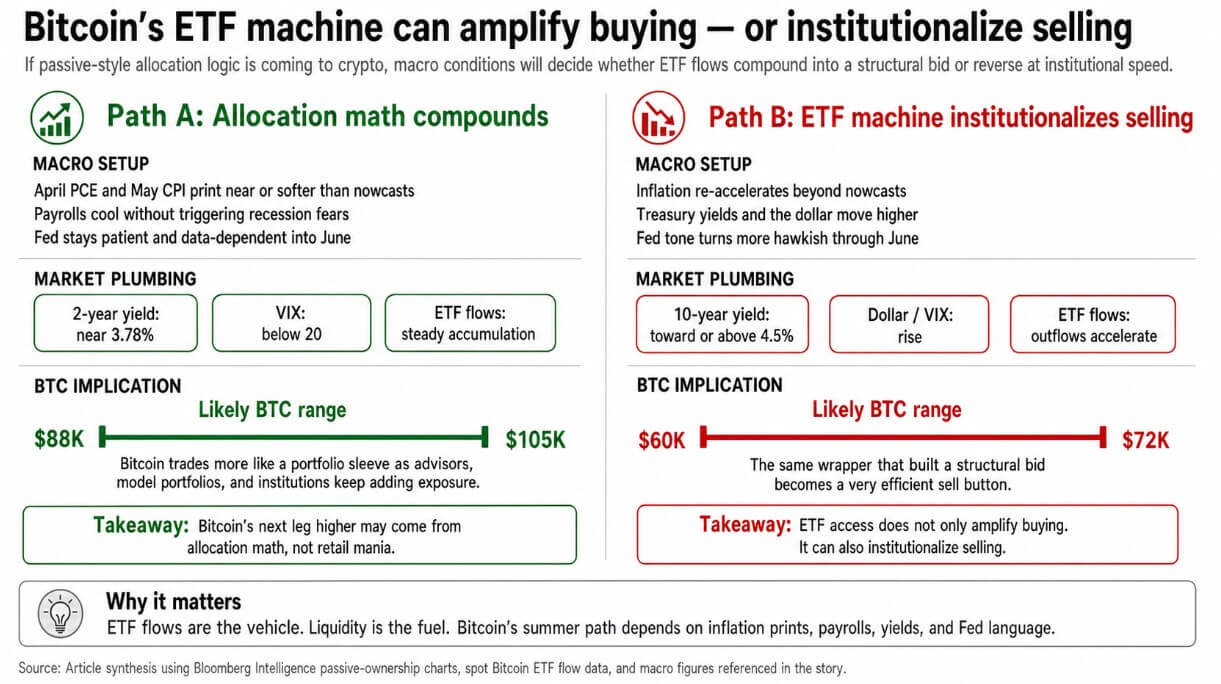

If April PCE and May CPI are close to or softer than the Cleveland Fed’s nowcast (April CPI 3.56% y/y and April PCE 3.60% as of April 28), April payrolls could cool without triggering recession concerns and the Fed could continue to rely on the data until its June 16-17 meeting.

This will keep the two-year Treasury yield near 3.78%, the level seen in late April, keep the VIX below 20, and allow advisors and institutional investors to accumulate allocations through the June Fed window.

In that environment, Bitcoin trades as a portfolio sleeve, receiving regular flows from model portfolios, registered investment advisors, and institutions that size positions once and leave them alone.

BlackRock’s Spring 2026 Outlook frames current macro settings as a trade-off for benign stagflation, with the Fed pausing and only moving to gradual easing if inflation continues to slow or growth is moderate.

This is the context in which wrapper bidding can be further exacerbated by steady accumulation by buyers who monitor portfolio weights driven by allocation calculations.

If the weight of Bitcoin in discretionary model portfolios continues to grow, the next stage could resemble what happens when an asset takes a permanent seat in a standard allocation framework.

In a bullish scenario, BTC could be in the $88,000 to $105,000 range by summer, depending on the allocation calculation alone. The cumulative net outflow of IBIT is $65.37 billion, while the cumulative net outflow of GBTC is $26.26 billion.

Allocation battles within the Bitcoin wrapper market have already produced winners, who control the institutional distribution networks.

| metric | shape | why is it important |

|---|---|---|

| US Spot Bitcoin ETF Cumulative Net Inflows | ~$58.4 billion | Demonstrates the scale of institutional adoption via wrappers |

| IBIT net worth | ~$61.9 billion | Demonstrating BlackRock’s superiority in distribution for institutional investors |

| IBIT Cumulative Net Flow | $65.37 billion | Shows where structural bids are concentrated |

| GBTC cumulative outflow amount | -$262.6 billion | Indicates capital rotation for legacy wrappers |

| ETF net inflows from April 14th to 24th | ~$2 billion | Evidence that institutional bids are building rapidly |

| April 27th ETF net outflow | -$263.2 million | Evidence that the same vehicle can reverse quickly |

Machines institutionalize sales

The same rapper who built a bid of $2 billion in 10 days caused a one-time outflow of $263.2 million.

If inflation reaccelerates above current levels, as the Cleveland Fed’s model already puts PCE in April at 3.60% year-over-year, if Treasury yields recover, the dollar strengthens, and risk appetite shrinks, ETF outflows could clear Bitcoin’s order book at the speed and scale of institutional investors.

March CPI is already 3.3% compared to the same month last year, core CPI is 2.6%, February PCE is 2.8%, and core PCE is 3.0%.

Inflation data has been consistently above target, and if the April data beats the nowcast, the April 28-29 Fed meeting will signal a hawkish tone through June.

In that environment, Bitcoin trades as a high-beta macro asset with a very efficient sell button. As of late April, the 10-year Treasury yield was 4.31%, and a rise above 4.5% would compress equity multiples and remove the liquidity backdrop to comfortably hold a small portfolio allocation to Bitcoin.

Advisory models that placed 1% to 2% positions when risk appetite was supportive face the same rebalancing logic. Allocation is determined by whether Bitcoin depreciates enough relative to your portfolio.

In a bearish scenario, BTC would be in the $60,000-$72,000 range and would be pulled down by the same institutional mechanisms that have been driving it up.

The passive equity analogy has similar implications for the broader crypto market. The antipassive bucket in Seifert’s data, or stocks that have lost ownership share, is often home to thinner, more volatile stocks that rely on stock selection narratives, consolidating around wrappers where structural flows dominate.

Bitcoin holds a dominant ETF wrapper and distribution to institutional investors. Instead, a long tail of tokens competes for discretionary attention.

If passive logic is indeed moving into cryptocurrencies through the ETF channel, then Bitcoin will concentrate the structural bidding while everything else competes for a shrinking pool of discretionary allocations.

The ETF machine amplifies any liquidity provided by the macro environment and feeds it into the Bitcoin order book through a cleaner, more visible channel.

Whether Bitcoin’s next move is due to compounding allocation calculations in a patient macro environment, or hawkish liquidations via financial institution exits, it will depend on the same set of inflation performance, payroll data, and Fed language that governs all other risk assets in its portfolio.

(Tag translation) Bitcoin