Bitcoin’s price fell below $67,000 this weekend after a steep decline that saw it drop more than 40% below its October 2025 high. In February, BTC was down about 47% from its highs near $126,000.

In previous versions of this market, this kind of decline caused all sorts of ugly reactions and spread far beyond the spot market. Fear will spread like wildfire, long-term holders will flee, and selling will grow on its own.

But this time, that almost never happened.

The most interesting part of this decline was not the price change itself, but the movement around it.

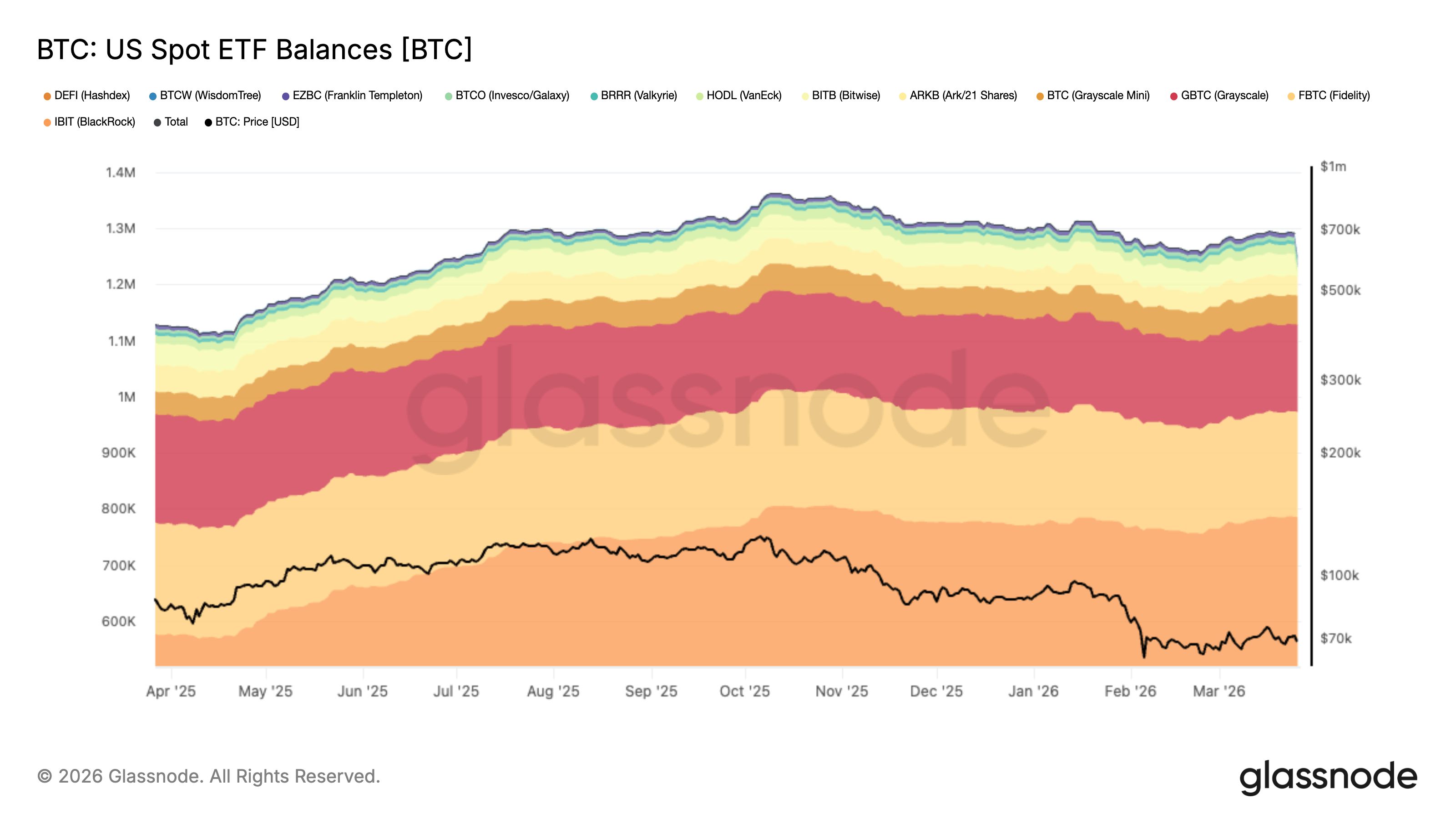

Despite such a large drawdown, the US Spot Bitcoin ETF complex has held up much better than anyone expected. Eric Balciunas, chief ETF analyst at Bloomberg, said in February that only about 6% of ETF assets remained during the decline.

The arrival of the Spot Bitcoin ETF has always been seen as a gateway moment for cryptocurrencies, but now, with the market under immense pressure, a bigger change may be on the horizon. Bitcoin has a new class of holders, but they don’t seem to be too keen on the first signs of pain.

