CleanSpark offered a good financial quarter, but its market performance did not reflect the same strength. This analysis categorizes key financial, operational insights and strategic directions for understanding the big picture.

CleanSpark Executive Overview: Powerful execution amid market ambivalence

The following guest posts are posted by bitcoinminingStock.io, a one-stop hub for all of Bitcoin Mining Stocks, Educational Tools and Industry Insights. Originally published on February 20, 2025, it was written by Cindy Feng, author of bitcoinminingStock.io.

During the survey of the Bitcoin Mining Annual Report in December 2024, CleanSpark highlighted several key metrics. Total margin, Hashrate expansion, M&A activities, and fleet upgrades. At the time, I believed that the company was in a strong year. Bitcoin prices continued to move upward.

Screenshots of the Annual Report (co-authored with NICO SMID, a digital mining solution)

However, following Cleanspark’s finances Q1 2025 Revenue Call February 6, 2025, the company Stock prices remained flat and even fell. This market response raised me a few questions: Which numbers surprised investors?? Did the company provide investors-related guidance? Take a closer look at the numbers and break down what’s going on.

Financial highlights: revenue and profitability have skyrocketed

CleanSpark’s finances The first quarter of 2025 (October 1 – December 31, 2024) was a financially outstanding quarter.demonstrates strong revenue growth and strong profitability due to rising Bitcoin prices and increased operational efficiency.

Key income statement indicators:

- Revenue: $162.3 million (+120% year-on-year) vs. $73.8 million in the first quarter of 2024. This is mainly Bitcoin prices will riseoffset by the low number of bitcoins mined by the April 2024 Harving Event

- Net profit: In the first quarter of 2024, $246.8 million (+854% year-on-year) vs. $205.9 million, dues for Bitcoin revaluation.

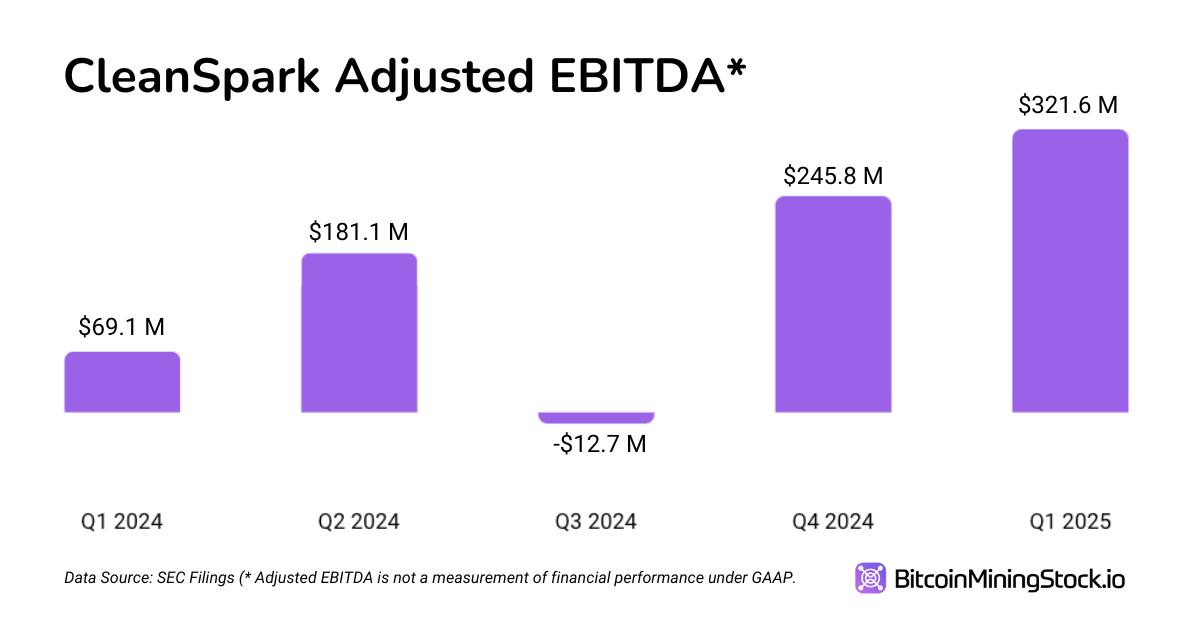

- Adjusted EBITDA: Set new records, ranging from $69.1 million to $321.6 million. (*This reported number includes a fair value earning of $228.2 million)

- Total margin: 57%, less than 60% year-on-year due to increased operational costs (particularly increased energy costs and mining infrastructure).

