The meta unfolded quietly last week $USDC Four years after the company sold its bankrupt Diem stablecoin (formerly Libra) assets to Silvergate Bank for $182 million, the payments to creators in Colombia and the Philippines have reignited old questions about whether Big Tech will finally enter retail finance.

The answer in 2026 is yes, but not from Apple, Google, or Mark Zuckerberg.

Singapore Summit: Meet the biggest Asia-Pacific brokers you know (and the ones you don’t!).

The most obvious competitive threats to Robinhood, Trading 212, eToro and Revolut are clustered in Walmart’s OnePay app, which has a market cap of more than $4 billion, and Elon Musk’s X Money, which is currently licensed to process payments in 41 US states.

Both rely on the same architecture, Brokerage as a Service, or BaaS, and incorporate Zerohash and DriveWealth into apps that are already used by hundreds of millions of users.

OnePay added Bitcoin and Ethereum trading through Zerohash in October 2025, and later that same month partnered with DriveWealth to bring stocks and ETFs to the same banking app.

X has hinted that it plans to roll out cash tags for stock and cryptocurrency charts, embedding trades directly into timelines.

Meta’s $3B Creator Pipeline Arrives $USDCnot a Libra

Meta confirmed on April 29th that it has started routing payments to Circle creators. $USDC Payments with stablecoins Solana and Polygon via Stripe’s Link wallet. The pilot is currently limited to two markets chosen due to their high density of creator economies and weak cross-border banking infrastructure.

According to Fortune, the company paid out about $3 billion to creators around the world in 2025, growing about 35% year over year. Polygon Labs CEO Marc Boisron said the program is expected to expand to more than 160 countries by the end of 2026.

This setup clearly avoids the central feature that doomed Libra: the meta does not issue its own coins. Spokesman Andy Stone publicly pushed back on any similarities to the original 2019 project.

Meta is $USDC Stablecoins on the Polygon blockchain aim to speed up payments and simplify cross-border transfers.

The program is currently being piloted in Colombia and the Philippines and will be expanded to more than 160 countries. pic.twitter.com/rHbGOHjR3

— What’s Trending (@WhatsTrending) May 4, 2026

FinanceMagnates.com’s coverage of Meta’s stablecoin re-entry strategy suggested that the company is rushing to launch before the GENIUS Act’s restrictions on Big Tech stablecoin issuance fully take effect.

OnePay reaches $4 billion valuation with Revolut-like stack

OnePay was launched in January 2021 as a joint venture between Walmart and Rivit Capital, the same VC firm that backs Robinhood, Affirm, and Credit Karma. It rebranded to OnePay in March 2025 after acquiring fintech companies Even and ONE.

The company has built a stack that matches or exceeds Revolut in most consumer verticals by 2024-2025. A funding round in 2024 valued OnePay at $2.5 billion. According to Bloomberg, a 2025 employee bid would push that figure to more than $4 billion.

