When the net present value of Stretch (STRC), a dividend-yielding preferred stock issued by Strategy (formerly MicroStrategy), is calculated, the results are disappointing for MSTR shareholders.

Michael Saylor expects STRC to somehow fund trillions of dollars worth of Bitcoin ($BTC) to purchase his common stock for the shareholder. However, while STRC raises capital, it mathematically generates a positive profit. $BTC MSTR’s yield is actually quite expensive over the long term.

Strategy promotes these immediate $BTC Purchase as an upfront benefit of STRC to MSTR common stockholders.

He happily praises me $BTC yield, surplus $BTC MSTR shareholders can enjoy today with the acquisition by Strategy. $BTC From the cash received from selling STC.

STRC is raising capital now and directing all maintenance costs to the future, which clearly improves the company’s current balance sheet. Like any other fundraising activity, Strategy promises future profits in exchange for current capital.

Read more: Michael Saylor’s Spinal Tap ad says STRC is like a bank account, but it’s not

11.5% dividend

Despite the changing terms of the STRC, such as variable and semi-fixed interest rates, it is possible to estimate the value of the STRC today.

While no one has offered to buy STRC outright from Strategy, a theoretical calculation of the value of this asset would indicate its actual value to the company’s common shareholders, rather than a misleading value. $BTC Yield index ignores all future obligations of STRC.

Specifically, STRC pays an annualized dividend of 11.5% in monthly cash installments.

Although the dividend rate is variable and subject to suspension at the discretion of the Board of Directors, prospective buyers may use the 11.5% dividend rate in their calculations.

In fact, if STRC trades significantly below its $100 par value (also known as the “official price”) in the future, as it has in the past, the company may need to increase its percentage even further to encourage bids from Nasdaq traders.

Additionally, if STRC trades far above the specified amount of $100, the rate may be lowered.

Basically, using the 11.5% dividend rate as is is a good starting point for your calculations. This interest rate is the one currently selected by the company, and the market is currently pricing STRC based on its dividend.

Is it worth comparing STCs to junk bonds?

Assuming that a purchaser of a bond portfolio is interested in STRC, he or she may compare its dividend interest rate to the average yield of junk bonds. In fact, the strategy itself has a junk credit rating of “B-” by S&P.

Thaler has repeatedly compared STRC to high-yield bank accounts and money market funds, despite having no deposit insurance, no guarantee of maintenance of principal value, no guaranteed interest payments, no sustained market bidding to support secondary trading at par, and a 9.8% change in value over the past four months.

Still, many crypto investors first learned about high-yield bonds through STRC’s retail-focused ads. These include various X ads and Spinal Tap appropriations that claim that dividends are somehow “income” and can “stretch” the typical money market rate of 3-4% to 11.5%.

Although STRCs are not bonds, their marketing promises are very similar to bond offerings, emphasizing monthly payments, annualized interest rates, and vague hints that the value of the principal invested may be stable.

It contains extensive documentation of the strategy’s attempts to pull financial levers should STRC fall significantly above or below its $100 par value.

Of course, a company paying 11.5% to raise capital is itself a red flag. Investment grade corporate bonds pay approximately 5%. Even the riskiest Baa-rated companies, one step short of junk, pay an average of 6.1%.

The 11.5% interest rate is much higher than junk bond interest rates, which average nearly 7%.

In fact, the average junk bond yield of 7% provides a starting point for calculating and questioning the net present value of STRC relative to a junk bond portfolio.

Huge credit spread of 450 basis points above average junk yield, yet no principal repayments and there is no expiration date, STRC’s 11.5% dividend is so high that it seems more like an annuity than a bond.

Calculate STRC like a pension

In contrast to bonds, annuities can be structured to pay almost any annual interest if the payment period is short enough. If you give a pension company $1 million and ask for 10% simple interest for 10 years, they’ll be happy to oblige.

This is free money for the pension company, and for 10 years you will only be repaying the principal while enjoying the investment yield on the balance.

In fact, STRC is much more comparable to a custom annuity than a bond, as it is a choose-your-own-adventure product that Strategy stripped of its 11.5% dividend rate at its sole discretion.

Additionally, there is an established and relatively liquid market for pension settlements.

Pension settlement Provides a reference point for a one-time cash payment for an instrument that never repays the principal or matures. While STRC could theoretically pay dividends over centuries, limiting that dividend to the lifetime of a person like Thaler is probably a more realistic starting point than infinity.