- Bitcoin production: 1,945 BTC, slightly down from 2,020 BTC in the first quarter of 2024 due to the Bitcoin Harving event in April 2024.

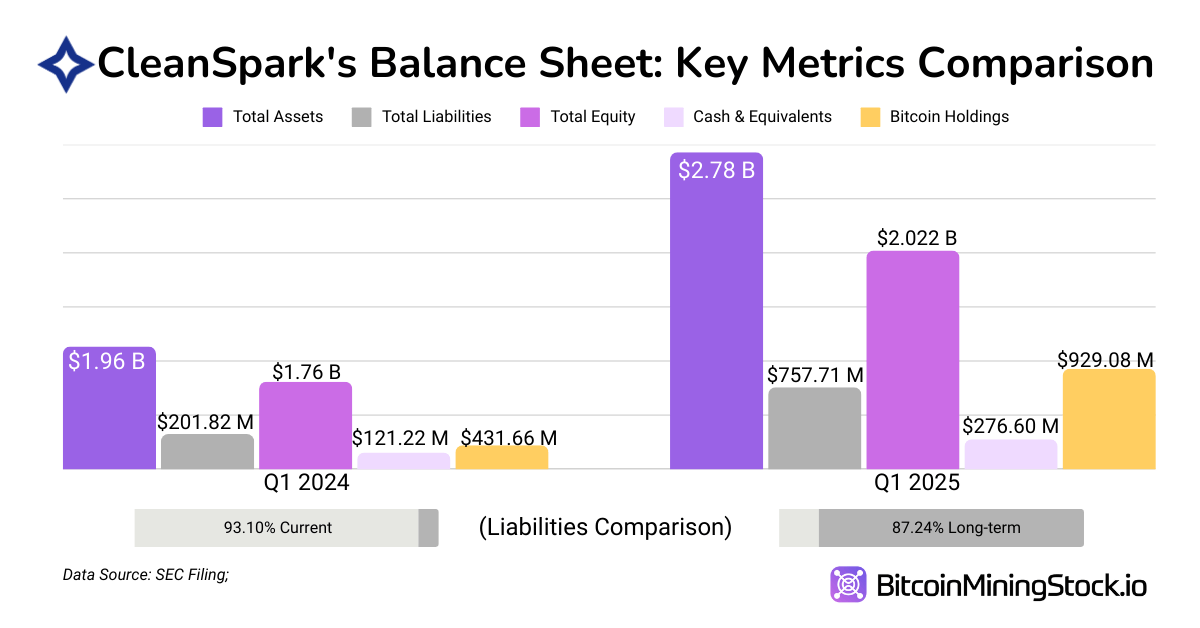

Key Balance Sheet Metrics

- Total assets: $2.78 billion (+41.6%) for the first quarter of 2024 vs. $1.96 billion. It is primarily driven by the expansion of Bitcoin Holdings and data centers and the increase in new mining infrastructure.

- Current Total Liabilities: A decrease of $96.7 million from $187.9 million, primarily due to loan repayments ($522 million repayments).

- Long-term debt: $641.4 million ($7.2 million) mainly due to the issuance of new convertible debts

- Shareholder fairness: $2020 million (+14.8%) for the first quarter of 2024, $1.76 billion

- D/E ratio: 0.32 (vs 0.08), This shows that CleanSpark has significantly increased leverage over the past year by undertaking more debt to fund growth.

