During Strategy’s May 5th earnings call, Strategy CEO Von Leh made it clear that the company would “sell Bitcoin when it’s advantageous for the company,” and Saylor added that Strategy “will probably sell some of its Bitcoin as a dividend just to vaccinate the market.”

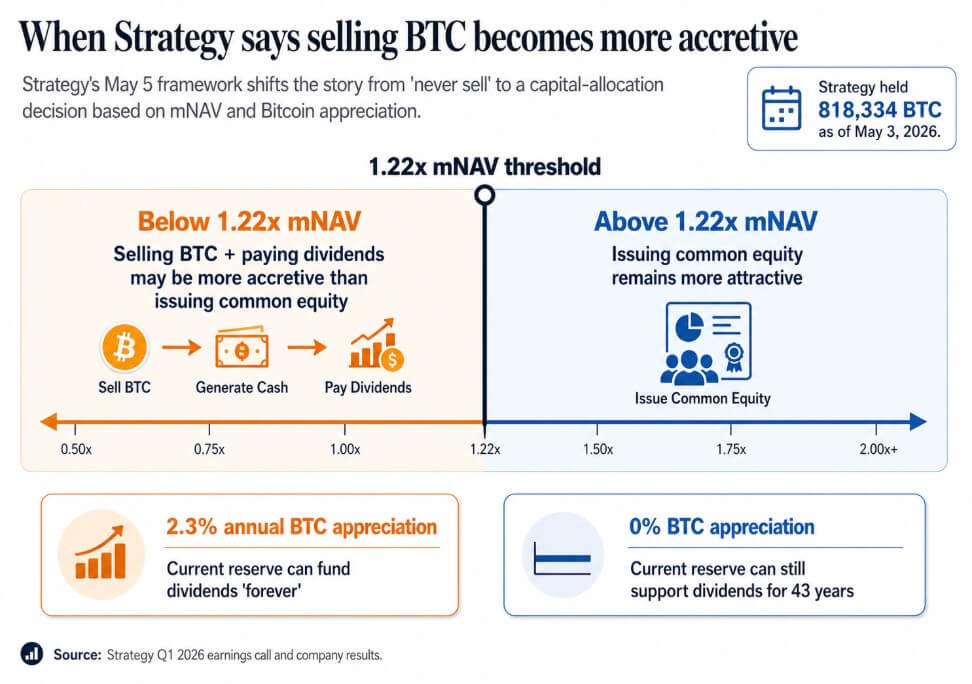

As of May 3, Strategy held 818,334 BTC, an increase of 22% since the beginning of the year, with a market value of $64.14 billion.

What was established in the May 5th conference call was the public normalization of BTC sales as a corporate finance instrument and the quantitative framework that now stands behind it.

Management stated that below mNAV of approximately 1.22x, selling BTC and paying dividends may be more accretive than issuing common stock. Saylor argued that even if Bitcoin appreciated just 2.3% a year, Strategy’s current reserves could fund the dividend “forever,” and even if Bitcoin’s appreciation rate dropped to zero, the reserves could support the dividend for 43 years.

Absolutist slogans have been replaced by a model in which companies leverage financial and credit instruments to buy when increasing, issue shares when increasing, issue preferred shares when increasing, and sell BTC when increasing.

Investors originally bought these companies as agents for Bitcoin, which is built on scarcity and permanence. The 1.22x mNAV threshold and 2.3% breakeven rate are a more honest representation of that proposition, and a more complex one.

When Bitcoin becomes liquid

Sequans reported first-quarter sales of $6.1 million, down 24.8% year over year, and an operating loss of $50.5 million. The first quarter included a realized net loss on Bitcoin sales of $11.7 million, the proceeds of which were primarily allocated to convertible debt redemptions and the ADS repurchase program.

As of March 31st, the company held 1,514 BTC, with 1,217 BTC collateralizing its $66.2 million convertible note. By April 30th, the company held 1,114 BTC, with 817 BTC serving as collateral for a $35.9 million debt due by June 1st.

This follows the same pattern in November 2025, when Sequans sold 970 BTC to redeem 50% of its convertible notes, reducing its obligations from $189 million to $94.5 million.

After two quarters of declining revenues and debt maturities, Bitcoin becomes operationally liquid. In a pledged collateral structure, BTC nominally held by a company as collateral for a debt is committed prior to a sale decision.

Sequans operates on a different scale than Strategy and has a weaker operating business behind its finance department. If BTC is needed to fund immediate debt repayments, inventory logic will take over.

MARA applied the same logic on a larger scale in March, reducing its outstanding convertible debt by approximately 30% and gaining a value of approximately $88.1 million by selling 15,133 BTC for approximately $1.1 billion and using the proceeds to repurchase convertible debt.

