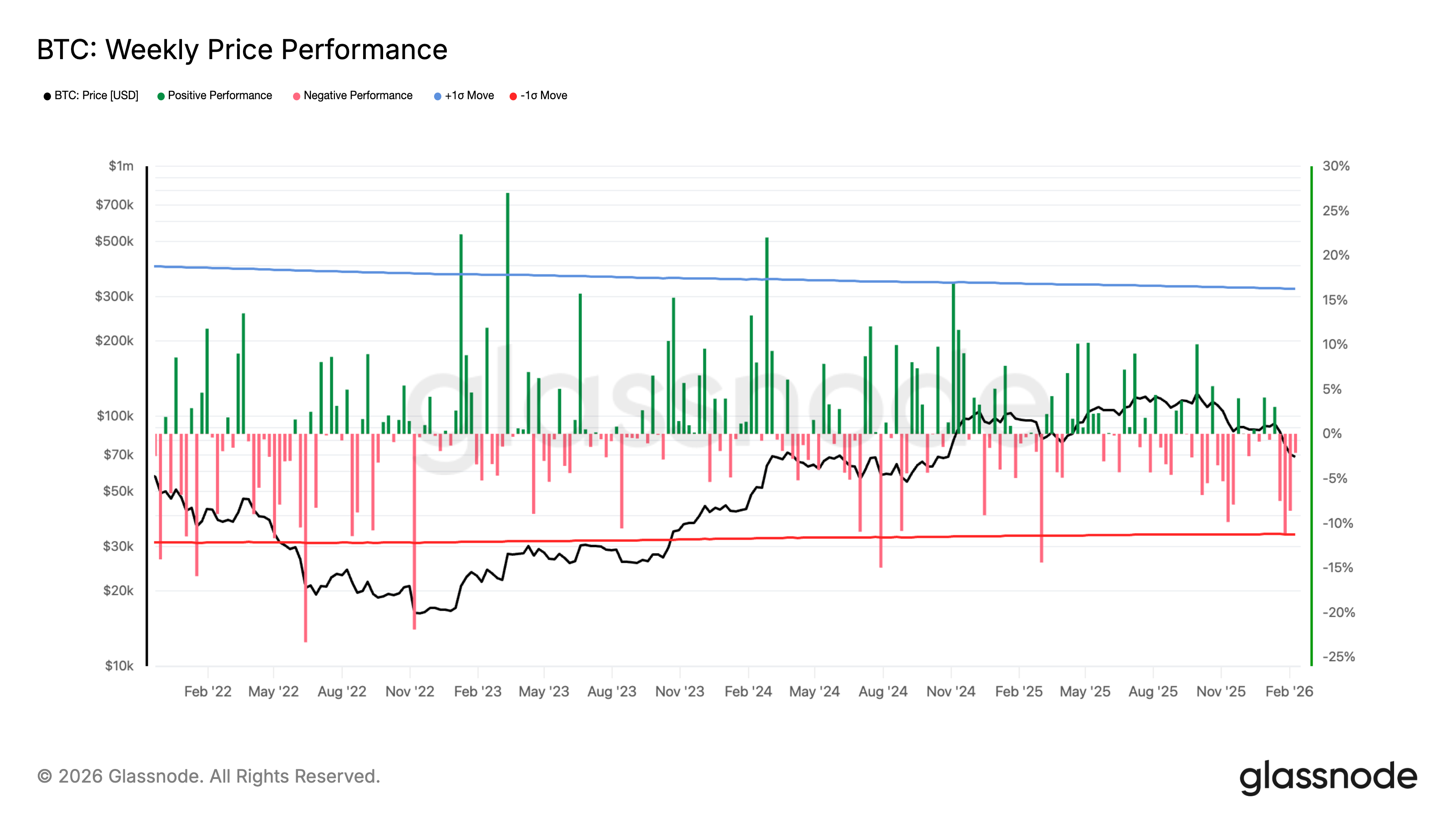

Bitcoin is on pace to record its fifth straight week of declines, the first time since March-May 2022, when Bitcoin fell for nine consecutive weeks.

As of Thursday Asian time, the largest cryptocurrency by market capitalization had already fallen about 3% this week to below $67,000, according to market data from CoinDesk, making a weekly red close likely.

Macro pressures are increasing technological weaknesses. According to the Wall Street Journal, the United States has amassed the largest concentration of air power in the Middle East since the 2003 invasion of Iraq. The US government is reportedly prepared to launch an attack on Iran, but President Donald Trump has not made a final decision and bettors at Polymarket place a 27% chance of an attack by the end of this month.

Geopolitical uncertainty pushed the dollar index to 97.7, its highest level since February 6, while WTI crude rose to $65 from Wednesday’s low of $62. A stronger dollar and higher oil prices typically weigh on risk assets, creating further headwinds for Bitcoin and making weekly closes more negative.

Bitcoin has fallen more than 50% since its all-time high of around $126,500 in October, hitting a low of $60,000.

On a month-to-month basis, Bitcoin has recorded five consecutive declines since October, making it the second-longest consecutive decline in history, surpassed only by a six-month decline from 2018 to 2019.

Bitcoin has fallen relative to the precious metal for seven straight months against gold, the longest underperformance of the pair.