Key Cash Flow Metrics

- Operating Cash Flow: $119.5 million net cash used in operations

- Investment cash flow: $255.9 million used (including $126.9 million for new miners and $57.4 million for fixed assets)

- Cash flow funding: $531.1 million inflows (+$635.7 million in loan revenue including $186.8 million in stock offerings – $145 million in Treasury stock repurchase)

- The company expects cash, BTC holdings and operational cash flow to be sufficient Over 12 monthsHowever, further expansion may require funding.

Evaluation Metrics and Enterprise Value

CleanSpark’s Currently, the market capitalization is $2.6 billion (Marketing closure on December 31, 2024)). To better understand that valuation, I have put together a few key financial metrics.

- Enterprise Value (EV): $2.16 billion (market capitalization + debt – cash and Bitcoin holdings).

- EV/evits ratio: 6.71x ($216 million/$321.6m). This is relatively low in high-growth Bitcoin miners.

- P/E ratio:10.57x ($261B/$246.8M). It suggests that the company is trading at a discount compared to high-tech growth stocks.

- BTC is held as a percentage of market capitalization: 35.6%, or more than a third of that rating, is supported by Bitcoin Holdings alone.

I’ll come back and compare it with other miners who have similar operational scales when the data is available.

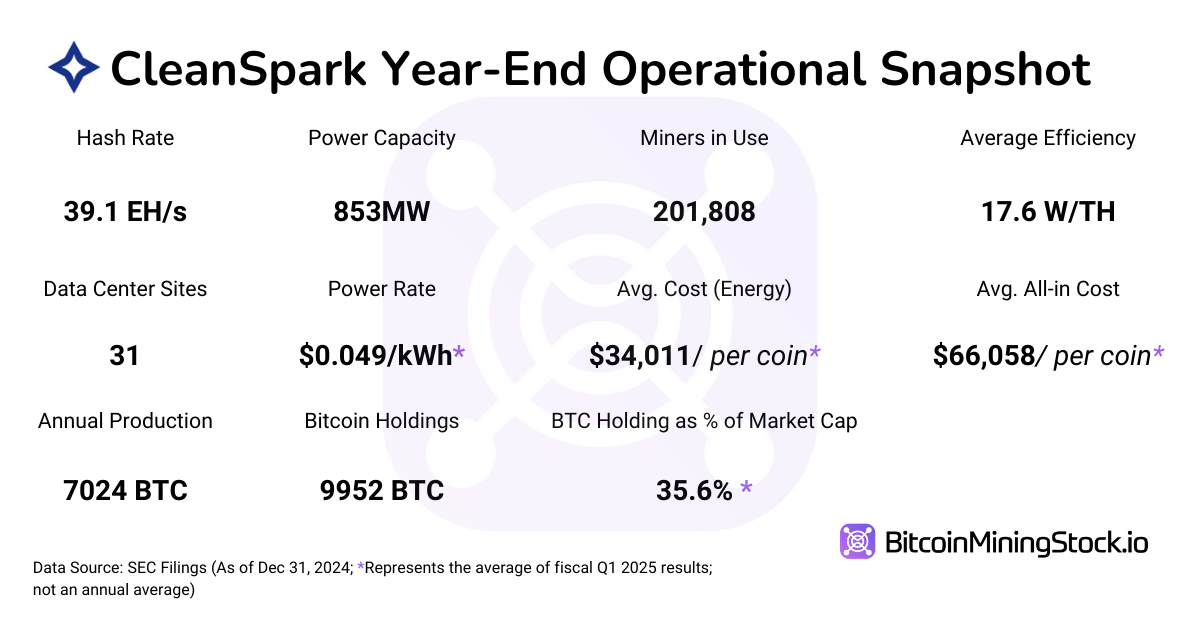

Operational Indicators: Improving Hashrate Growth and Efficiency

Key hashrates and efficiency indicators:

