Digital asset markets entered a more defensive phase as Bitcoin fell below the $60,000 mark, ending months of tight trading and exposing traders to market structures that could fuel the next big move.

crypto slate The largest cryptocurrency had been flat since February, when it first tested the $60,000 area, according to the data.

This prolonged consolidation has made the level a widely watched indicator for traders, even as concerns over macro risks, physical exchange-traded fund outflows, and corporate Bitcoin holders weighed on prices.

As a result, the recent decline points to a more vulnerable situation, with large amounts of Bitcoin moving to major exchanges, open interest rising while spot prices remain depressed, and professional traders paying more to protect against further declines.

Bitcoin breakout turns currency flows into a supply test

The most obvious signs of stress are in currency-related flows.

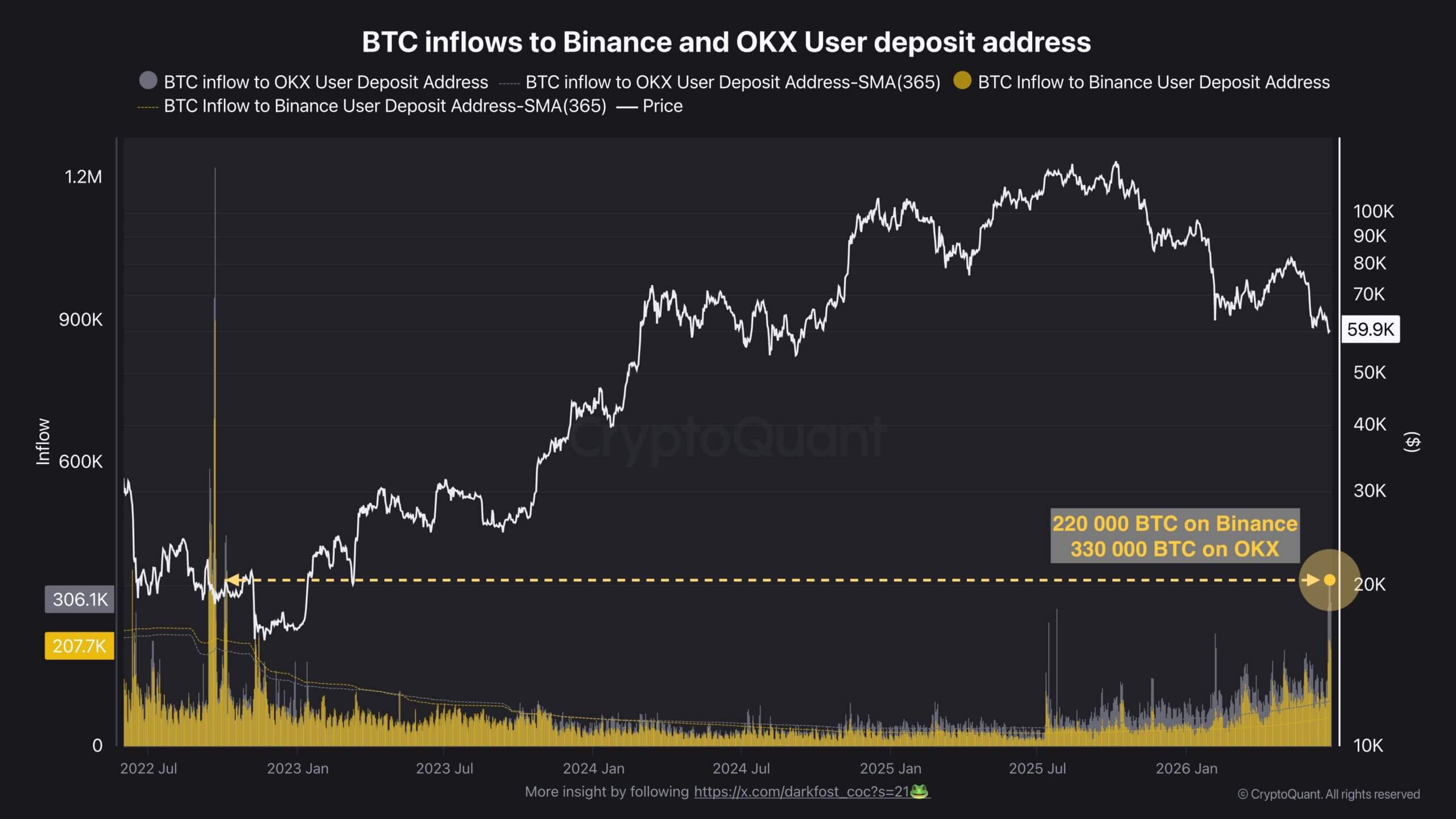

According to CryptoQuant data, more than 550,000 BTC moved to deposit addresses linked to Binance and OKX after Bitcoin fell below the $60,000 area. Deposit addresses linked to Binance received over 220,000 BTC, and addresses linked to OKX received over 330,000 BTC.

These numbers are far above normal measurements this year. According to CryptoQuant data, comparable inflows for Binance average around 60,000 BTC, while OKX averages around 95,000 BTC.

The latest transfers are the biggest this year and similar to levels last seen during the 2023 bear market.

In the architecture of cryptocurrency markets, a sudden transfer of coins to an exchange deposit address serves as the first operational indicator of intent. Users typically route their assets to these specific points before the funds are aggregated into the platform’s central hot wallet for execution, lending, or collateral allocation.

Still, timing makes the data more important. Large sums of money directed towards exchanges during times of falling prices often raise concerns that more supply will become available if the market falls further.

A potential oversupply could make it difficult to sustain a rebound in a market that is already trading below levels that many investors have been watching for months.

This trend reflects how volatile markets can become when they break out of familiar levels. If a trader spends months reacting to the same zone, risk management, hedging, and stop-loss decisions can become concentrated around that zone. When levels break down, many participants simultaneously reassess their exposure.

