Bitcoin mining is still driven by subsidies rather than demand.

This is a more beneficial place to start for the next Bitcoin difficulty adjustment period. CoinWarz currently predicts that the difficulty will drop by 4.91% to 132.14 trillion from 138.97 trillion on April 18, 2026.

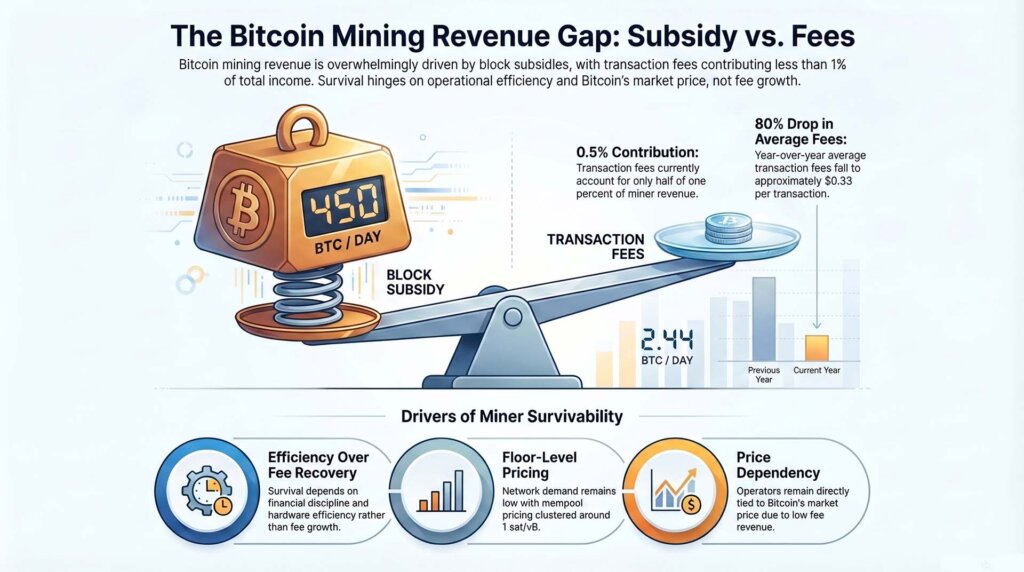

The schedule is not as important as the structure underneath it. YCharts using data from Blockchain.com showed that the daily Bitcoin transaction fee is 2.443. $BTC On April 8th, it was down 69% from the previous year.

Block subsidy fixed at 3.125 $BTC Although the network generates approximately 144 blocks per day, fees are still only a small portion of miner revenue. $BTC Clause.

So over the next few weeks, we’ll be working on more focused, more informative questions. If fees are fixed near the floor, what actually determines miner viability?

The answer starts with the revenue stack, then the cost stack, and then the adaptation stack. Revenue remains overwhelmingly dependent on subsidies and Bitcoin prices.

Costs still depend on power, vehicle efficiency, debt, and financial policy. If mining alone no longer provides enough attractive returns for power and infrastructure, adaptation will depend on how flexible operators are.

The role of upcoming difficulties is secondary. Less difficult targets can reduce pressure on operators by increasing their output per hash unit when prices and fees are stable. In the current environment, that distinction shapes the entire operational map of miners.

Subsidies accumulate revenue while fees remain near the floor.

Bitcoin miners receive compensation from two sources: subsidies and fees. Subsidies are protocol-level issuances that accompany each block. Fees are additional fees paid by users to confirm transactions.

In a more powerful on-chain environment, the fee tier becomes a true contributor to the miner’s economy. In a weak one, it atrophies into irrelevance, leaving miners more directly tied to Bitcoin’s market price.

That is the current condition. A recent snapshot of mempool.space shows that low-priority, medium-priority, and high-priority transactions are clustered around 1 sat/vB. According to YCharts, the average Bitcoin transaction fee as of April 8 was $0.3335, down 80.53% year-on-year. The network is still functioning smoothly, blocks are still being mined, and users still have cheap access to block space.