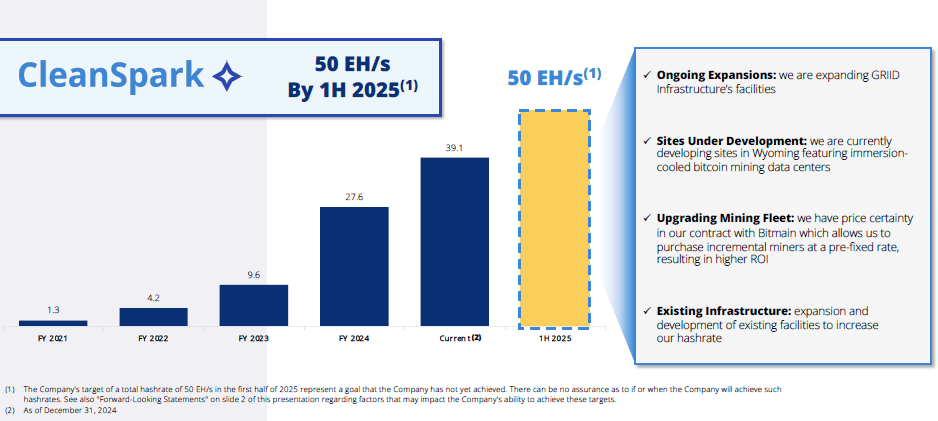

- Hashrate: 39.1 eh/s (4.87% of global hashrate), a quadruple increase in the previous year (first quarter 2024).

- Operating Minor: Since 201,808 and 88,559, when it is in operation.

- Average efficiency: Improved from 17.6 w/th and 26.4 w/th.

- Bitcoin production cost (direct energy costs per BTC at the property):$34,011, from before $12,808.

- Total cost per BTC (including depreciation and financing): Starting at $66,058, starting at $24,429.

Energy Cost Analysis and Mitigation Strategy

- Power Fee: $0.049/kWh (vs. $0.044/kwh yoy).

- 40.4% of Bitcoin’s revenues are used for energy costs, up from 35% year-on-year.

- Hurricane Helen has resulted in temporary operational cuts and reduced efficiency.

- Energy mitigation strategy:

- Diverse geographical expansion: New sites in Wyoming, Tennessee and Georgia have low power rates.

- Highly efficient mining rig: The S21 XT Immersion Unit will be deployed for low power draws.

- Flexible power contracts: A contract that optimizes energy usage and costs, but remains exposed to price volatility

Bitcoin Holding and Financial Strategy: HODL Over Sell

BTC Ministry of Finance:

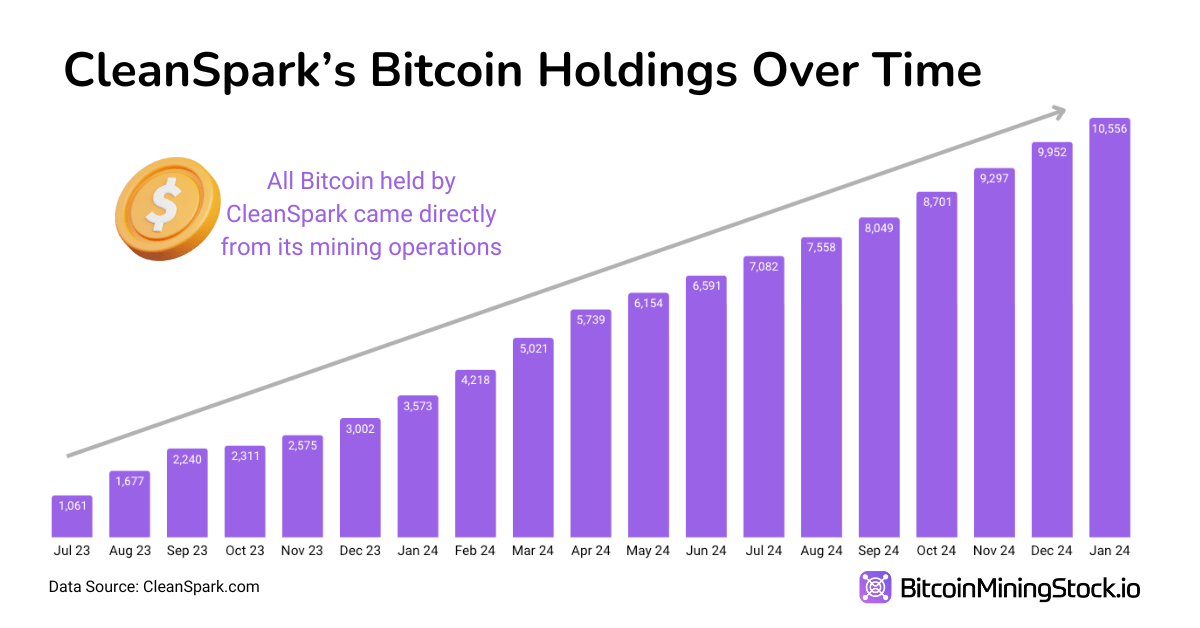

- Total Bitcoin was retained: 9,952 BTC (values $929 million from 6,819 BTC compared to the previous quarter).

- 99% of BTC in cold storage and 1% of hot wallets.

- BTC was sold during the quarter: 3,413 BTC (equivalent to $3.4 million) compared to 43,300 BTC ($43.3 million) in the first quarter of 2024

- BTC used as collateral (To Coinbase): $8.86 million was transferred and $129.18 million was acquired from the collateral account.

- Funding work: Instead of BTC sales, it relied on external financing (a conversion obligation of $635.7 million).

- No BTC lending or yield strategies have been reported.

Expansion & M&A: Scale up to 50 EH/s

Growth and expansion plans:

- goal: 50 Eh/s by mid-2025there are potential expansions 60 eh/s.

- New mining sites acquired:

- Tennessee Site: $29.9 million investment.

- Mississippi Site: $2.9 million in infrastructure in addition to $3 million investment.

- Fleet Growth:

- 60,000 S21 miners securedan option to buy 100,000 at $21.50/TH, 37% below the market price.

- Owned by 285,098 miners~83,290 are pending deployment.

CleanSpark’s Hash Rate Growth Roadmap (Screenshots of company presentations)

Thoughts: Big picture and important considerations

Looking at the figures in the financial report, we believe that CleanSpark holds a strong position in the Bitcoin mining sector. The company holds its position as a US Bitcoin miner that could potentially have an even more advantage under the current US administration.

But my main concern remains the Bitcoin price transfer. Historically, CleanSpark’s stock price has closely correlated with BTC’s performance. If Bitcoin surges, CleanSpark could be more attractive. However, if BTC stagnates or dips, CLSK could face a massive sale.

Another important factor to consider is How CleanSpark manages revenue across different market cycles. Unlike AI/HPC diversifying peersCleanSpark is committed to Bitcoin mining. Its CEO continues to be skeptical of HPC. Statement“Reusing Bitcoin mining facilities for high-performance computing is much more complicated than it looks,” reinforces Clean Spark’s long-term focus on Bitcoin as an efficient, proven, scalable business model. This indicates that it is unlikely that the company will immediately pivot like its peers.

That said, the company may find a way to strategically leverage its BTC holdings. Perhaps through a financial strategy that minimizes counterparty risk while increasing financial flexibility.

Ultimately, CleanSpark boasts one of its biggest mining operations: top range efficiency, disciplined capital management, excellent execution (beyond annual hashrate targets), and ambitious expansion plans. I currently have no strong reason to be weak about CleanSpark As long as Bitcoin mining is still a viable industry.

Even if we talk about current trends Bitcoin Financial StrategyCleanSpark can be an attractive investment opportunity. Compared to Strategy (MSTR), the most well-known proponent of this strategy, CleanSpark retains important benefits. They can get Bitcoin at a significantly lower price (all-in-cost: $66,058 per coin) by mining. As people say “If you can mine at a lower price, why would you buy it?”