MARA packages this move as a balance sheet optimization based on debt structure and financing conditions, establishing that a BTC sale can be made as a capital allocation decision independent of Bitcoin conviction, and that the relevant question for treasury companies is under what conditions a sale would be the most profitable move.

| company | BTC action | Size of impact of sale/holding | Why BTC was used | what it informs |

|---|---|---|---|---|

| strategy | Publicly normalized potential BTC sales | held 818,334BTC As of May 3rd | If the increase is expected to be greater than the issuance of shares, there is a possibility of selling BTC to raise dividends. | BTC is now part of the corporate finance toolkit, not just a reserve asset |

| Continue | Selling BTC while under operating and debt pressures | BTC holdings fall 1,514 From March 31st 1,114 April 30th | Debt redemption and ADS repurchase | BTC becomes liquid as revenue declines and debt matures |

| Mara | Selling BTC for liability management | sold 15,133BTC about $1.1 billion | Buy back convertible bonds and reduce debt by approximately 30% | Selling BTC can be seen as balance sheet optimization, not just distress. |

what the shift decides

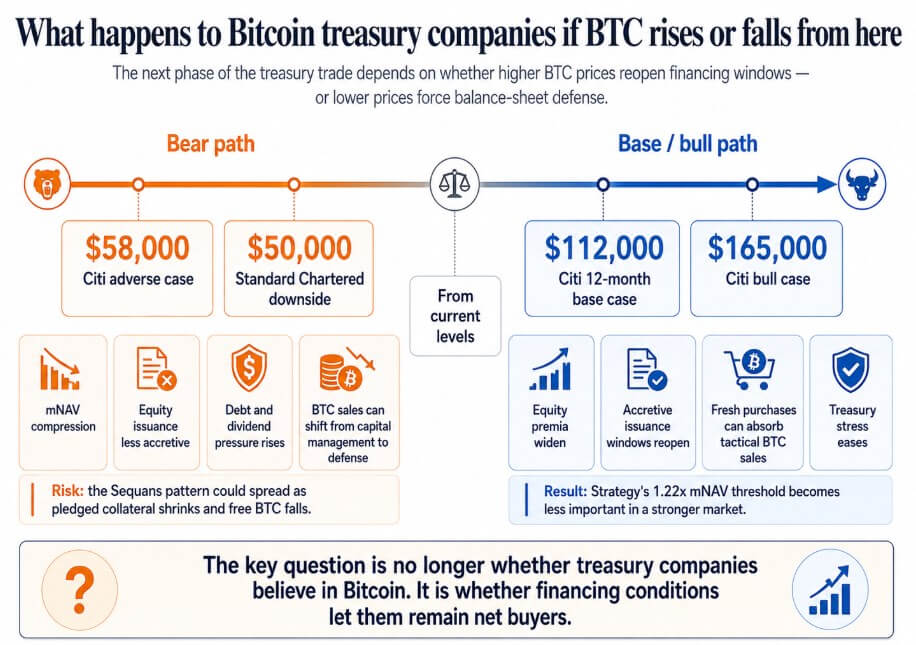

If Bitcoin recovers towards Citi’s 12-month base case target of $112,000, or bull case of $165,000, the stock premium across treasuries will widen, incremental issuance will be reinstated, and larger new purchases will absorb tactical BTC sales.

The strategy’s 1.22x mNAV threshold disappears into technical details, allowing second-tier companies facing debt stress through the Bitcoin market downturn to eliminate debt and hold unlimited BTC for the next cycle.

If Bitcoin heads towards Citi’s $58,000 downside, which Standard Chartered has flagged as a potential path to $50,000, companies trading near or below NAV will lose increased access to the stock market.

In this scenario, preferred dividend obligations increase and BTC sales shift from capital management to balance sheet defense.

The Sequans pattern could spread to treasury companies that combine thin operating income with BTC-backed borrowing, in which case the only response is to sell Bitcoin to pay off debt while posting collateral to reduce free float.

At that point, corporate Bitcoin bidding turns into a cycle in which falling prices trigger further selling, pushing the price down.

Corporate Bitcoin financial transactions are based on the promise of perpetual accumulation, making these companies recognizable to investors as Bitcoin agents.

Once selling becomes a tool in the model, investors need to factor in debt maturities, collateral requirements, dividend obligations, etc. mNAV threshold At this point, management may decide that selling stock will perform better than issuing stock.

Saylor’s breakeven 2.3% upside and 1.22x mNAV threshold are more honest. The next steps in Bitcoin Treasury trading will be determined as much by funding terms as Bitcoin’s conviction.

(Tag translation) Bitcoin