JPMorgan views Wall Street’s move to private blockchains as a more serious threat to Bitcoin than Strategies selling BTC.

JPMorgan warned that moving tokenization, payments, and settlement to closed networks could drain activity, liquidity, and capital from cryptocurrencies, leading to lower valuations.

A hybrid public-private system, stricter stablecoin rules, and Bitcoin’s staying power as digital gold could still upset that outlook.

Swift said 17 banks across six continents, including Citi, HSBC, Standard Chartered, UBS, Wells Fargo and Itau Unibanco, will begin live testing tokenized deposit payments on the new blockchain ledger, opening the door to 24-hour money transfers.

On May 4, DTCC announced that more than 50 companies, including BlackRock, Goldman Sachs, Morgan Stanley, Nasdaq, and the New York Stock Exchange, have joined the tokenization working group, with plans to begin limited production trading in July 2026 and full-scale launch in October.

How JP Morgan’s lawsuit stands

DTC already has over $114 trillion in assets under custody, and DTCC subsidiaries processed $4.7 trillion in securities transactions in 2025.

When tokenized deposits are settled within bank-managed ledgers and tokenized securities reside within DTC’s own infrastructure, their volumes never touch the fee markets, liquidity pools, or token demand that Ethereum, Solana, stablecoin issuers, and RWA platforms rely on.

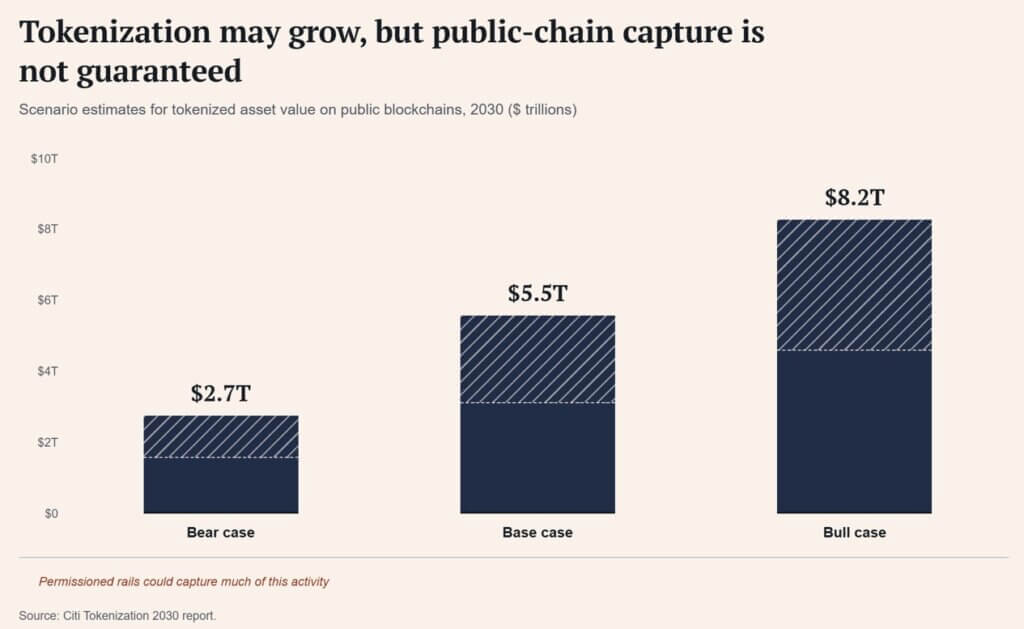

According to Citi’s Tokenization 2030 Report released in June 2026, the base-case tokenized asset market will reach $5.5 trillion by 2030, with a bear case of $2.7 trillion and a bull case of $8.2 trillion.

In its June 2026 annual report, BIS pointed out how that growth will look, noting that while private permissioned networks can meet the regulatory and governance needs of financial institutions, they also risk creating walled gardens that stifle competition and innovation.

What Wall Street wants from Bitcoin

BlackRock’s Spot Bitcoin ETF (IBIT) page describes the product as providing exposure to the price of Bitcoin through an exchange-traded mechanism that eliminates the custodial and operational work involved in owning the asset directly.

IBIT had approximately $45.6 billion in net assets as of July 8, a figure that held despite a year-to-date NAV return of -28.93%.

Investors continued to park tens of billions of dollars in funds that have lost nearly 30% of their value this year, a pattern that resembles allocators securing scarcity through the most manageable wrapper.