For miners, the impact on revenue is straightforward. There is little additional support from fee income. Bitcoin was hovering around $71,800 as of April 10, up 7.4% in the past seven days and 3.1% in the past 30 days. This move is primarily due to the value of the subsidy, rather than a resurgence of user-paid demand for block space, but it is helpful.

The magnitude of the imbalance is large enough to define a frame by itself. Bitcoin still produces about 144 blocks per day. 3:125 $BTC per block, or about 450 $BTC Every day, you will receive the newly issued subsidy before the charges. On this basis, the total commission on April 8th is 2.443. $BTC This suggests that fees contribute about half of 1% of miner revenue. $BTC Clause.

This is why it’s a living question that keeps miners alive when fee tiers are of little use. The following resets are still included in the analysis, but belong to the correct location:

Lower difficulty settings improve economy at the fleet level because miners require less computational effort to find blocks. It can relieve pressure. Miner survivability in the coming weeks will still be largely determined by price, efficiency, power costs, debt, and financial discipline. Power costs, machine quality, debt burden and financial policy determine who bends first.

Once the revenue side is stripped down to subsidies and prices, it becomes much easier to see how costs stack up. Miner viability depends on who can produce Bitcoin at a cost that leaves room for operating cash flow.

It all comes down to electricity prices, fleet efficiency, hosting costs, the level of debt on the balance sheet, and whether management has enough flexibility in the Treasury to avoid a sale in weak conditions.

CoinShares provides the clearest external framework for its hierarchy. CoinShares said in its Q1 2026 mining report that Q4 2025 was the toughest quarter for miners since the 2024 halving, and predicted that the weighted average public miner cash production cost would be close to $79,995 per miner. $BTC In the fourth quarter of 2025.

This number clearly shows how narrow the spreads have become across the listed areas. CoinShares also stated that miners under S19 XP are losing $30 per PH per day if they are paying more than 6 cents per kilowatt hour.

This helps build a clearer three-tier hierarchy.

The first tier consists of low-cost operators with modern fleets, favorable hosting or self-mining power, and balance sheets that can absorb volatility without immediate forced sales.

These miners still face pressure from a low-fee market, but they have enough efficiency and financial flexibility to weather it. Their problem is margin compression, not immediate viability.

The second tier is the disciplined middle tier. These operators can survive, although they require tighter financial controls, more selective deployment, slower expansion, and tighter filters on capital expenditures.

They should be able to survive the next few weeks if Bitcoin prices hold and the expected difficulties are close to current expectations. There is still much less room for error compared to the higher tiers, as the pricing tiers offer much less support.

The third layer is where the real pain is. These are companies with high-cost legacy fleets, operators running older machines, miners with weak power economics, and capital structures that don’t give them much time.

The group first broke out because low fees eliminated the one revenue line that could have cushioned a difficult quarter. For them, the problem is often no longer about growth. It’s about cuts, site-by-site triage, machine outages, opportunistic Treasury sales, and whether parts of the fleet are still worthy of capital increases.

This is an operating leverage point where mining scope often becomes vague. Price is still important here, but is primarily used as an input to hash price and cash margin. CoinShares estimated that if Bitcoin recovers to $100,000, the hash price could rise to about $37 per PH per day, and if it retests $126,000, it could rise to about $59 per day.

These ranges indicate how quickly the situation will improve if prices move large enough. They also show why the current environment still feels challenging. Although Bitcoin has stabilized, it is still well below levels that provide broad comfort across the mining stack.

Therefore, fiscal policy becomes a more important variable than usual. Operators with strong treasuries are able to withstand periods of low fees and moderate hash prices.

Inflexible businesses need to decide whether to sell sooner $BTCreduce capital expenditures and idle older rigs or retire marginal sites. In markets where subsidies do almost all the work, financial management becomes part of the production model.

Define your stack to adapt to the next reset window with reduction, fleet triage, and AI pivots

When revenues slump and costs tighten, the next challenge is adaptation. What do miners actually do when pure Bitcoin mining no longer provides sufficient operating leverage?

