Strategy’s biggest Bitcoin sale in years has put new pressure on the corporate financial model that has made Michael Saylor one of the hottest names in digital assets.

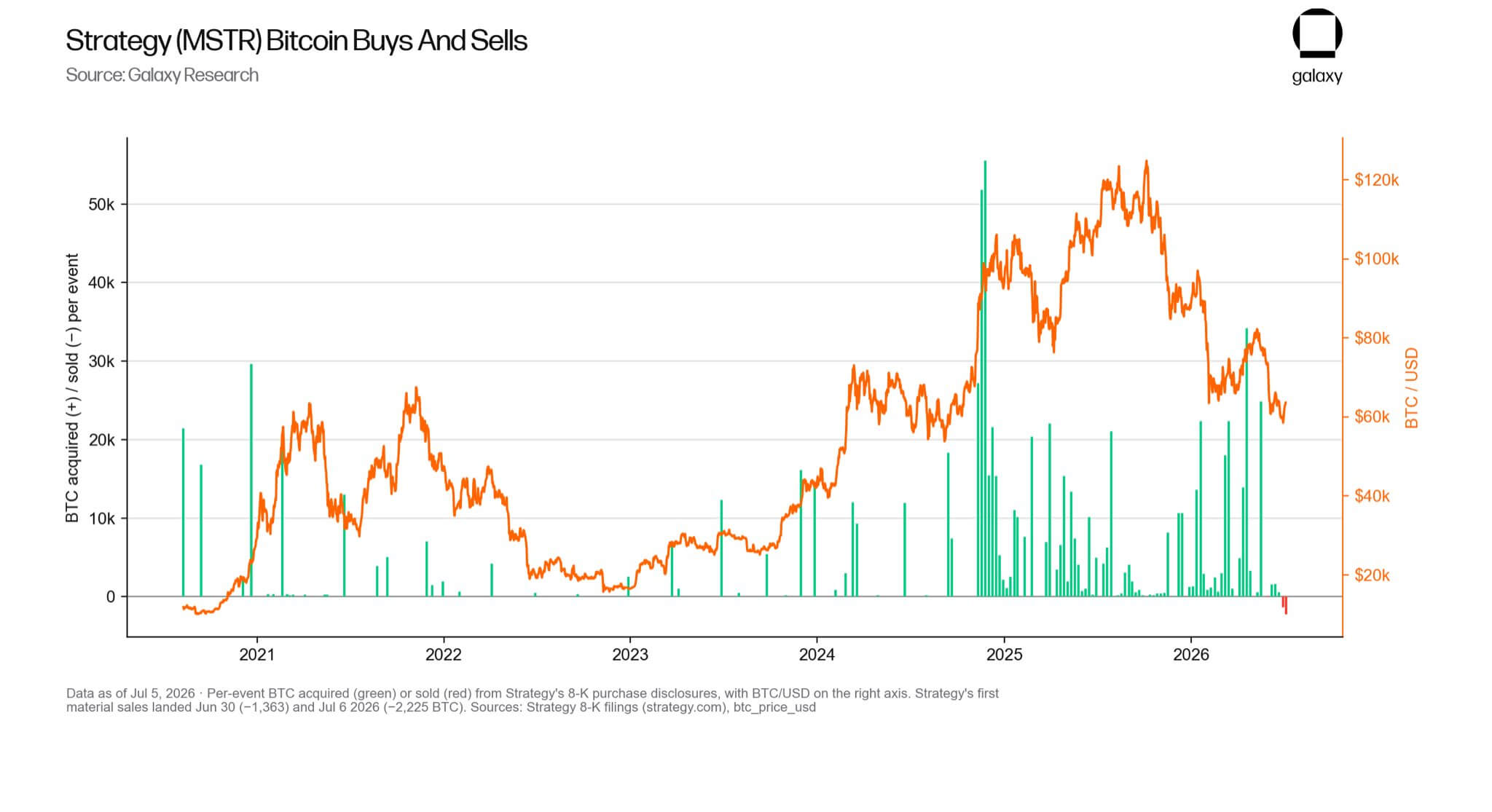

On July 6, the company formerly known as MicroStrategy revealed that it sold 3,588 Bitcoins for approximately $216 million between June 29 and July 5.

According to the filing, Strategy sold the coins in two installments. First, he sold 1,363 Bitcoins from June 29th to June 30th at an average price of $59,256, followed by an additional 2,225 Bitcoins from July 1st to July 5th at an average price of $60,773.

With the previous sale of 32 BTC, the company sold a total of 3,620 BTC in the second quarter. However, the company remains a top crypto net buyer, acquiring over 85,000 BTC during the reporting period.

While these BTC sales are small compared to Strategy’s remaining 843,775 Bitcoins, they represent a notable change for a company that has long been associated with relentless accumulation and public refusal to treat Bitcoin as a source of cash.

Notably, the company’s remaining Bitcoins were acquired for approximately $63.69 billion, or an average price of $75,476 per coin.

This means that this sale was conducted at a price significantly below Strategy’s average purchase price.

Blockchain analytics platform Lookonchain estimated that recent BTC sales resulted in losses of more than $55 million, based on the difference between the company’s reported sales price and past acquisition costs.