Walled gardens are easy to understand once you name them. Bank-run ledgers can freeze balances, permissioned chains can exclude wallets, tokenized deposits still answer to the issuing bank, and a transfer agent’s record can outweigh the tokens sitting on it.

Bitcoin is slow, expensive to move at scale, and built for purposes other than regulated securities settlement, providing a ledger that is outside the control of any single institution and exists alongside practical limitations.

This makes Bitcoin an asset outside of the system that Swift, DTCC, and a growing list of World Banks are building on.

| Features | Private bank ledger/tokenized deposits | Bitcoin |

|---|---|---|

| core functionality | Accelerate institutional payments, settlements, and asset recording | Rare bearer assets outside the bank’s control |

| access model | Permits, KYC gates, institutional intermediaries | open network access |

| control point | Bank, custodian, transfer agent or market infrastructure provider | Not a single institution operator |

| Reversible/Freezable | Your balance or access may be frozen or restricted | Remittances are not controlled by one institution |

| Main benefits | Compliance, speed, liquidity efficiency and regulatory suitability | Neutrality, scarcity and resistance to censorship |

| Main weaknesses | Walled garden, exclusion risk, limited openness | Volatility, scaling limits, storage/security risks |

| JP Morgan’s risks are most applicable to: | Public chain activity, fees, liquidity, and token value acquisition | Bitcoin only if investors treat it as a general cryptocurrency beta |

Bitcoin 3rd throw

Bitcoin began as peer-to-peer electronic cash, but became digital gold when ETFs included it in their allocations.

The era of private chains gives us a third paradigm: scarce assets available to everyone every time the digital rails pass a bank, custodian, or compliance gate.

The Fed kept its target range at 3.50-3.75% at its June 2026 meeting, and the dollar index was hovering around 100.93 as of July 9, amid geopolitical tensions and inflation concerns.

Stablecoins still have the largest public chain payments footprint, with DeFiLlama showing around $311.9 billion compared to the nearly $14.9 billion stablecoin market capitalization of tokenized U.S. Treasuries, which is only a fraction of the roughly $30 trillion U.S. Treasury market itself.

The above case is a narrative argument and there are real limits to what can be guaranteed relative to price. JPMorgan Private Bank noted that Bitcoin’s volatility has been about four times that of global equities over the past decade, and noted that a 5% Bitcoin allocation increased portfolio risk by 13%, compared to a 2% increase for a comparable gold position.

Cryptocurrency companies are already bracing for the risks posed by quantum computing, with some estimates suggesting that a significant portion of Bitcoin’s supply could eventually be exposed if cryptography is not upgraded.

On the bullish path, tokenization will grow towards the higher reaches of the City, with access remaining gated, reversible, and bank-mediated every step of the way. Public chain tokens lose the premium on the payment layer that JPMorgan’s argument targets, and highlight Bitcoin’s characteristics of being rare, neutral, and not issued by any institution.

The introduction of a private chain will begin to serve as a free advertisement for one ledger independent of all the banks that build this system.

On the bear side, ETF outflows and risk-off markets dominate the narrative, with investors reading the introduction of private chains as evidence that banks now control the infrastructure cryptocurrencies they once promised to replace.

| scenario | what must happen | What it means for public chain cryptocurrencies | What it means for Bitcoin |

|---|---|---|---|

| Bull path: walled garden increases the value of the exit | Tokenization expands towards Citi cap, but access remains gated, reversible, and bank-mediated | Public chain tokens will lose some of the payment layer premium targeted by JPMorgan | Bitcoin’s contrast strengthens as a rare, neutral currency outside of bank-controlled ledgers |

| Bearish path: banks win the infrastructure story | ETF outflows, risk-off markets and weak liquidity dominate sentiment | Private chain adoption interpreted as evidence that banks have captured the promise of cryptocurrencies’ native infrastructure | Bitcoin trades in crypto beta despite its clear financial theory |

| base path: both arguments coexist | While banks tokenize payments, Bitcoin remains primarily an allocation asset in the ETF era | Activity moves to permitted rails, limiting some profits on the public chain | Bitcoin benefits narratively, but price still depends on flows, macro liquidity, and risk appetite |

Bitcoin has fallen relative to other sectors because its price follows the sector’s overall risk appetite rather than its underlying narrative, no matter how clear the theory is.

When it comes to Bitcoin, JPMorgan’s warning describes the asset’s oldest debate in real time. A financial system that only a handful of institutions can program creates a unique demand for an asset that no other institution can.

(Tag translation) Bitcoin