Bitcoin prices have fallen again due to the oil shock, rising US Treasury yields, dispelling expectations for interest rate cuts, and huge deribit expirations on top of an already weakened market.

Approximately $14.1 billion of BTC options expired today, March 27th, and an additional $2.2 billion of Ethereum contracts were settled the same morning, bringing the total to approximately $16.38 billion.

This equates to nearly 40% of Deribit’s BTC open interest rolling off in a single session.

Reuters links the broader risk-off factor to oil prices surging above $105, rising U.S. Treasury yields, a strong dollar and markets pricing in a Fed rate cut in 2025 on the back of escalating tensions in the Middle East.

Yesterday, BTC hit an intraday low of $68,127 and ETH reached $2,036. While the deadline approaches Sales have already begun, And this morning, Bitcoin fell to $66,200 and Ethereum fell below $2,000.

Why the last 30 minutes matter the most

Deribit settles expiring contracts at 08:00 UTC using a 30-minute time-weighted average of the index sampled every 4 seconds from 07:30 to 08:00 UTC.

This generates around 450 observations instead of one closing price, making it harder to maneuver the delivery price, but also means that broader market movements during that window are directly reflected in settlements.

At the same time, the deltas of expiring options and futures decay linearly toward zero over the same 30-minute period. Hedges are adjusting, rolls are compressing, and pricing clocks are ticking simultaneously.

This convergence receives a disproportionate amount of attention compared to the window length.

A 2025 SSRN paper using Deribit data found that BTC option activity is concentrated around 8:00-9:00 GMT, with the effect of settlement time being strongest on days with more expiring contracts and shorter maturities. Both cases are true here.

| metric | value | why is it important |

|---|---|---|

| BTC option expires | $14.16 billion | Core size for Friday expiration |

| ETH option expires | $2.22 billion | Have a broader market impact |

| Total expiration date of BTC + ETH | $16.38 billion | Displays the total size of the reset |

| Deribit BTC open interest share decreases | nearly 40% | Emphasizes concentration in one session |

| Payment time | March 27th 08:00 UTC | Fixed events that readers can watch |

| Key pricing windows | 07:30–08:00 UTC | This 30 minutes determines the delivery price |

| Payment method | 30 minute TWAP of Deribit index | Final price is based on average, not per print |