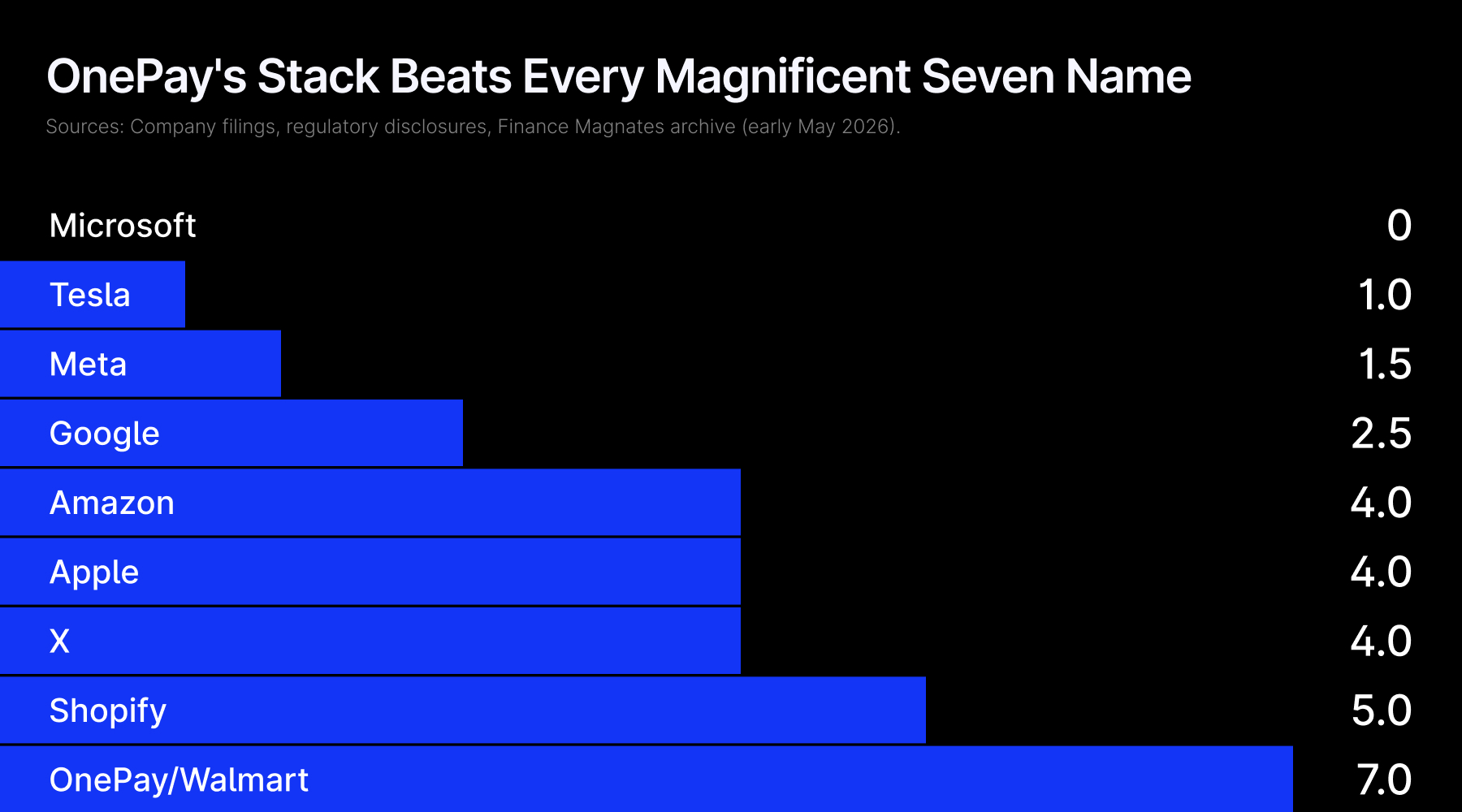

Score: 1.0 = Live Consumer Product. 0.5 = Under consideration or development. 0 = No product. Industries: Payments (P2P/Wallets), BNPL, Cryptocurrency Trading, Securities Trading (Stocks/ETFs), Banking/Deposits, Insurance, Card Products, Small Business Loans.

The stacking is impressive. OnePay operates high-yield savings through Coastal Community Bank, Klarna through BNPL, and provides paid wages to 1.6 million Walmart employees. Last fall, the Synchrony-Mastercard credit card replaced Capital One in Walmart stores.

Bitcoin and Ethereum trading through Zerohash began in October 2025, followed by stock and ETF trading a few weeks later by DriveWealth, the same company that powers Revolut’s US offering.

The app had annual payment flow of $15 billion and run-rate revenue of over $200 million by the end of 2024.

X Money launches in 41 states, with brokerage services in the works

Mr. Musk’s X Company is further along in the path to financial primordial ownership than any other company adjacent to the Magnificent Seven. The public beta of X Money began rolling out in April after several months of delays.

The product launched with FDIC-insured deposits through Cross River Bank, P2P transfers through Visa Direct, a Visa-issued metal debit card with cash back, and a 6% APY on deposits, although PYMNTS noted that it is unclear whether this rate is permanent or promotional.

Today, X․ com’s new cache tag feature for the web. Now X can become a core part of your trading terminal with real-time charts and posts for any asset. pic.twitter.com/QD8Tn4uj1l

— Nikita Bier (@nikitabier) April 30, 2026

The mediation angle is under development. X rolled out CashTag in the U.S. and Canada on April 14th, allowing users to see real-time price charts when they tap on “AAPL” or “BTC” in their timeline.