Meanwhile, Strategy Inc. revealed that it recorded a loss of $8.32 billion on its digital asset holdings in the second quarter, as the value of its holdings fell below cost basis due to the fall in Bitcoin prices during the reporting period.

He further added:

“As of June 30, 2026, Strategy’s cost basis in Bitcoin holdings exceeded the fair value of its Bitcoin holdings. As a result, Strategy expects to record a valuation allowance against deferred tax benefits and deferred tax assets related to unrealized losses on Bitcoin during the quarter ended June 30, 2026, fully offsetting these amounts.”

Strategy to use Bitcoin as a source of funds for preferential offering dividends

Strategy’s Bitcoin sale changes the way the company uses its reserves.

In its filing, the company said: 3,588 Bitcoin sales will fund preferred stock Handouts.

Sailor said:

These are the Q2 quarterly dividends for STRF, STRE, STRK, and STRD, and the full June monthly dividend for STRC.

The company added that the sale will also partially replenish its US dollar reserves used for payments. Reserves stood at $2.55 billion as of July 5 and are intended to cover preferred dividends and interest on outstanding debt.

Meanwhile, the filing also shows that Strategy chose not to execute during the period.

Mr. Thaler’s company did not sell any common stock through its market share program during the week ending July 5, nor did it repurchase any common stock or preferred stock. The full amount of the $1.25 billion Bitcoin monetization program remains available.

This leaves Bitcoin as a more visible tool in the company’s capital management strategy. Under this framework, Strategy can sell Bitcoin to rebuild dollar reserves, pay preferred dividends, repay debt, and support common and preferred stock buybacks.

Already, market observers such as Jiang Zhuoer, founder of Chinese mining pool BTC.top, have suggested that Saylor may sell more coins soon. Mr. Takuji pointed out as follows.

“MSTR’s willingness to pay this price can only be interpreted as MSTR preparing for a swing trade with a huge coin position, and all 20,000 coins already approved by shareholders will likely be sold.

In the current bear market, MSTR, the relentless buying and selling force of the bulls, is giving way to the short-selling bears. And during the ensuing bull market phase, we will see the biggest whale dumping hundreds of thousands of coins. ”

This complicates what was once a simple market story. Strategy built its reputation on raising funds to buy Bitcoin. The latest filing shows that the opposite can also happen. This means that Bitcoin could be sold to support the financing structure that helped fund the accumulation.

This brings the preferred stock complex closer to the center of the investment agenda. Strategy’s preferred securities reduced its reliance on common stock issuances, but also created periodic cash obligations prior to common stockholders.

If Bitcoin rises and Strategy’s stock is trading at a premium compared to its holding value, this structure will be easier to maintain. In that environment, the company can raise capital on favorable terms and continue to grow its Bitcoin position.

If Bitcoin falls and stock prices decline, management will need to balance three competing priorities: preserving liquidity, avoiding unattractive equity issuances, and maintaining confidence among preferred holders.

The latest sale suggests that Strategy is willing to use Bitcoin to manage its balances. While this gives the company flexibility, it also raises new questions for public shareholders about whether future dividends, debt costs, or reserve requirements could prompt additional Bitcoin sales during times of market stress.

Bill Miller IV of Miller Value Partners offered a more favorable interpretation, saying shareholders and Bitcoin supporters should welcome the sale. This is because a sale provides the benefit of recovering losses and helps demonstrate to rating agencies that Bitcoin is liquid enough to support corporate debt.

That’s the new tension within Strategy’s model. Using Bitcoin to support preferred dividends could help validate the use of assets as collateral in traditional capital markets.

However, this also means that Strategy’s Bitcoin holdings are not insulated from the cash needs of its own financial institutions.

Thaler’s long-term paper passes the short-term test

Despite Bitcoin’s recent sell-off and large quarterly losses, Saylor remains publicly committed to the idea that Bitcoin’s next decade will be shaped by deeper integration with global capital markets.

Over the weekend, Saylor introduced Bitcoin as a form of digital capital. In his view, the future of the asset will depend less on protocol changes and the traditional four-year halving cycle than on the growth of financial structures built around it (ETFs, corporate bonds, bank credit, derivatives, collateral markets, sovereign reserves, etc.).

This paper helps explain why Strategy goes beyond just buying Bitcoin. The company is building a capital market structure around its holdings, using preferred stocks, bonds, cash reserves and other securities to turn Bitcoin into the basis of what Saylor calls digital credit.

The latest sale shows the practical side of that vision. If Bitcoin can function as capital within traditional finance, it must also function within the routines of corporate finance. Dividends must be paid. Interest must be paid. Reserves must be maintained. We need to reassure investors across the capital structure.

That creates tension in strategy. The more successful the company is at turning Bitcoin into a productive balance sheet asset, the less its holdings will look like a one-way vault. Bitcoin can support credit products and preferred securities, but it can also be sold if cash is needed for those products.

Saylor argued that while Bitcoin itself should remain slow-moving and immutable, innovation should develop around it through storage, lending, structured products, payment systems, and institutional balance sheets. Strategy is currently testing that argument in the public market.

The company’s challenge is no longer just convincing investors that Bitcoin will rise over time. They must also convince them that the corporate lending machine built around Bitcoin can withstand periods of asset decline.

(Tag translation) Bitcoin