STRC’s cash settlement estimate in the form of an annuity is compared to the value of another annuity paying the average yield on junk bonds, or 7%, and must be discounted from the bond’s principal repayment at maturity.

Unlike bonds, classic income annuities typically do not have their principal repaid at any time. Instead, similar to STRC, it irreversibly converts principal capital into a payment stream over the policyholder’s lifetime.

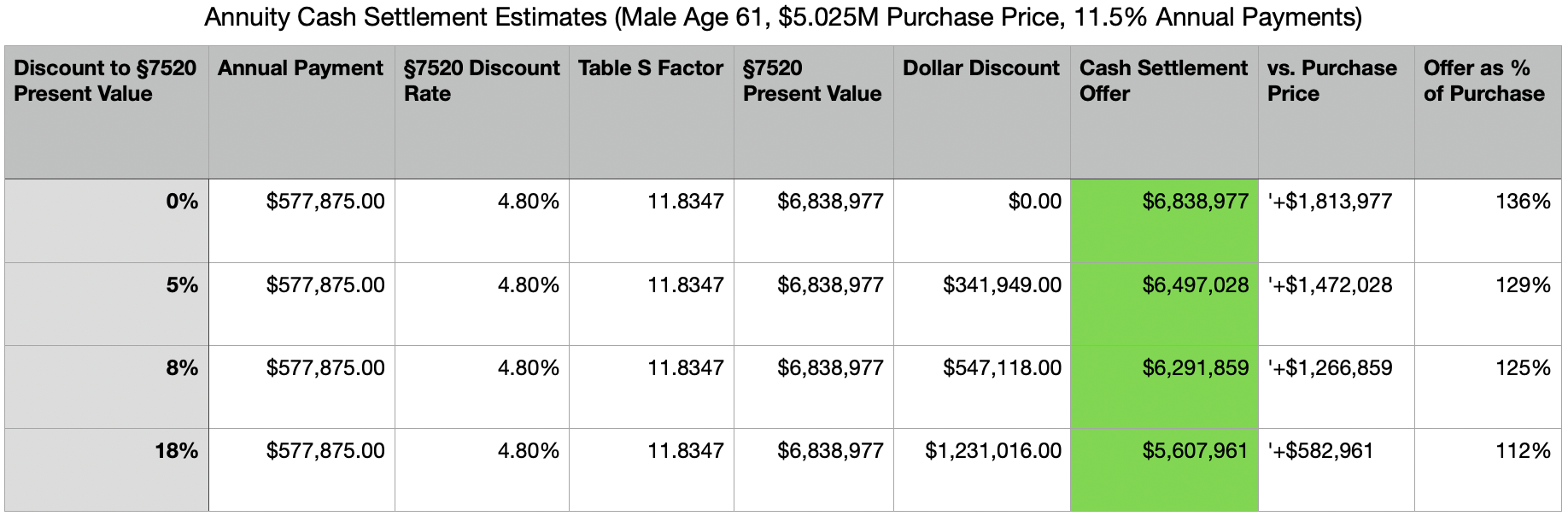

What is the value of a $5 billion annuity that pays 11.5%?

If we run a classic life annuity of $5.025 million into an actuarial calculator that pays 11.5% annually until the death of a 61-year-old American male policyholder, the same age as Saylor, cash settlement offers for this annuity buyout range from a fairly low 18% discount bid of $5.6 million to a more realistic and fair market discount of 8%. 6.3 million dollars.

Simply replace 1 billion with the word 1 million above to convert to the net present value of STRC’s notional principal balance of $5.025 billion.

Of course, STRC is not legally bound to anyone’s lifetime, and dividends can in principle continue indefinitely or be cut early.

Using Sailor’s life to cover the horizon is a simplistic assumption and not an inherent property of STRC.

Yes, it’s a theoretical pension of $5,025,000. Get instant value with cash payments Because the generous 11.5% yield creates instant value on the secondary market. Such payments are usually from creditworthy issuers for the obvious reason that they are not available elsewhere.

The discounts mentioned above, such as 8% and 18%, are calculated based on the annuity’s mathematical value as defined in IRS Publication 1457, also known as a Section 7520 valuation.

For an equal payment annuity under §7520, its present value is calculated using the §7520 interest rate and the appropriate mortality table.

