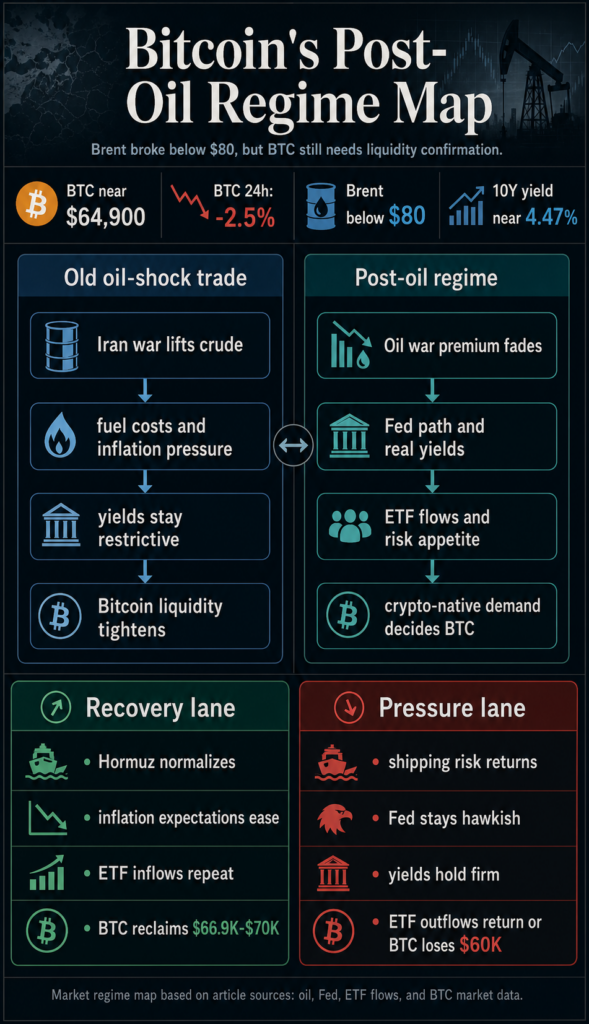

Bitcoin is falling as Brent crude oil trades below $80 after the US-Iran peace deal.

The oil shock that dominated Bitcoin macro trading in 2026 has eased, but Bitcoin is still trading around $64,900, down about 2.5% in 24 hours on firememecoins’s Bitcoin price page.

The decline in Brent could have given risk assets a cleaner relief trade. Instead, the following problem became apparent:

The market has moved beyond the simple oil up, Bitcoin down model. Low oil prices remove the bearish factor. Restoring liquidity support will need to come from interest rates, ETF flows, and risk appetite through the end of 2026.

Global oil prices fell below $80 for the first time since the start of the Iran war, after a framework between the US and Iran hinted at reopening the Strait of Hormuz. Ships were still unable to pass through the choke points normally, and the operational effectiveness of the peace agreement remained unresolved.

President Donald Trump’s public message that the Iran deal is done has prompted traders to remove some of the war premium from crude oil. Bitcoin’s reaction will revolve around liquidity, interest rates, risk appetite, ETF demand, and the willingness of crypto buyers to intervene in the wake of geopolitical pressures.

oil moves to background

In the past, Bitcoin transactions were consistent. Rising oil prices due to the Iran war could have sent fuel costs up through the supply chain, kept inflation expectations high, delayed the Fed’s interest rate cuts and depleted oxygen for risk assets.

This early hydraulic set-up was already evident when Bitcoin fell as financial conditions tightened due to rising oil prices, rising yields, and extinguished expectations for interest rate cuts. Oil was the first signal because war was the fastest way to get to inflation, yields, and the Federal Reserve.

The same point was made by the opposing side regarding the framework for restoring the Iran deal. A peace framework could help Bitcoin only if lower oil prices translate into real oil flows, lower gasoline prices, less inflation compensation, and Fed policy less hostility towards risk assets.

The first link in the confirmation chain has been moved. Oil prices have fallen and Bitcoin can no longer be traded like an asset with a clear recovery path to the upside.

Oil has moved from being a major driver to a background risk. Oil could still negatively impact Bitcoin if Hormuz traffic fails to normalize or if energy markets reassess the disruption. If oil prices continue to fall without improvements in Fed expectations, ETF flows, and risk appetite, the reason for Bitcoin to rise will diminish.