| sampling frequency | every 4 seconds | produces about 450 observations |

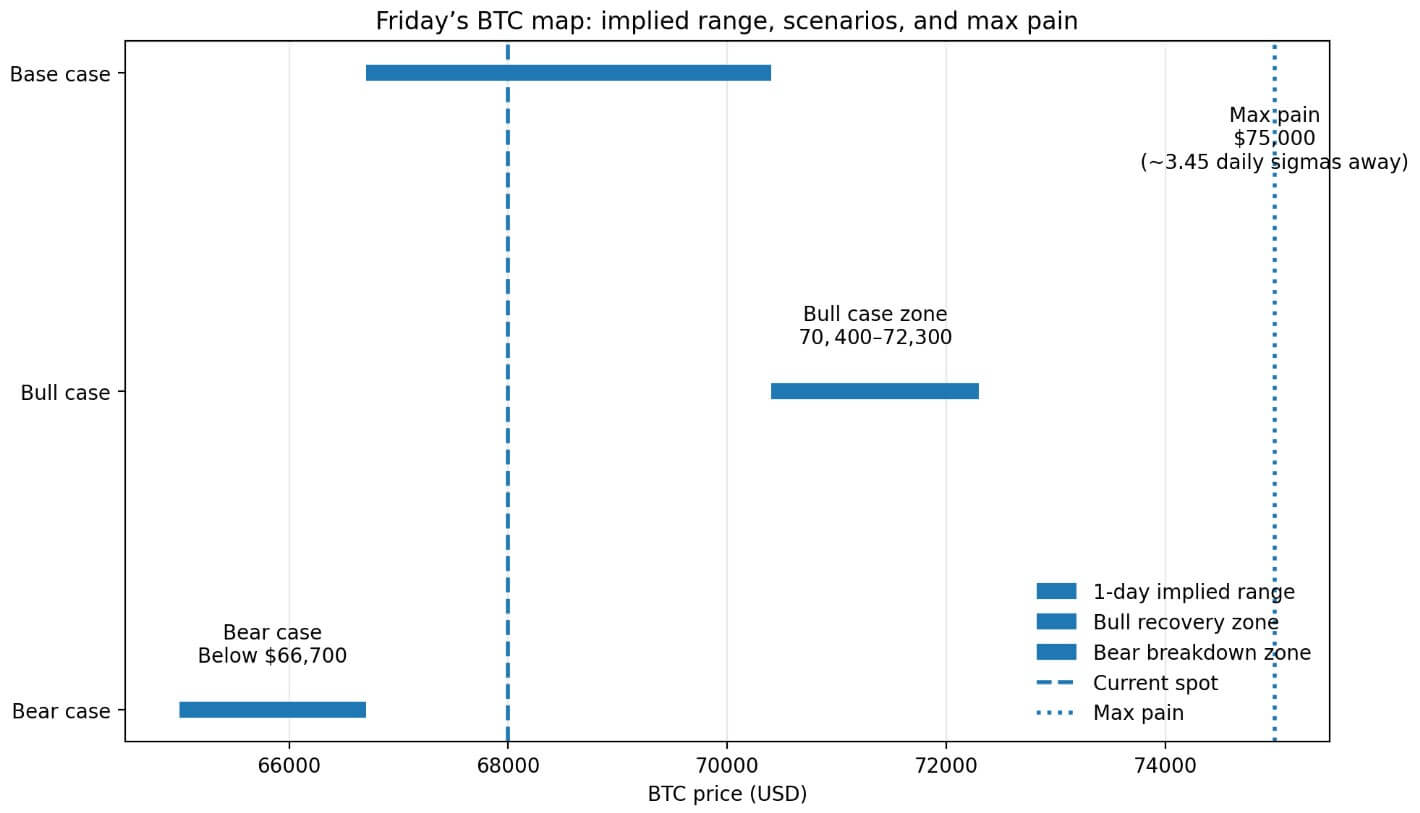

| BTC spot reference | nearly $68,000 | Baseline for all comparisons |

| BTC biggest pain | $75,000 | Positioning reference rather than prediction |

| Put/call ratio | 0.63 | indicates misalignment |

| Distance from spot to maximum pain | ~9.4% | Indicates maximum pain is significantly above current price |

| 7-day BTC ATM Implied Volatility | 52% | Basis for estimating short-term movements |

| Implied daily movement | ~$1,866 | realistic day range frame |

| Implied 30 minute travel | ~$269 | Frame realistic payment window movements |

| Maximum pain distance in 1 day sigma conversion | ~3.45p | Suggests $75,000 is far from possible daily price movement |

| Maximum pain distance in settlement window sigma terms | ~24 hours | Maximum pain indicates far from realistic 30 minutes of movement |

A 2023 paper found that while not uniform across exchanges and contracts, Bitcoin expiration dates have a distinct impact on volume, volatility, and returns around expiration, with the strongest effects immediately before and at expiration.

According to a report citing data from Deribit, BTC’s highest price on Friday was $75,000, with a put/call ratio of 0.63. That level has risen about 9.4% from yesterday’s level of around $68,000. Using the quoted 52% 7-day BTC at-the-money implied volatility, the daily implied move is approximately $1,866, placing $75,000 approximately 3.45 sigma per day above the spot.

On a 30-minute implied volume basis, the implied settlement window movement is approximately $269. This means that $75,000 is almost 24 sigma away from the settlement window.

The maximum pane at $75,000 shows where the concentration of open interest is most intense and is currently about 9.4% above the spot and the settlement window sigma is almost 24 sigma away.