Exchange data is therefore central to the current setup. The market isn’t just dealing with a drop in Bitcoin prices. It also addresses the possibility that more coins are moving closer to venues where holders can act quickly.

Valuation reset reduces excess risk but not volatility risk

Exchange flows are coming as Bitcoin’s on-chain metrics show that much of the excess from the initial cycle has already been compressed.

CryptoQuant’s MVRV Z-score shows that Bitcoin’s valuation premium has fallen sharply and is approaching historic low valuation territory.

The MVRV framework compares Bitcoin’s market value and realized value. Market value reflects the current price of coins in circulation, while realized value estimates the total cost basis of the network by valuing each coin at the last price it moved on-chain.

When market value trades far above realized value, unrealized gains typically increase and cyclical risk tends to increase. As the gap narrows, profitability declines and speculative pressures are alleviated to some extent.

The Z-score moderates that relationship by measuring the distance between market value and realized value relative to Bitcoin’s historical market capitalization deviation. This helps traders determine whether Bitcoin is trading at a valuation level that is close to an abnormally extended valuation level or a compressed valuation level relative to its history.

Current numbers suggest that the market is approaching reset territory.

However, the indicator does not identify the exact bottom price. Bitcoin has historically traded near cheaper valuations, especially when prices have continued to fall during periods of illiquidity, forced selling, or macro stress.

This distinction is important now because valuation and positioning send different messages. On-chain data suggests the market is less tense than earlier in the cycle. Market structure data suggests traders are still bracing for disorderly moves.

CryptoQuant data shows that while funding rates on major exchanges are back in positive territory, Bitcoin remains languishing around $59,000 to $60,000. Positive funding typically means traders with long positions are paying short, indicating a return in demand for bullish exposure after a more negative development.

At the same time, spot prices remain weak, but open interest is rising. This means that new positions are being built in decline rather than risking exit from the system.

This combination can make it more sensitive to price fluctuations. If Bitcoin falls further, newly opened long positions could come under pressure. If the market rebounds sharply, traders could be forced to cover against further declines.

With either outcome, the next move could be bigger than the spot market alone suggests.

