Hut 8 is further committed to AI infrastructure than most other Bitcoin miners. The latest disclosures show that a company has access to power, data center leases, project debt, $BTC-Backed liquidity to build the funding stack for the move.

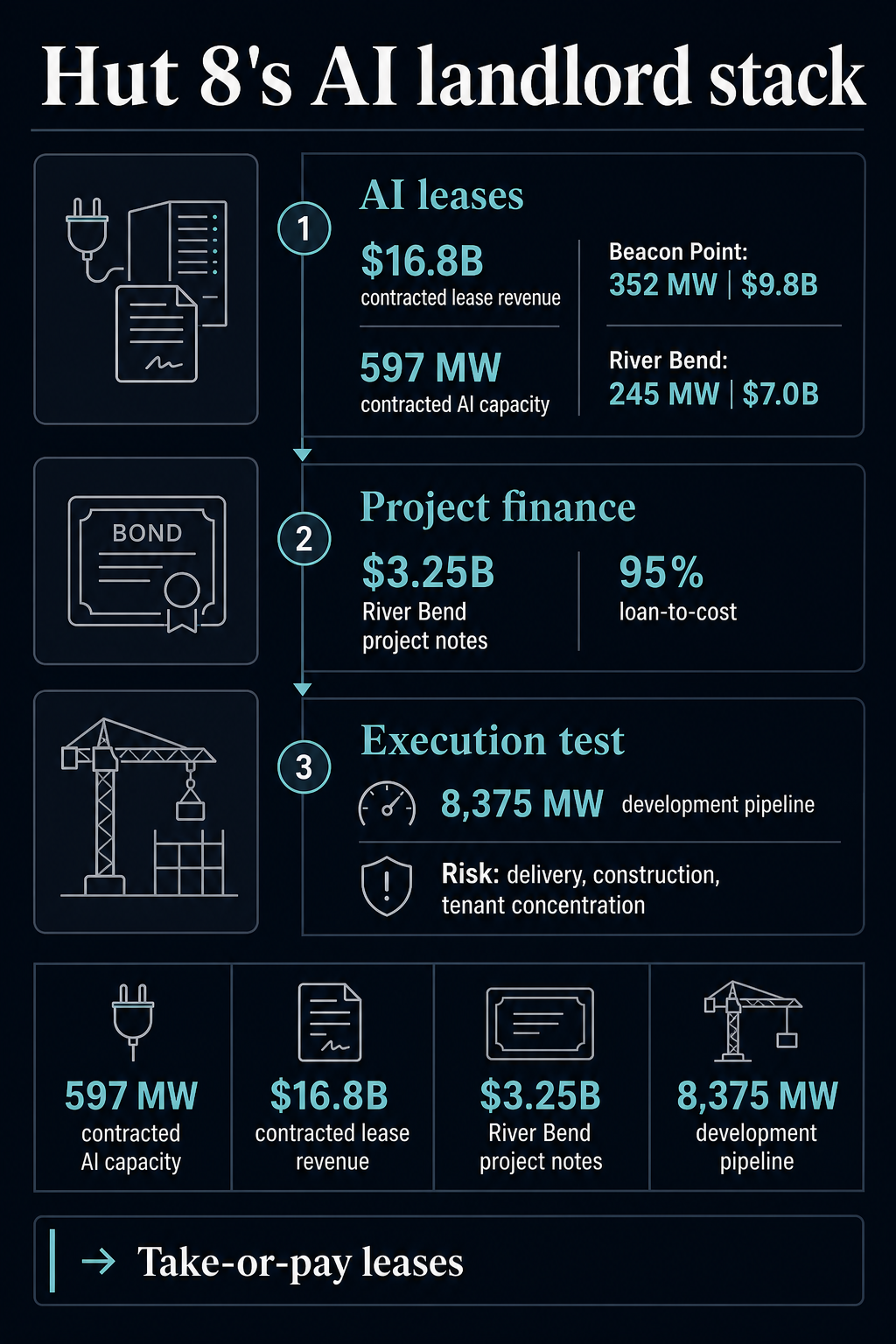

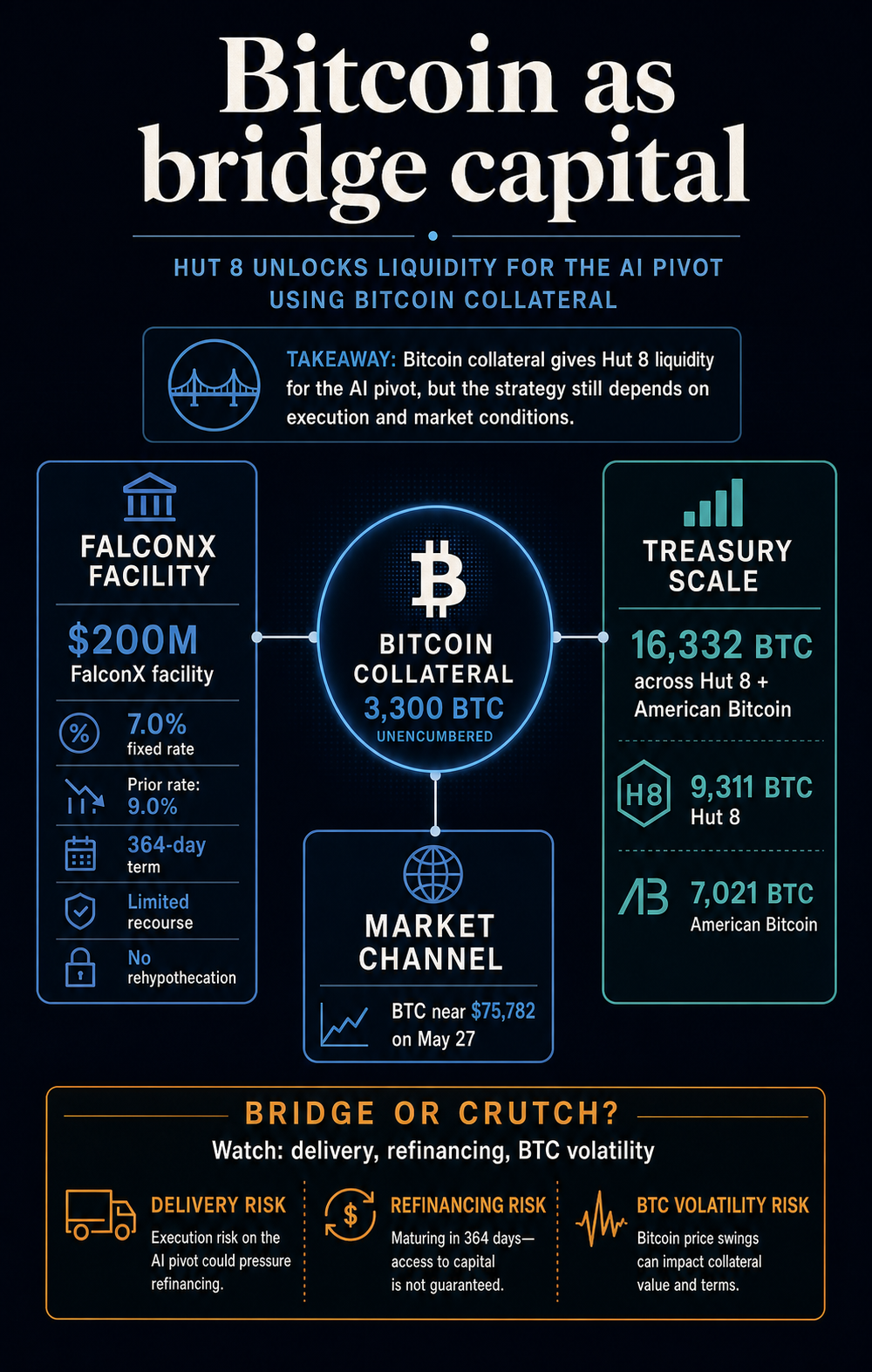

The company’s latest disclosure provides numbers on that transition. Hut 8 reported $16.8 billion in triple-net, take-or-pay lease revenue across its two hyperscale AI campuses, and subsequently refinanced a separate $200 million Bitcoin-backed credit facility to FalconX.

The new facility lowered the fixed interest rate from 9.0% to 7.0%, eliminating approximately 3,300 contributions. $BTC From the previous collateral package.

Taken together, these disclosures indicate that the identity of miners is changing to be more like the owners of the infrastructure. Hut 8 is turning megawatts, lease agreements, project debt, and Bitcoin holdings into a business machine that doesn’t rely solely on mining.

The result is a more substantial case study than the typical AI pivot. Although Hut 8 has received funding and points the way to data center infrastructure, this model still requires proof of operation. The test will be whether contracted AI cash flows arrive on time and are durable enough for Bitcoin collateral to become a bridge rather than a recurring source of dependence on the balance sheet.

Lease bases turn electricity into finance

The strongest numbers in Hut 8’s first quarter disclosures come outside of the first quarter income statement. That’s $16.8 billion in contracted lease revenue across River Bend and Beacon Point, covering 597 MW of AI data center capacity.

Hut 8 had revenue of $71 million in the first quarter, including $66 million from computing, and a net loss of $253 million, primarily including $295 million in unrealized losses on digital assets.

The $16.8 billion figure represents the amount of long-term leases Hut8 is offering as the basis for another type of business.

The work is concrete. Hut 8’s Beacon Point lease added 352 MW of IT capacity and $9.8 billion in base period value. The previous Riverbend lease added 245 MW and a base term value of $7 billion, with Google providing a financial backstop for the base lease term.

Hut 8 commercializes scarce power and data center capacity under long-term lease structures. This appeal comes from contracts and access to power, not tokens, cloud slogans, or vague promises of computing.

Triple-net terms and take-or-pay terms are designed to make these cash flows easier to finance, as tenant obligations are less tied to day-to-day mining economics.

Hut 8 disclosures span four moving parts:

Hut 8’s AI transition includes more elements than many other components, but each component still carries different types of risks.

