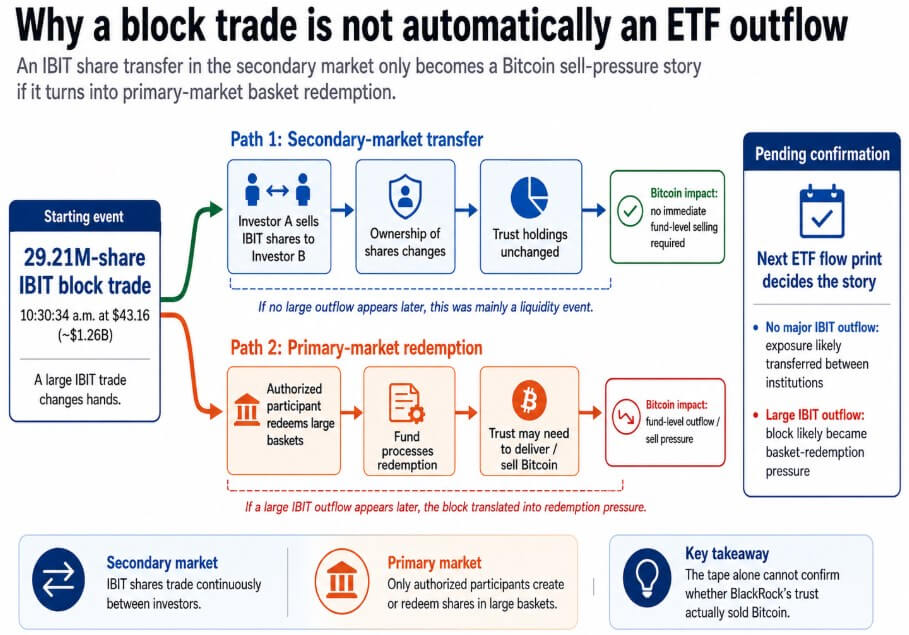

At 10:30:34 a.m. ET, a single IBIT print of 29,212,864 shares traded at $43.16, with a notional value of approximately $1.26 billion.

The next most visible move was 1.3 million shares, with one trade dwarfing all others in IBIT’s session, accounting for approximately 34.8% of the ETF’s reported intraday volume of 83.86 million shares.

IBIT rose approximately 0.09% to close at $42.99, while Bitcoin fell approximately 1.73% to trade at approximately $75,911. The dark pool executed the trade with a momentary 1% drop in Bitcoin, but quickly recovered, confirming that the block was absorbed through organized liquidity and settled cleanly.

With IBIT’s intraday volume of 83.86 million shares, there was enough daily volume for the market to absorb an issuance of 29.2 million shares without causing a chaotic price increase in the ETF, and the buyer or network of buyers matched the seller at $43.16.

Prior to the launch of the Spot Bitcoin ETF, moving $1 billion in Bitcoin exposure required either a large OTC desk arrangement or a series of exchange orders that left a measurable price impact across the crypto market.

Today’s block went through block desks, market makers, arbitrage desks, and authorized participants gearing up, with IBIT ending near where it started.

Differences in secondary market

IBIT stock is continuously traded in the secondary market between investors, and block trades between those investors change ownership of the stock, leaving the trust’s underlying Bitcoin holdings intact unless something else happens.

BlackRock’s fund documents state that IBIT shares are bought and sold in the secondary market and are not individually redeemable from the trust.

Only authorized participants, who are large financial institutions that interact directly with the Fund, may create or redeem shares in a large basket. This is done through a separate process that determines whether the trust actually sells the Bitcoin.

far side investor The May 26th IBIT flow line has not yet been populated, and confirmation of whether today’s block translated into a fund-level Bitcoin sell remains pending.

IBIT’s previous single-day withdrawal record was approximately $523 million, recorded in November 2025. If confirmed, an outflow comparable to today’s full notional size would more than double that record.

If IBIT does not report large outflows, a bulk transfer of exposure from one institutional holder to another will be a liquidity event limited to the secondary market.

If IBIT records large outflows, especially those that approach or exceed the all-time high of $523 million, that block will turn into pressure for basket redemptions.

Large holders may have used IBIT because they wanted to reduce their Bitcoin exposure and provided enough liquidity to move size cautiously. The buyer could be another institution rotating into Bitcoin exposure via an ETF wrapper.

This trade may also reflect portfolio rebalancing, basis trade unwinding, hedge adjustments, or mandate-driven allocation changes, none of which need to take into account Bitcoin price direction.

Piping under pressure

In the bullish case, ETF flow data shows no major outflows from IBIT, and today’s block confirms the depth of Bitcoin’s institutional market.

One institution reduced its exposure, another absorbed it through an ETF structure, taking spot Bitcoin off the exchange’s order book and keeping the ETF price intact.

This result supports the argument that Bitcoin’s market structure has matured by allowing the transfer of billions of dollars of exposure within the ETF pipeline.

Institutions looking to scale Bitcoin have a liquid and organized space to handle that volume, and the May 26th move is proof of that.

In the bearish case, IBIT reports large outflows in its next flow print, approaching or exceeding its previous record of $523 million.

This means that the block turned into redemption pressure in the basket as authorized participants returned their shares to BlackRock, the fund sold Bitcoin to match redemptions, and the ETF’s structure amplified and transmitted concentrated selling to spot price pressure.

The broader implication is that massive institutional de-risking can fuel redemption cycles and turn secondary market block trades into primary market Bitcoin sales in an order that tape alone cannot show.

Regardless of what the flow data confirms, today’s block has already demonstrated the depth of Bitcoin’s institutional infrastructure.

| scenario | ETF flow print | interpretation | meaning of market |

|---|---|---|---|

| absorption | No major IBIT leaks | One holder sells and another holder absorbs the stock | ETF market passes $1 billion liquidity test |

| Partial redemption | Outflow amount below record high | There is pressure from the primary market, but not a complete block conversion. | Mixed signals; secondary liquidity still absorbs some of the trade |

| Records leaked | Runoff from nearby or above $523 million | Blocks likely to translate into pressure for basket redemptions | Institutional investor risk aversion led to fund-level selling |

| extreme case | Outflow is nearing full $1.26 billion conceptual | More than double the previous IBIT withdrawal performance | This event could be reframed as a large-scale ETF redemption shock |

Approximately $1.26 billion worth of trades were completed in a single venue, and the ETF maintained its price, supported by the depth of IBIT’s order book, the liquidity of its block desk, and an arbitrage system that keeps the ETF’s price tied to its net asset value even under stress.

A block trade will only turn into deeper Bitcoin selling pressure if it appears in the next ETF flowprint. Previously, a cleaner interpretation was that a multi-billion dollar transfer of Bitcoin exposure occurred and the market absorbed it.