BlackRock’s iShares Bitcoin Trust has become the test Bitcoin bulls didn’t want. ETFs, which helped transform regulated access into a simple institutional demand narrative, are now the primary place where price-sensitive holders emerge.

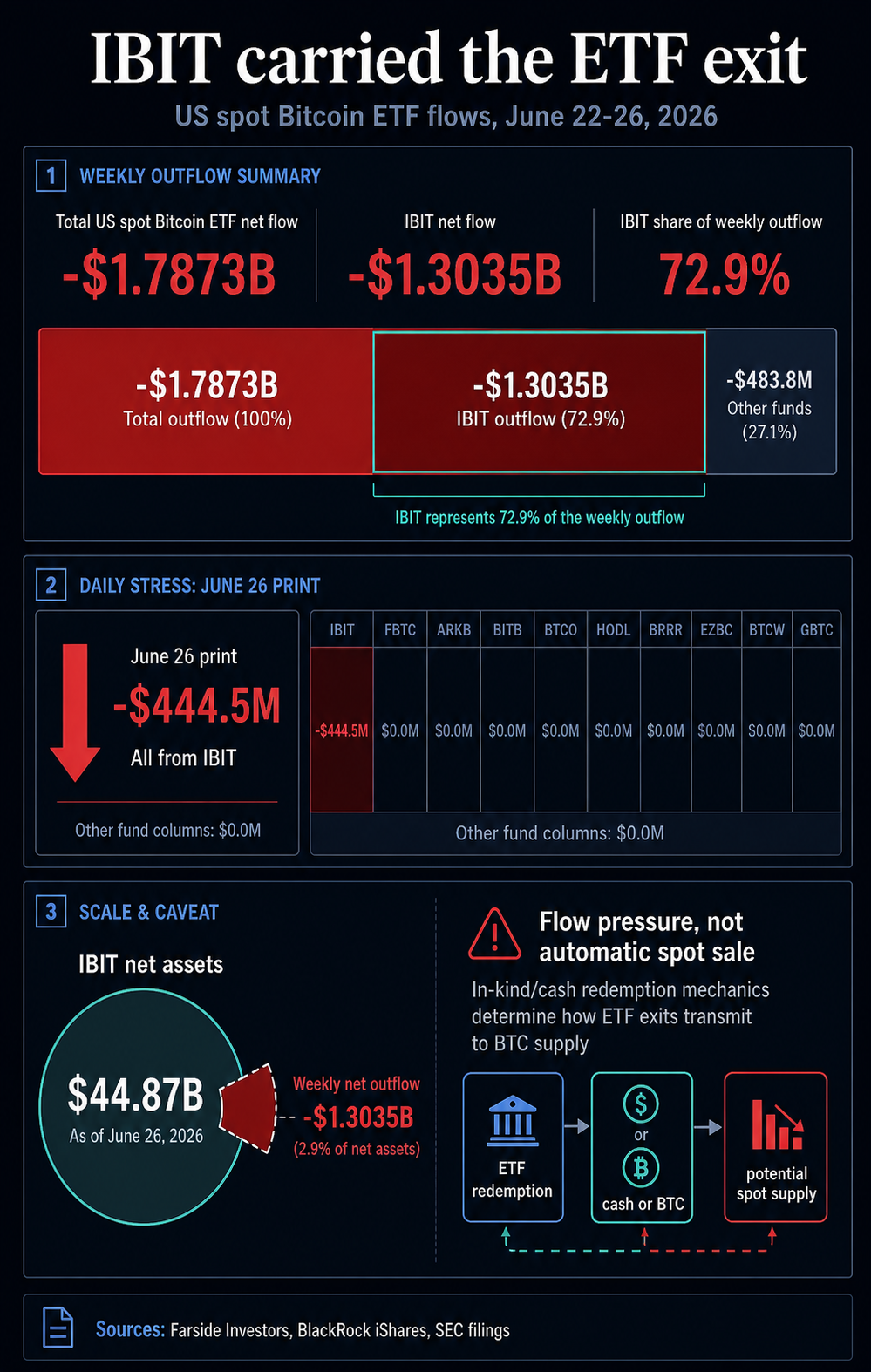

U.S. spot Bitcoin ETFs lost about $1.79 billion in the trading week of June 22-26, according to Bitcoin ETF flow data from Pharcyde Investors. IBIT accounted for approximately $1.3 billion of this total and nearly 73% of weekly exits.

The latest daily line made that signal clear. Pharcyde’s June 26 table shows net outflows from the ETF complex of $444.5 million, with all of the negative portion coming from IBIT.

The recovery test changes depending on its concentration. Bitcoin can still treat the ETF complex as a demand channel, but the largest spot Bitcoin ETF should also be treated as a redemption channel.

If the same wrapper that validated Bitcoin for brokerage account buyers becomes the primary exit lane, spot buyers outside the ETF complex will have to absorb exposure as ETF holders reduce risk.

