The identity of Bitcoin miners is collapsing on four fronts simultaneously: shrinking margins, accelerating AI transformation, rising debt burdens, and the no longer applicable discipline of selling government bonds.

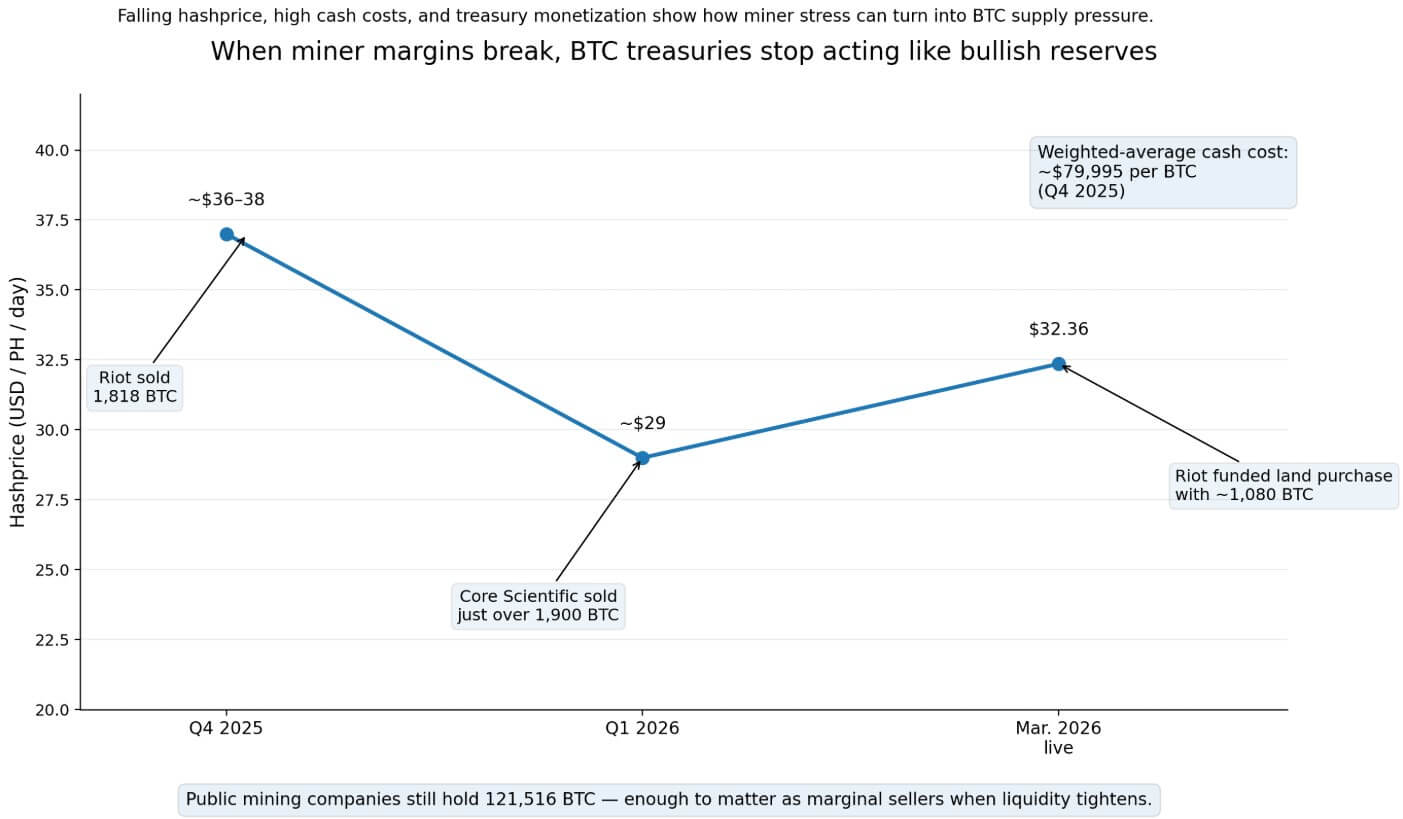

According to CoinShares’ latest mining report, the weighted average cash cost for public miners in Q4 2025 was approximately $79,995 per BTC. During the quarter, hash prices fell to around $36-38 per PH/sec per day, and further fell to around $29 in Q1 2026.

The network has recorded three consecutive negative difficulty adjustments, the first such streak since July 2022. Live hash prices are currently around $32.36/PH/day, fees are only 0.40% of the block reward, and the average hash price in the 6-month futures market is close to $30.42.

What miners do under these circumstances begins the case for market structure.

Public mining companies collectively hold 121,516 BTC worth approximately $8.63 billion, making them significant marginal sellers even after losing their position as the dominant public company financial class.