Linda Yaccarino, former CEO of X, Source: LinkedIn

At the Cannes Lions in June 2025, then-CEO Linda Yaccarino said users would soon be able to “invest and trade directly through the platform.” A smart cashtag that will lead to in-app crypto purchases is reportedly in the works.

Musk himself describes X Money as “the place where all the money is.” The architectural similarities with OnePay are unmistakable, with X connecting to the infrastructure of licensed banks and brokerages rather than building its own infrastructure.

Its distribution moat is approximately 600 million monthly active users.

Apple, Google and Amazon secretly choose partnerships over licenses

The contrast with the larger Magnificent Seven names is striking. Apple, the Big Tech company with the largest track record in financial services, has spent the past 24 months retreating to a partnership model.

In June 2024, Apple ended Apple Pay Later and instead integrated Affirm and Citigroup installment offers globally within iOS Wallet. In October 2024, the CFPB fined Apple and Goldman Sachs a total of $89 million for failing to resolve Apple Card disputes.

In January 2026, Apple approved JPMorgan Chase as its new Apple Card issuer, with more than $20 billion in card balances scheduled to be transferred over 24 months, closing a chapter on the partnership that Goldman bankers had publicly disavowed.

Google is focused on India and launched Flex by Google Pay, a credit card linked to UPI and co-branded with Axis Bank, in December 2025. Amazon’s strategy is purely embedded.

Affirm offers BNPL at checkout, and Amazon Lending issues SMB loans through Goldman Sachs, Lendistry, Parafin, and fintech Slope. None of the three individuals has applied for a broker-dealer license within the past 36 months.

Why big tech companies still refuse to build retail intermediation services

Since the failure of the Libra project in 2019, Apple, Google, Amazon, Meta, and Microsoft have jointly reduced their retail trading products to zero. The most cited reason for this is regulatory friction.

Broker-dealer licenses under FINRA and SEC, Reg BI, order flow payment scrutiny, and recent best execution reforms create higher compliance costs than money transmitter licenses.

Arkadiusz Jožwiak

“European brokers need not fear Apple,” Arkadiusz Jóźwiak, financial analyst and editor-in-chief of Comparic.pl, told FinanceMagnates.com. “They need to watch the back door, the back door that Walmart and Musk are trying to walk through with their ready-made stacks of securities.”

The second is reputational risk. Bankers who pitched retail trading products to Big Tech executives say the meeting ended on the same note. The consumer protection implications if Instagram or WhatsApp users lose money on stocks are not a battle Apple or Meta want to pick.

Third, brokerage-as-a-service eliminates the need for ownership. DriveWealth, Alpaca, Bitpanda Technology Solutions, and Zerohash now allow distribution platforms to offer transactions without holding a license.

Yahoo Finance’s one-click Coinbase trading integration, announced in February 2026, follows the same architecture.

Brokers still see Revolut as a bigger threat

For European retailers, Big Tech remains a distant concern. Revolut, which has around 60 million users, €8.5 billion in customer assets, and a reported $150 billion IPO target, is a closer competitor.

Omar Arnaout, XTB CEO

Speaking at Invest Cuff in Warsaw, XTB CEO Omar Arnaout said he believes “Robinhood probably won’t be successful in Europe,” instead pointing to Revolut as a standout competitor.

However, asymmetry is evident in user-based calculations. Together, Walmart and X touch more than 850 million people each week or month.

Robinhood reported having approximately 26 million funding accounts at the end of 2025, while Interactive Brokers ended the first quarter of 2026 with an average of 4.4 million trades per day.

If even a small percentage of OnePay or X users opened in-app trading accounts, the reduction in customer acquisition costs alone would significantly erode the funnel that mid-market brokers rely on.

For brokerages watching the Big Tech threat from across the Atlantic, the message in 2026 now is that the danger is no longer about Apple or Google launching stock trading apps.

The idea is that Walmart, Musk, and Shopify will quietly take what those companies don’t do and turn their existing user bases into customer acquisition channels that traditional brokers can’t compete with.