Downside hedges built as institutional investor interest wanes

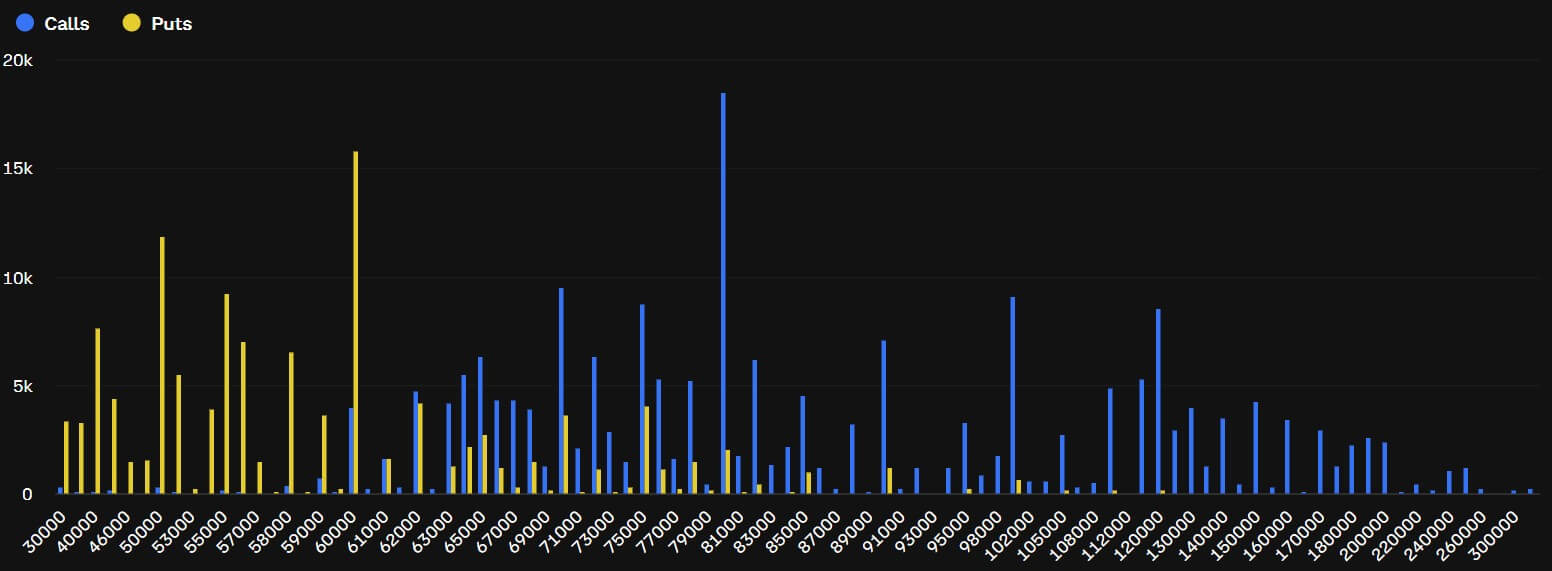

To manage this heightened structural uncertainty, institutional investors are actively building defensive positions in the options market.

Singapore-based digital asset trading firm QCP Capital reports that the implied volatility index is trending systematically upward as market participants pay a premium for downside protection.

Demand is focused on Bitcoin put options expiring in July with strike prices between $55,000 and $58,000, the company said.

Data from digital asset derivatives exchange Deribit reinforces this story, showing that around $1.2 billion of open interest is specifically concentrated in the $55,000 and $50,000 strike zones.