Leases reduce some income uncertainty. Debt financing alleviates some funding pressures at the parent company level. Bitcoin functionality increases liquidity. Still, all three have left Hut 8 with the task of building, delivering, and operating infrastructure for customers with different requirements than Bitcoin mining.

Bitcoin becomes a bridge capital

FalconX’s refinancing is the clearest sign that Bitcoin is becoming part of the financing system, not just an asset to be mined.

Hut8’s full release, distributed through Nasdaq, describes the facility as a 364-day Bitcoin-backed loan with limited security. $BTCno rehypothecation execution, fixed loan-to-value criteria, and no loan-to-value ratchet caused by falling Bitcoin prices.

These terms blunt some of the obvious criticisms. The agreement improves miners’ coin-backed borrowing terms, rather than making them worse in order to chase new markets.

Hut 8 reduced the fixed cost of debt by 200 basis points and increased Bitcoin holdings outside of collateral terms. The release states that the newly unencumbered coin will be worth approximately $260 million as of May 1, 2026, allowing Hut8 to free up space on its balance sheet without having to sell any assets.

This makes this facility a better tool, but it is not without risks.

Hut 8’s own balance sheet shows why this distinction is important. In the 10th quarter, it was announced that the company held approximately 16,332 shares. $BTC As of March 31, 2026, including approximately 9,311 people $BTC Owned by Hut 8, approximately 7,021 people $BTC Owned by American Bitcoin.

Total fair value is approximately $1.11 billion, based on approximately $68,222 per transaction. $BTC. The same filing tied digital asset losses in the first quarter to Bitcoin’s decline over the same period.

Bitcoin is currently trading around $75,782 on CryptoSlate’s price page, down 2.1% in 24 hours and about 40% below its all-time high in October 2025. The market price channel is the relevant risk.

While Bitcoin can provide liquidity without being sold, the borrowing value, contractual security, and refinancing context will still depend on the asset’s market trends.

This is why an AI landlord strategy cannot be separated from a Bitcoin financial strategy. If AI leasing generates reliable cash flow, $BTC Collateral can be a transitional fund. If deliveries are delayed, financial markets tighten, or Bitcoin falls at the wrong time, the same collateral could leave the pivot tied to the volatility it was meant to avoid.

Minor labels are becoming less useful

Previous coverage of the miners’ AI pivot demonstrated the broader identity divide facing the sector. Miners are moving toward AI and high-performance computing because power access, cooling infrastructure, land, interconnection works, and industrial operations can be worth more under contract dollar income than compressed mining margins.

Hut 8 fits into that broader sector change. Public miners built their businesses around converting electricity into electricity. $BTCThe demand for AI data centers is giving some data centers the possibility of a second use of the same physical footprint.

The difference is that AI customers do not buy the same things that the Bitcoin network buys. Mining can tolerate interruptions if economic or grid conditions change. AI tenants demand uptime, certainty of delivery, dense power, cooling, network architecture, and trusted execution.

Miners with megawatts still have to become hyperscale landlords. Positions of power need to be transformed into infrastructures that lenders and tenants treat as trustworthy.

Hut 8’s disclosure shows both sides of that transition. The company describes itself as an energy infrastructure platform that integrates power, digital infrastructure, and computing. They are also still reporting losses in digital assets. $BTC Asset holdings and exposure to the mining economy.

Some computing revenue and $BTC Since the assets are held by consolidated subsidiary American Bitcoin, Hut8’s strategy is not as simple as withdrawing from mining altogether.

That complexity is part of the change. The market is watching to see if miners can stop being pure. $BTC They can send agents without losing the discretionary nature of the balance sheet that made the Treasury so valuable in the first place.

The strongest argument in favor of Hut 8 is that AI Pivot uses more than just Bitcoin-backed debt. The company announced that it has closed $3.25 billion in investment grade senior secured notes fully amortizing over 16.5 years to finance River Bend.

Hut 8 described the financing as a non-dilutive and non-recourse to Hut 8, increasing the loan-to-cost ratio to approximately 95%.

That weakens the crutch argument. If project-level debt funds the campus and long-term leases support the debt, the Bitcoin collateral becomes part of the structure rather than the entire structure. It is a liquidity tool alongside project finance and contract revenue.

It should be noted that the financial structure still needs to be operationally sound. Riverbend is still progressing toward delivery, Beacon Point still needs construction, and the company still needs to convert its 8,375MW development pipeline into actual contracted capacity.

Hut 8 also warned investors about risks related to data center construction, financing, power expansion, permitting, supply chain, technical challenges and market conditions.

Hut 8 shows that miners can fund routes to AI infrastructure with no electricity, reliable tenants, access to project finance, and a Bitcoin balance sheet underwritten by lenders. It remains to be shown whether this route can be self-sustaining.

The next test will be whether the AI infrastructure cash flows will be strong enough to force Bitcoin collateral into the background. Then Hut 8’s $BTC-backed financing will look like bridging capital for miners who have successfully monetized their power generation.

Failing that, the pivot remains tied to the same balance sheet assets that made the strategy possible in the first place.