Macro arc that configures expiration time

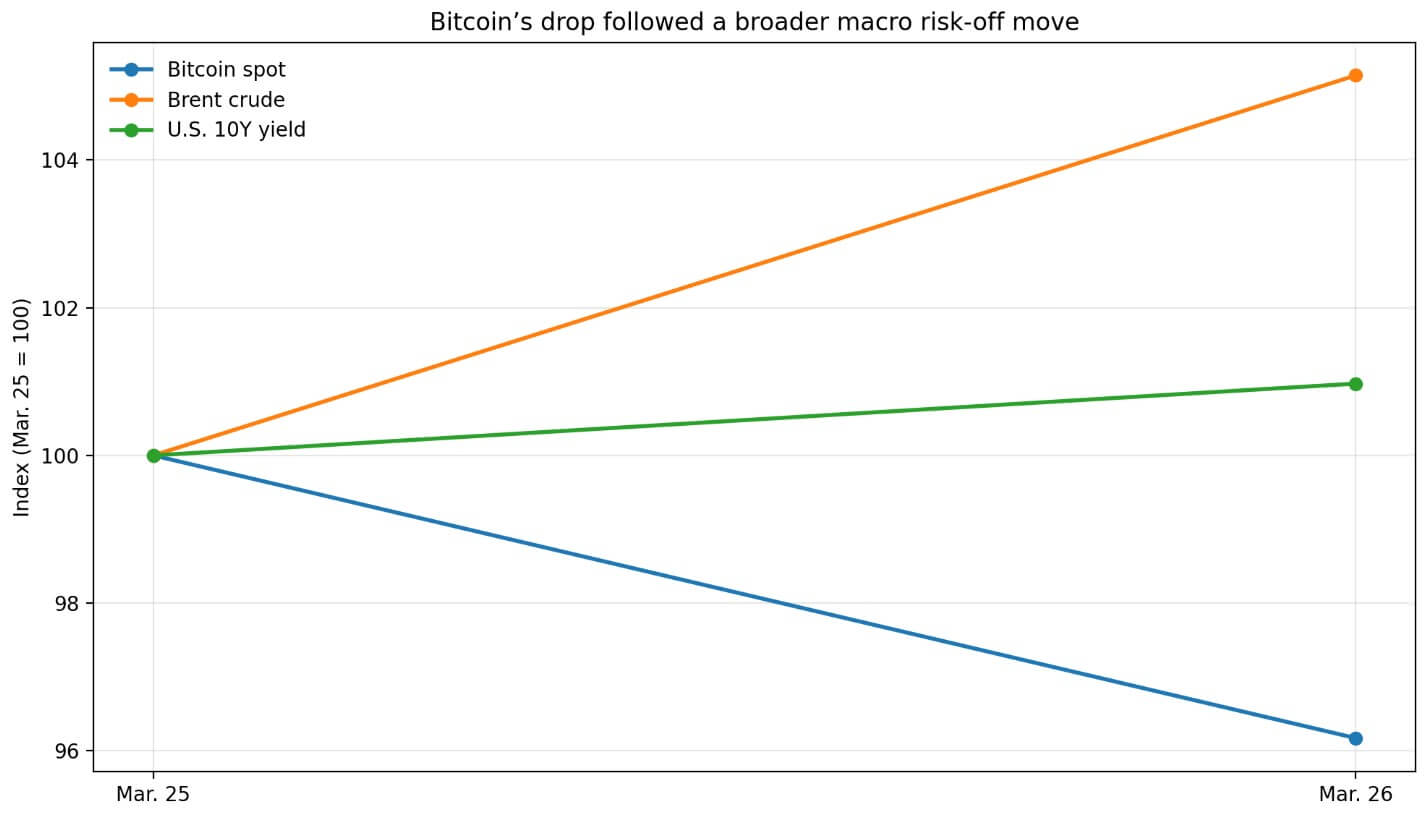

BTC’s recent resilience was already beginning to fray before the recent decline.

Deribit commentary on March 25 stated that Bitcoin has remained relatively stable amid widespread traditional market stress, characterized by weaker stock prices and tighter credit conditions.

By March 26, that foothold had crumbled, with Bitcoin falling below $69,000 as oil shocks, rising yields, and defunct expectations for interest rate cuts resurfaced.

Reuters reports that global equity funds shed $20.3 billion in the week ending March 18, while money market funds absorbed $32.57 billion, consistent with widespread defensive rotation.

Short-term BTC implied volatility fell from 57% to 52% this week as headlines of temporary de-escalation took hold while put skew held. BTC 25 delta puts remained about 5 volatility points higher than calls, and BTC futures implied yields were only 2% to 3% across tenors.

Markets are pricing in a less immediate shock, but the overall mood remains cautious due to put skew and subdued futures yields. The $14.16 billion deadline now puts it in that position.

Deribit holds approximately 85% of the market share for BTC and ETH options, so its settlement rules have significance far beyond its user base. If a single venue’s 30-minute TWAP dominates such a large notional cash settlement, that window mechanism could spill over into the spot market.

Best and worst possible outcomes

Headlines of easing tensions on oil and geopolitics did not arrive by 7:30 UTC, halting Bitcoin’s recovery towards the $70,400 to $72,300 range, with expiring hedges capping the downside rather than adding to fresh selling.

This window may have acted as a stabilizer. With spot firming and fewer in-the-money open puts, dealer hedging flows would have been less unilateral and settlement TWAP would have ended above recent lows.

Expirations cleared without any dramatic changes, and macro easing may have carried prices into the weekend. Tell would have been spot recovered before the settlement began.

However, stress on oil and interest rates deepened into the morning. BTC has fallen below the lower end of its current daily implied range of $66,700, with the current expiration mechanism adding intraday noise to an already bearish market.

For dealers to hedge their put positions, they must sell into a down market, amplifying short-term movements around the settlement window. 30 minutes TWAP has been printing delivery prices that fully reflect macro forces, and now the expiry is accelerating its collapse.

The macro environment that led to this move is now continuing into the post-settlement session.

Academic research and Deribit’s own data confirm that settlement time drives flow and pricing mechanics.

This morning’s 07:30-08:00 UTC window focused on compressing hedging behavior, delta decay, and pricing methodologies into a single, well-defined interval within a macro environment that has already pushed BTC down beyond its implied daily range.

(Tag translation) Bitcoin