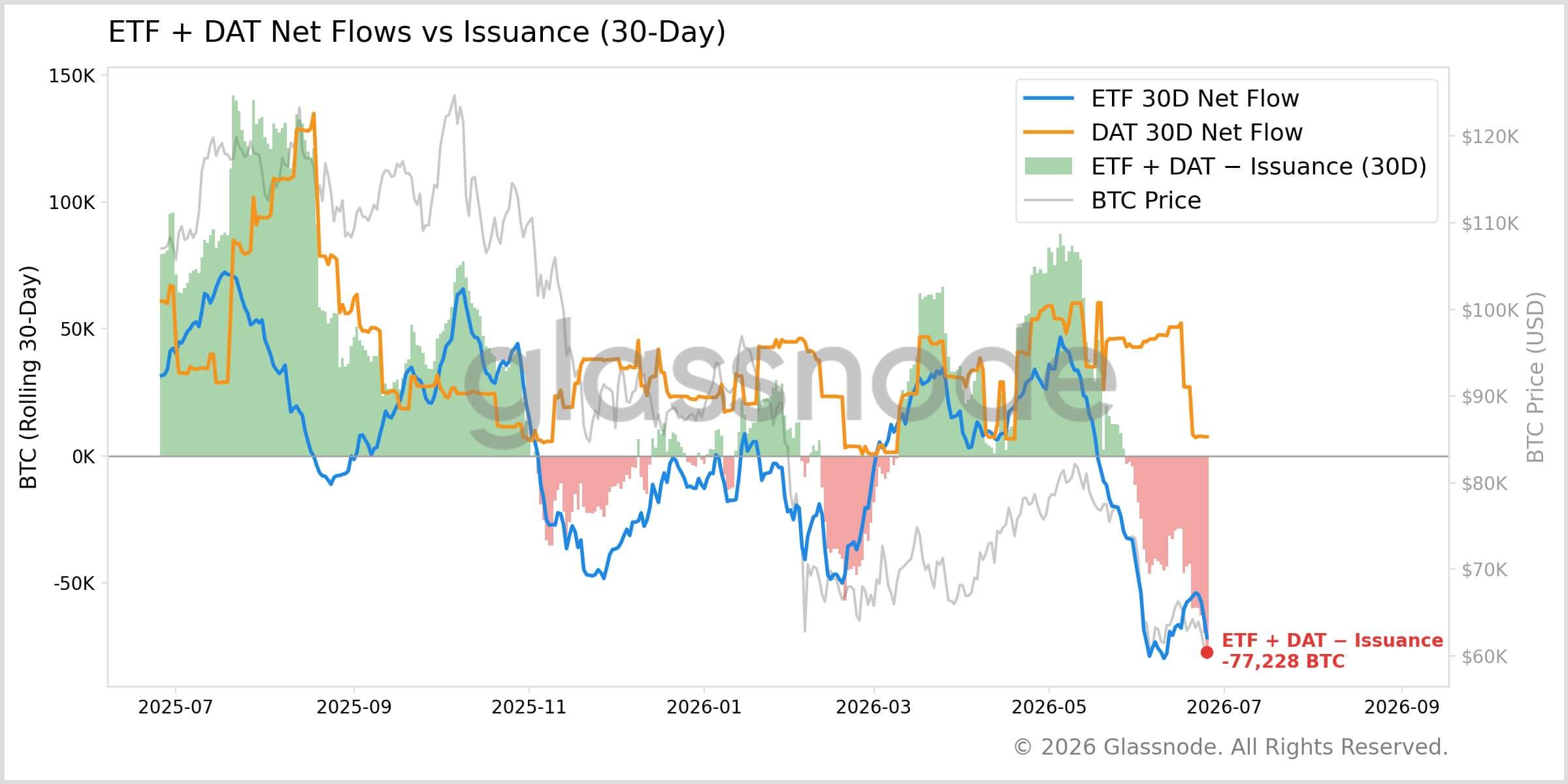

Compounding this defensive position are structural changes in the flow of capital from institutional investors.

Data from blockchain analytics firm Glassnode reveals that institutional demand is no longer acting as a reliable sponge to circulate supply. Over the past month, the physical Bitcoin exchange-traded fund (ETF) has decreased by approximately 71,600 BTC, while the digital asset trust has increased by only 7,500 BTC.

Adjusting for network issuance, the total net institutional capital flow is -77,000 BTC.

According to Glassnode analysis, any near-term spot market recovery will immediately face friction from this persistent wrapper supply glut until net flows reverse.

This trend of institutional deleveraging has been clearly quantified by BlockScholes, whose proprietary Bitcoin Risk Index has been anchored below the -1.0 threshold for more than 23 consecutive days.

Brock-Scholes notes that this prolonged trend signals a break from typical cyclical declines and suggests continued structural risk reduction by institutional allocators, which will likely require fundamental macroeconomic and industry-specific catalysts to change.

This leaves Bitcoin in a vulnerable position even after it falls below the $60,000 area. On-chain valuation metrics suggest that the market has already significantly reduced initial excess, but currency flows, options positioning, and institutional demand all indicate that the market is still bracing for stress.

The immediate test will be whether spot demand can absorb the supply near exchanges. Defensive positioning could help rebound if demand improves.

Otherwise, the same structure could turn a breakout of $60,000 into a broader shock to volatility.

(Tag to translate) Bitcoin