In layman’s terms, the net present value, or the entire stream of future payments valued today in today’s dollars, is equal to the dollar amount of each annuity payment multiplied by an IRS-defined annuity factor that provides discount rates and mortality assumptions based on age and gender.

The actual negotiated range was approximately $6 million, which corresponds to the 5% to 10% discount rate band that makes up the majority of pension “settlement” bids.

The 11.5% interest rate is very high compared to current market rates, and buyers have a strong incentive to compete, so a well-negotiated deal with multiple competing bids could approach $7 million.

The fair value floor is actually more than the principal, which is more than $6 million. This is because the annual cash yield of 11.5% creates an immediate positive carry rate from day one, compared to other institutional investors’ average cost of capital of 6-7%.

An offer of less than $6 million is likely to be predatory with a discount rate greater than 18%, which would unfairly penalize the seller and primarily benefit the buyer.

In other words, even though STRC has not promised to repay the principal, The net present value of Saylor’s future cash flows over its expected life, discounted at 11.5%, is probably worth about $6-7 billion.or the full amount of the outstanding notional notional amount of $5.025 billion.

Again, if you want to substitute a realistic pension figure measured in millions, simply replace the word billion and use the analogy with STRC.

Additional considerations

Of course, buyers and sellers in this hypothetical scenario could argue over how much STRC’s dividend rate would change. After all, STRC is a floating rate.

Additionally, there may be a discussion on whether STRC will maintain its $100 par value on the secondary market, i.e., on the Nasdaq.

If a buyer was somehow 100% sure that STRC would maintain its $100 par value by the end of Saylor’s life, he might bid $5 million or more for the entire STRC product today, or $10 billion to $12 billion.

Of course, at the time of writing, STRC is near a sub-peg at $99.75, so no one is actually bidding more than $200 on STRC right now.

Therefore, the market somewhat agrees with the annuity comparisons above. However, there is little belief that STRC can maintain its sub-$100 peg long-term, so this comparison is ignored.

The discounted net present value of STRC’s future cash flows is actually worth at least $1 billion more than its $5.025 billion face value, assuming it actually pays dividends at an annual rate of 11.5% over Mr. Saylor’s lifetime. If the bidder had been confident that STRC would still maintain its par value on Nasdaq by the end of Mr. Thaler’s life; Should be worth more than twice as much Current stock price is $100.

So how, exactly, does Strategy expect a product worth far less than the cash-settled value of its peer annuity to compensate for its lack of confidence and still take advantage of all future payments?

The market argues that STRC’s current market capitalization of $5.012 billion does not allow it to be worth more than the $5.024 billion face value it raised to finance the acquisition. $BTC.

The only way this works is $BTC Gathering. a lot.

In order for STRC trading to work for your strategy, $BTC You need to achieve growth rates well above 11.5% per year.

If so $BTC If you collect 30% annually, it will pay for itself.

As always, STRC’s generous 11.5% dividend only makes sense if: $BTC It is valued far above that rate. For example, it could rise in line with Saylor’s ultra-bullish forecast of 30% annual growth.

Obviously, it’s easy to buy something that sells for 11.5% and appreciates 30%, as long as that thing actually appreciates 30% a year.

Unfortunately, over the past five years, $BTC There’s nothing like an annual increase of nearly 30%. In fact, it has only increased by 30% in five years.

In Sailor’s mind, $BTC Those shortcomings will soon be compensated.

That’s better. All about strategy $BTC-Since acquisition efforts are losing money on average, Mr. Thaler needs to: $BTC To gather desperately. The company’s average cost basis is $75,696, or 5% higher. $BTC I was trading today.

In summary, the results of STRC’s annuity-style cash liquidation valuation and STRC’s real market capitalization are both consistent with the above-par value of the STRC that financed the purchase. $BTC: 5 billion dollars.

However, STRC is actually trading at a market capitalization equal to its face value, so Currently, the market is giving Strategy shareholders no more return on STRC than the initial capital raised by STRC last year for the acquisition. $BTC.

There may be $BTC Although MSTR’s yield per share is high, MSTR does not enjoy any benefit from STRC when measured in USD.

To make matters worse, the company will have to pay STRC dividends indefinitely, even though the market has not given STRC more than par return on that promise today.

These future obligations will adversely affect the Company’s profitability and cash flows for many years to come.