Some companies have already moved from holding to selling. MARA changed its strategy in 2025, allowing the sale of Bitcoin from operations, and expanded it to balance sheet BTC in 2026.

Riot Platforms sold 1,818 BTC for $161.6 million in December 2025, Core Scientific sold just over 1,900 BTC for approximately $175 million in January 2026, and currently holds less than 1,000 BTC.

Separately, Riot fully funded the purchase of 200 acres of land in Rockdale by selling approximately 1,080 BTC from its balance sheet.

This action runs counter to retailers’ persistent assumptions, held by miners by default, that miners’ large financial balances are structurally bullish.

When margins break, miners act like commodity producers managing liquidity, and Treasury policy becomes procyclical, concentrating selling at a time when BTC is already falling.

fragmentation of identity

The rift CoinShares described widens deepest through the AI pivot.

The company says listed miners could earn up to 70% of their revenue from AI by the end of 2026, up from around 30% currently.

Core Scientific is supplying approximately 350 MW of power for CoreWeave and is targeting approximately 590 MW by early 2027. Q4 2025 revenue already shows $31.3 million from colocation, compared to $42.2 million from self-mining.

Hut 8 signs a 15-year lease for a 245 MW AI data center with a base price of $7 billion. IREN reported $17.3 million in AI cloud services revenue and secured $3.6 billion in GPU funding related to its deal with Microsoft, leading investors toward its $3.4 billion ARR goal by the end of 2026.

TeraWulf says it has signed more than $12.8 billion in long-term customer commitments and completed $6.5 billion in long-term financing through 2025. Riot signs first AMD data center lease.

For equity investors, this will redefine what a minor stock actually represents. Purchasing a publicly traded miner now bundles exposure to BTC price, hyperscaler demand, lease execution schedules, renovation capital expenditures, funding costs, and counterparty quality.

CoinShares explicitly described this as a watershed where AI/HPC-related names are garnering a valuation premium over pure miners. Although the stocks share the same ticker symbol, the underlying business has shifted its center of gravity.

| company | Mining business signals | AI/HPC signal | Debt/Funding Signals | What stocks increasingly represent |

|---|---|---|---|---|

| core scientific | $42.2 million in self-mining revenue | Colocation revenue was $31.3 million. 350 MW energized. 590MW target | Expansion of loan facility | Hybrid mining + datacenter execution |

| hut 8 | Still mining BTC | 245 MW, 15 year AI lease | Large-scale long-term infrastructure exposure | Power + Digital Infrastructure Platform |

| Airen | Mining still makes sense | AI cloud revenue was $17.3 million. ARR target of $3.4 billion | ~$3.7 billion in convertible debt | Leverage a hybrid of AI + mining |

| terra wolf | the mine still exists | $12.8 billion in customer contracts | Large amount of financing and debt | AI Landlord with Mining Residuals |

| riot | Mining-led brands | AMD Data Center Lease | Treasury Monetization + Expansion Capital Investment | BTC Exposure and Data Center Options |

| cryptography | mining operator | HPC diversification in development | Billions of secure banknotes | Migration story with emphasis on leverage |

Debt burdens amplify that disparity. IREN held approximately $3.7 billion of convertible notes as of December 31, 2025. Terrawolf’s balance sheet shows current long-term debt of approximately $46.3 million, short-term convertible debt of $489.8 million, long-term debt of $3.05 billion, and convertible debt of $1.58 billion.

Core Scientific expands its strategic financing facility to $1 billion. Cipher disclosed $3.73 billion in recent senior secured debt financings.

Businesses built around these balance sheets care about interest rates, refinance terms, construction cost inflation, and customer concentration in a way that pure Bitcoin miners never had to.

