As tariff refund transactions move from court hypotheticals to Treasury Department accounts, the macro picture appears to be more significant than traders initially assumed, and traders are increasingly focused on whether this process can improve the macro outlook for Bitcoin prices.

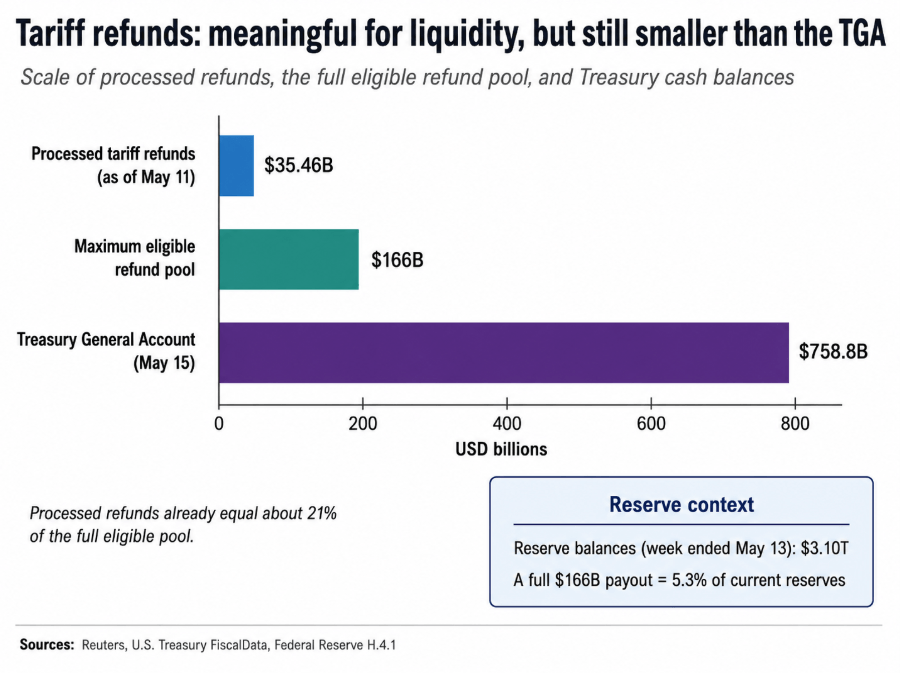

As of May 11, U.S. Customs and Border Protection had processed $35.46 billion in duty refunds, including interest, verified 86,874 claims covering 15.1 million entries, and completed 8.3 million shipments.

Up to $166 billion in IEEPA tariff collections are subject to repayment and paid to more than 330,000 importers across nearly 53 million imports, and the Supreme Court ruling stripped President Donald Trump of his authority to impose the tariffs.

The processed pool already represents about 21% of the potential maximum amount, and the remaining eligible volume is large enough to drive both reserves and pricing if payment is brought forward quickly.

Most of Bitcoin’s framework around redemption pools follows a path where funds flow out of Treasury general accounts, bank reserves increase, and risky assets are bid up.

Fed Director Christopher Waller’s balance sheet explanation supports this accounting, noting that when the Treasury makes payments, the Fed debits the TGA and credits the receiving banks’ reserve accounts, so refunds paid from existing cash balances increase reserves without issuing new issuance.

The TGA held $758.8 billion in reserves as of May 15, compared with approximately $3.1 trillion in reserves for the week ending May 13. The full payment of $166 billion represents about 5.3% of current reserves.

This change in liquidity is important because Bitcoin’s liquidity situation continues to be closely tied to reserve balances and movements in Treasury cash.

According to BofA’s public tariff commentary, the effective U.S. tariff rate will peak at 11.3% in October 2025, fall to 8.7% in March 2026, and the bank expects it to settle between 6% and 8% by the end of the year.

The bank believes the path to rate reductions is a supply chain event that could cause companies to delay future price increases, with pricing benefits flowing to company margins rather than consumer rebates.

Government refunds flow directly to importers, and the deflationary route goes through importers, supply chains, and future CPI statistics.

Why both channels need to work for Bitcoin price

Sustained inflationary pressures and rising Fed interest rates continue to shape the broader outlook for Bitcoin price appreciation.

CPI rose 3.8% in April compared to the same month last year, core CPI rose 2.8%, while energy prices rose 17.9% and gasoline prices rose 28.4%. March PCE was up 3.5% year over year, with a core value of 3.2%.

The Dallas Fed estimates that the tariff collection will increase the core PCE inflation rate by about 0.8 percentage points for the 12 months ending in March 2026, and the core inflation rate excluding tariff-related effects will be 2.3 percentage points.