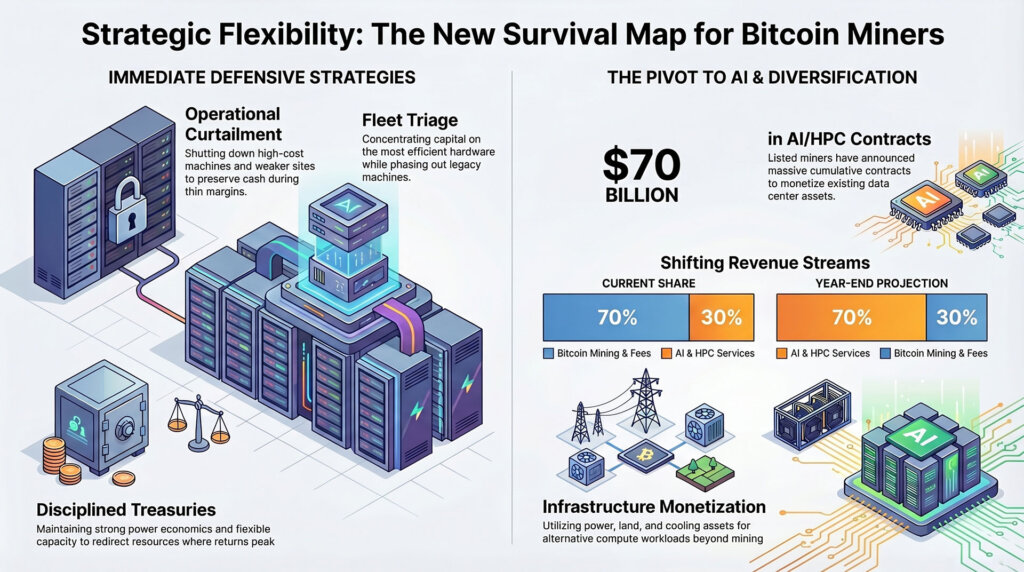

The first adaptation is reduction. Operators shut down high-cost machines, reduce exposure on weak sites, and conserve cash while waiting for better pricing terms or more favorable difficulty profiles.

The second is fleet triage. Capital is directed towards the most efficient hardware and best performing sites, while older machines remain online only if the costs of power and hosting can be covered.

The third is strategic diversification, where miners move beyond Bitcoin mining itself and begin to consider how their power, land, cooling, and data center assets can benefit them in adjacent markets.

CoinShares said in a report that publicly traded miners have announced more than $70 billion in cumulative AI and HPC contracts and could derive up to 70% of their revenue from AI by the end of the year, up from about 30% currently.

This prediction says a lot about how miners rank options. Sites with sufficient power access and data center potential may earn more revenue from alternative workloads than from mining Bitcoin in a low-fee environment.

Low fees also reduce the relative attractiveness of mining compared to other compute-intensive businesses competing for the same infrastructure footprint. Miners don’t need ideological beliefs to make that change.

The next reset window still poses a short-term test for the market. CoinWarz will make its next difficulty adjustment on April 18th, when the predicted value will be lowered to 132.14 trillion. If this adjustment reaches levels close to expectations, miners should receive some relief in the economics of production. More pointed questions follow. Are there any actual changes in pricing layers?

Any meaningful improvement would require a rise in Bitcoin prices, a return to tangible fees, or both. Without fee collection, miners remain dependent on subsidies and prices, even at low difficulty settings.

The winners in the coming weeks are likely to be miners with efficient fleets, better power economics, stronger financial controls, and enough strategic flexibility to shift production capacity to where it will be most profitable.

The losers are likely to be miners who need rate support to compensate for legacy equipment, high power costs, or weak balance sheets.

Bitcoin mining is still producing blocks on schedule, and the next difficulty adjustment may give operators some peace of mind.

The deep state remains the same. Demand for block space contributes little, and the viability of miners depends on who can endure a low-fee environment long enough for prices, fees, or both to improve.