IBIT executed an ETF exit

Far-side data turns this week into a market structure signal, as pressure is concentrated on the market’s most visible Bitcoin ETFs.

| flow measurement | June 22-26, 2026 |

|---|---|

| US Spot Bitcoin ETF Total Net Flows | -$1,787.3 million |

| IBIT Net Flow | -$1.335 billion |

| IBIT’s share of weekly outflows | Approximately 72.9% |

| Total ETF net flows on June 26th | -$444.5 million |

| IBIT net flow on June 26th | -$444.5 million |

IBIT is more than just a ticker in an ETF complex. This is one of the most clearly regulated access points for Bitcoin through existing brokerage accounts, and its size means its flows carry more weight in the market than redemptions from smaller funds.

Once that product becomes a large portion of the weekly exits, the signals won’t just cool across the ETF market. This is the strongest access rail Bitcoin stress test from the Spot ETF launch.

This flow also landed while Bitcoin was already under pressure. According to firememecoins market data, BTC was trading around $60,000 on June 28th, with negative 7-day and 30-day performance.

Recent firememecoins coverage tracked the already broad ETF decline and Bitcoin’s struggles in the high $50,000 to low $60,000 zone. Now, the added pressure is that IBIT itself will become a noteworthy marginal stream.

The story of early spot ETFs was straightforward. Regulations on access widened the buyer base, demand for ETFs reduced available supply, and Bitcoin gained ownership rails more accessible to institutional and brokerage account investors.

The latest data shows that the same access points can work in reverse if ETF holders decide to exit, while keeping its history intact.

The size of IBIT is why the outflow week is so important, and it always predicts trends. BlackRock’s official iShares product page lists IBIT’s net assets as $44.87 billion as of June 26, with a benchmark level of around $59,813.

The $1.3 billion in weekly outflows is large enough to dominate the ETF complex, but it’s still only a fraction of the fund’s asset base. IBIT remains the primary regulated Bitcoin wrapper. The question for markets is what to do with their size.

As IBIT raises capital, its size strengthens the institutional demand narrative. When a loss occurs, its size makes it difficult for the rest of the market to ignore the spill.

Smaller funds can bleed without changing the overall argument for ETFs. This is not possible with IBIT. That redemption suggests that the ETF’s holdings are becoming more price sensitive near Bitcoin’s support zone.

The main difference is around $60,000. A constructive interpretation is that the largest redemptions have already passed through the system, outflows will then slow, and recoveries in the $59,000 to $62,000 area appear to be absorbed.

A cautious interpretation is that the next rally will have to withstand fresh ETF selling pressure, rather than simply recovering from a liquidation flush.

This is a sell-wall version of the IBIT story. There is no need for BlackRock to become bearish on Bitcoin, and there is no need for IBIT holders to exit en masse. This is a market structure argument. That is, the highest access products may be where price-sensitive ownership appears first.

How ETFs work keeps claims accurate

ETF flow data is a pressure signal rather than a direct on-chain sales log.

In July 2025, the SEC authorized the physical creation and redemption of virtual currency ETPs. IBIT’s filing also indicates that the redemption mechanism could include cash proceeds from the sale of Bitcoin or Bitcoin itself, depending on the route used.

Therefore, ETF outflows should be treated as a contagion risk, rather than as automatic evidence that all redeemed dollars were immediately sold to the spot market.

The risks are still real. Large liquid ETFs can turn investor risk aversion into a recurring source of pressure on Bitcoin supply or supply expectations, especially if redemptions are settled in cash or if redeemed Bitcoins are subsequently sold.

The market does not require complete mechanical certainty for a signal to matter. If IBIT continues to print significant negative days, buyers will need to ask who will absorb the exposure as it leaves the ETF wrapper.

If Bitcoin is unable to regain the $60,000 region while that happens, the old institutional demand story will weaken. If the flow stabilizes quickly, the same data may appear to be reset after the congested trade clears.

The real test is whether the ETF’s holdings have matured into a two-way source of price pressure. Spot ETFs have made it easier for investors to take ownership. Easier ownership means easier termination.

IBIT’s latest week of outflows has favored this trade-off over Bitcoin, which is at a vulnerable point on the chart.

If IBIT’s outflow is slow and Bitcoin sustains the low $50,000 range before reclaiming the $59,000-$62,000 band, the week can be treated as a potential capitulation or flow reset.

In that version, ETF holders who wanted to exit did so, the market absorbed the contagion risk, and the largest regulated product remained net positive for Bitcoin in the long run.

The interpretation changes if IBIT continues to dominate redemptions while Bitcoin cannot rebuild above $60,000. The ETF complex will define the next recovery test by requiring non-ETF spot buyers to defend the market without the help of the wrapper that once provided the easiest bullish story.

The latest IBIT-led withdrawal leaves Bitcoin with a real test rather than a firm verdict. One week’s worth of flow data does not establish investor motivation, and the redemption mechanism thwarts the argument for a simple dollar-for-dollar spot sale.

However, the data shows that the most visible Bitcoin ETF on the market could become the dominant source of outflow pressure at the very moment Bitcoin needs demand outside of the ETF complex.

In the case of Bitcoin, the next few trading sessions will be unusually important. If IBIT bleeds slowly, it will be a sign of exhaustion for the week. Another large redemption would make the sell wall framework difficult to ignore.

(Tag translation) Bitcoin