EIA expects Brent crude to remain around $106 per barrel in May and June due to Strait of Hormuz disruption risks, and global crude oil inventories are expected to decline by an average of 8.5 million barrels per day in the second quarter.

| indicator | latest reading | Article relevance |

|---|---|---|

| CPI year-on-year change | 3.8% | inflation is still rising |

| Core CPI YoY | 2.8% | Underlying inflation remains above target |

| energy prices | +17.9% | Importers continue to face cost pressures |

| gasoline | +28.4% | Keeping inflation expectations sensitive |

| Core PCE YoY | 3.2% | Fed-recommended inflation indicators remain hot |

| Tariff contribution to core PCE | +0.8pp | We show you why refunds matter on margin |

| brent crude oil forecast | ~$106/barrel | Energy could offset tariff relief |

| Drewry Container Index | $2,553 / 40ft container | Fares absorb refund benefits |

Drewry’s World Container Index rose 12% to $2,553 per 40-foot container in the week ending May 14, driven by higher trans-Pacific and Asia-Europe rates. In that environment, we would first rebate cash flows towards energy and cargo absorption.

Bitcoin prices were trading around $77,507, below the 200-day moving average of about $82,000, and CoinShares recorded $982 million in Bitcoin product outflows for the week ending May 18.

With inflation still at a high level, the Federal Reserve kept its policy interest rate unchanged at 3.50% to 3.75% in April, and the market was pricing in the possibility of an extension of the policy rate or a rate hike.

A moderate disinflationary signal could ease the yield constraint on the margin, and any increase in reserves from TGA outflows would need to be supported by the yield backdrop, allowing liquidity to flow into risk assets rather than bond supply.

If both channels start

If the $125 billion to $166 billion refund is quickly processed primarily from existing TGA balances, the reserve injection would amount to 3% to 5% of the current balance, enough to shift the reserve optics without the need for new issuance.

At the same time, the Dallas Fed’s 0.8% tariff burden on core PCE begins to chip away at the margins as importers absorb higher freight and energy costs and deploy rebates to keep price hike schedules off track.

Given that BofA still sees services and energy as driving the majority of inflation, even a partial reversal of their contribution, with a realistic base case of core PCE mitigation of around 5-15 basis points, would be enough to ease the yield path that has limited Bitcoin’s recovery.

In that scenario, Bitcoin price regaining its 200-day moving average near $82,000 would be a macro-driven trade, with reserve dynamics and inflation data driving the setup.

Refund Pool develops the Bitcoin argument through two simultaneous conditions. One is that TGA balances are falling faster than the Treasury can rebuild them through bill issuance, and that importers are gaining enough margin room to defer planned price increases.

Both results are reflected in the same Bitcoin price argument: lower yields, stronger liquidity in US Treasuries, and improved risk appetite across risk assets.

In a bear market, refunds can be delayed, legally challenged, or distributed unevenly among importers. Companies with the largest refund claims could direct cash toward repairing their balance sheets rather than fixing prices.

If the Treasury simultaneously replenishes the TGA through bill issuance, reserve balances would remain flat and the liquidity channel would close. Energy and services inflation will dominate the easing in prices, and core PCE could remain well above the Fed’s 2% target through the end of the year.

In that scenario, Bitcoin would still be a yield-sensitive risk asset, with yields still constrained by rising interest rates. BofA’s year-end core PCE forecast of 3.1% already factors in some of the tariff withdrawals, and even a fully processed $166 billion refund pool could land as expected.

| scenario | refund pass | inflation channel | liquidity channel | Impact of Bitcoin |

|---|---|---|---|---|

| bull case | $125 billion to $166 billion processed quickly | Importers delay price increases. Core PCE relief becomes visible | TGA declines, reserves increase by 3%-5% | BTC has a strong macro tailwind. 200-day average of $82,000 is key |

| basic case | $50 billion to $100 billion processed over several months | 5-15bps core PCE mitigation | Partial reserve increase, partially offset by issuance | Modest support, but yield is still needed to stabilize BTC |

| bear case | Refunds are slow, conflicting, or uneven | Companies hold cash as a margin adjustment. Service and energy dominate | Ministry of Finance restructures TGA through bill issuance | BTC remains yield-sensitive and vulnerable around $75,000-78,000 |

The market is pricing in an extension of the rate hike or an interest rate hike, and the financial situation is tighter than the provision figures alone indicate. Bitcoin outflows continue as BTC price maintains or loses the $75,000 to $78,000 support zone.

The refund pool is large enough to matter, but it will only provide a macro tailwind to Bitcoin prices if reserves grow faster than the Treasury can replenish them. Easing margins for importers would slow future price increases enough to give the Fed enough room to suggest an extension of the moratorium.

Tracking CBP’s weekly processing totals along with TGA balances and core product inflation records provides the most accurate real-time read of whether the two-channel paper is doing well or stalling at the last minute.

(Tag translation) Bitcoin