The SEC approved Bitcoin spot trading products in January 2024, and trading began the next day. This was followed by the largest product launch in ETF history.

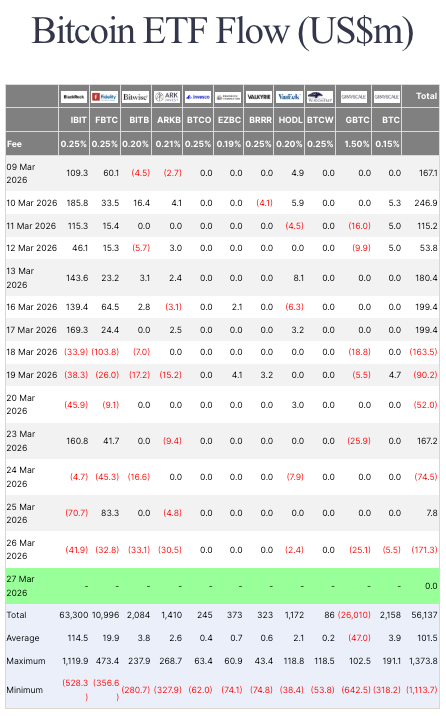

As of March 27, cumulative net inflows across U.S. spot Bitcoin ETFs since launch were approximately $56.1 billion, according to Pharcyde data. BlackRock’s IBIT alone accounted for about $63.3 billion, while Fidelity’s FBTC brought in about $11 billion. In contrast, Grayscale’s GBTC suffered losses of about $26 billion.

There have been real sell-offs within this category, some of which have been quite large. But overall, ETFs continued to attract money anyway.

Therefore, even when Bitcoin suddenly fell, the ETF did not fall along with it.

The daily flow situation is still unstable, but in line with everyone’s expectations. According to Pharcyde data, there was a net inflow of $167.2 million on March 23 and a net outflow of $171.3 million on March 26. Perfect peace probably won’t come anytime soon, especially given the ongoing geopolitical turmoil, but it is relatively resilient. A deep downturn arrived, and the mass exodus that many had expected did not actually occur.

new bitcoin holder

The ETF wrapper has changed who can own Bitcoin and how they can own Bitcoin. Rather than residing on exchanges or wallets, BTC has moved into an institutional product within a well-known investment structure.

ETFs brought Bitcoin to institutional investors, but this adoption worked both ways. In other words, it brought Bitcoin to institutional trading as well. While some of the initial movement for Bitcoin ETFs may have been large Bitcoiners seeking regulated exposure, the space quickly became saturated with people looking to profit from its liquidity and volatility.

CF Benchmarks examined 13F filings and found that much of hedge fund exposure to Bitcoin ETFs is tied to basis-style trading rather than long-term conviction. SEC rules also make clear that 13F filings arrive late, so you see a historical snapshot rather than real-time behavior. Still, they help show how broad the investor base has become.

That distinction is important. When I say Wall Street barely blinked, it doesn’t mean no one sold because BTC lost half its value. What this means is that the ETF complex experienced a painful decline without the mass withdrawal that once seemed inevitable.

This becomes even clearer when we look at individual funds. IBIT remains a huge winner in this category, but FBTC has also built a large base and GBTC continues to see asset outflows. We’ve seen strong inflows to the big funds, steady support for several others, and continued outflows from older incumbents.

A different rhythm crash

Gold may be the best comparison for the impact of Bitcoin prices on ETFs.

In 2013, a sharp drop in gold prices led to a massive outflow of gold-backed ETFs. The World Gold Council announced that by the end of April 2018, 350 tonnes had leaked, reducing its holdings by 12.9%.

However, the Bitcoin ETF base appears to be different. Although the damage to prices was far more severe than that experienced by gold, the exit of large holders did not occur.

Nevertheless, Bitcoin is far from stable at the moment. On March 26th alone, there was a net outflow of $171.3 million from the ETF, and the price continues to fluctuate wildly as news emerges regarding developments in the Iranian situation.

But holders’ reactions are changing, and that may be the most important change brought about by the ETF era.

There are two ways to read this. For one, ETFs have taken a stronger hold and brought investors more willing to treat Bitcoin as part of a broader portfolio. The other is that even if the sell-off simply slows, a bigger macro shock could test its patience later. Both possibilities are possible, as the data has not yet resolved the debate.

Whatever the future outcome, this change in ETF behavior has revealed something new about how Bitcoin behaves under stress. A 40% crash looked like a full-blown bear market panic, but it’s a common stress test in this ETF-dominated market. After just a year of rising prices, prices have fallen significantly, but ETF holders, at least overall, have held up much better than anyone expected.

And this may be the clearest sign that Wall Street has changed the way it sells Bitcoin, not just buys it.

(Tag translation) Bitcoin