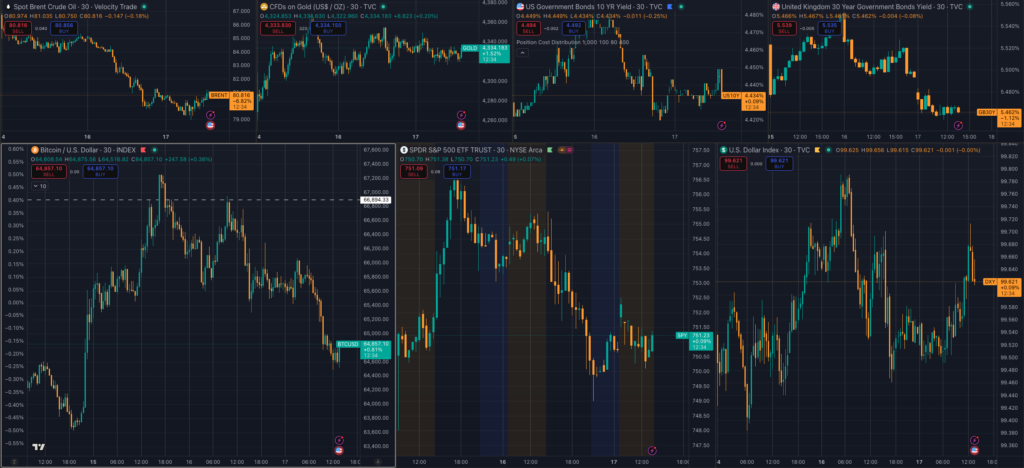

The Fed remains central. Energy-driven inflation risks remained top of mind in April’s FOMC meeting minutes, with the latest visible data showing the 10-year Treasury yield at about 4.47%.

This is a limiting backdrop for non-yielding assets that still trade like high-beta liquidity even during periods of stress.

The next Fed communication is placed directly on that path. Bitcoin needs the market to believe that low oil prices will give policymakers room to stop risk aversion.

A hawkish message from the Fed, persistent inflation rhetoric, or even a further push in real yields could make the peace deal look more like an oil market event than a Bitcoin liquidity event.

That is why the lower oil painting imposes a different burden of proof on Bitcoin. The next confirmation needs to come from the parts of the market that set liquidity: Fed communications, Treasury yields, dollar pressure, equity risk appetite, ETF flows, and derivatives positioning.

Liquidity will be a year-end test

Bitcoin ETF flow data showed small daily positive flows on June 16th, but the magnitude is too small to explain the entire regime shift.

Previous coverage of ETF Flows showed how institutional demand can quickly turn from support to stress point when oil, interest rates, and risk appetite move against Bitcoin.

That’s why your year-end path relies more on repetition than on a single green ETF investment. Bitcoin needs a few sessions of falling oil prices, combined with steady ETF demand, lower yields, and increased risk appetite.

Without this combination, the market may interpret the latest inflows as a pause in risk aversion before a new allocation cycle begins.

Crypto-native liquidity is the final test. According to CoinGlass data, BTC open interest and futures volume were large enough to correlate positioning to short-term price movements.

The directionality again depends on the catalyst. Surprises from the Fed, ETF desks, or the stock market can be transmitted quickly through leveraged positioning.

| signal | oil shock regime | post oil regime |

|---|---|---|

| first market question | Will oil keep inflation and yields high? | Will low oil prices meet the Fed’s expectations and risk appetite? |

| Bitcoin pressure points | The company’s financial situation became tight due to rising energy costs. | Weak liquidity and uneven ETF demand will limit recovery. |

| confirmation signal | Hormuz flow, gasoline, CPI, Fed pricing. | Continuous ETF inflows, falling yields, downward pressure on the dollar, risk-on stocks. |

| failure signal | Crude oil stress has flared up again and there is no way to cut interest rates. | BTC loses $60,000 and yields rise or ETF outflows return. |

The baseline scenario for the remainder of the year is for a fragile, liquidity-driven recovery.

This is a more cautious view than the oil chart alone suggests. Brent below $80 removes one of the biggest bearish factors heading into 2026, but Bitcoin still needs to rebuild its demand side.

The asset could recover if low oil prices reduce inflation expectations, lower yields, and ETF flows shift from temporary positive days to steady demand.

The recovery lane is easy. Hormuz traffic has normalized, gas pressure has eased, inflation compensation has fallen, and the Fed has enough cover to make it sound like restrictions are easing.

At the same time, Bitcoin ETF flows stabilize, spot demand improves, and BTC regains the $66,900-$70,000 ledge that was highlighted in recent market structure coverage.

In this lane, oil’s job is to prevent liquidity transactions from being blocked. Once the conflict between interest rates and flows ceases, we will see an upside as capital returns to Bitcoin as a rare, liquid, risk asset.

The pressure lane is clear as well. Oil prices could be revised if the peace framework stalls in its implementation, tanker traffic remains backed up, or shippers and insurers lose confidence in the route.

Even with low oil prices, Bitcoin could remain locked in if the Fed removes easing expectations, US Treasury yields hold firm, and ETF flows return to redemptions.

That’s a key shift. Liquidity and risk appetite are now driving trades. Bitcoin’s next move will depend on whether the market views the peace deal as a true disinflationary shock or a crude reset that leaves interest rates, dollar pressure, and ETF demand unresolved.

Liquidity and risk appetite outperformed oil for the remainder of 2026. The Bitcoin bull thesis is still alive, but it’s now on the desks of the Fed and ETFs, showing crypto capital’s willingness to buy on the push after the war premium has already emerged from oil.

(Tag translation) Bitcoin