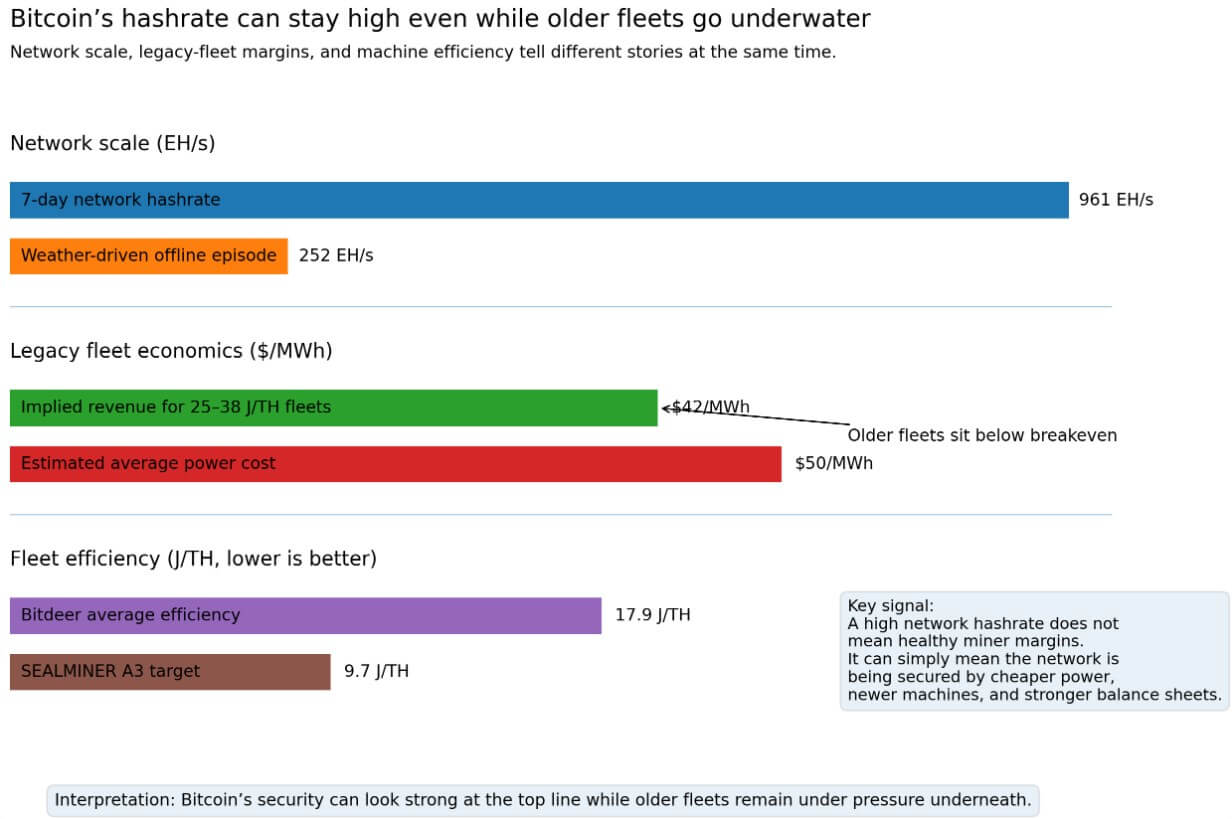

On the other hand, the network hash rate runs at around 961 EH/s, but this figure is more clearly explained by Luxor’s data.

Fleets operating at 25-38 J/TH had an implied return of approximately $42/MWh compared to an estimated network average power cost of $50/MWh, and S19 class hardware was in negative gross margin territory throughout February.

Luxor also recorded a 252 EH/s weather offline episode, demonstrating how quickly a marginal fleet can disappear when the economy tightens.

Bitdeer aims to achieve an average miner efficiency of 17.9 J/TH in the fourth quarter of 2025 and 9.7 J/TH with SEALMINER A3.

High hashrate can now coexist with widespread unprofitability in older fleets. That is, a narrower, better-capitalized, and more machine-efficient set of survivors now protects the network. At the same time, the broader sector remains under stress.

potential scenarios

If BTC recovers towards the $100,000 mark, hash prices ease, and financial stress immediately subsides, the winners in the stock will be operators that can combine mining margin recovery with reliable AI/HPC execution. Because these names capture both BTC’s recovery and infrastructure-related valuations.

Core, Riot, Hut 8, TeraWulf, and IREN all demonstrate ample data center ambition to drive price recovery and widen the gap between hybrid and pure brands.

In that scenario, the AI pivot shifts from survival strategy to valuation drive, allowing the most indebted operators with the strongest contract pipelines to reap profits that pure miners cannot match.

If BTC falls below the stress threshold warned by CoinShares, hash prices will remain in the high $20s to low $30s, normalizing additional Treasury drawdowns across the sector.

Luxor’s February fleet data suggests that many legacy machines were already in the water before further price declines, so a continued economic downturn will accelerate forced closures, monetization of reserves, and share transfers to lower-cost next-generation operators.

The sector’s total of 121,516 BTC in government bonds creates an oversupply that comes into play just when the BTC spot market is at its weakest.

At the same time, miners hauling billions of dollars of convertible cargo will face refinancing stress if AI contract performance is delayed or capital markets tighten.

The most indebted hybrid companies absorb headwinds from two directions simultaneously: BTC price and building infrastructure reliability.

CoinShares’ fracture report document runs under both scenarios.

Miners no longer share a unified BTC appreciation theory, and some miners are now selling BTC to fund their operations.

Some companies derive more enterprise value from executing data center leases than from block rewards.

Some companies could benefit from Bitcoin weakness once weaker rivals go out of service, difficulties ease and margins are secured for surviving companies.

The companies that still secure Bitcoin blocks are fragmenting into a minority of forced sellers of goods, debt-financed AI landlords, and efficient pure-play operators with power costs and machine quality that allow them to survive without a pivot.

(Tag to translate) Bitcoin