Bitcoin is nearing a point where the market has to choose between two very different outcomes. Traders are still paying to continue shorting, but prices, ETF flows, and market leadership are no longer behaving as if the market is in the midst of a collapse.

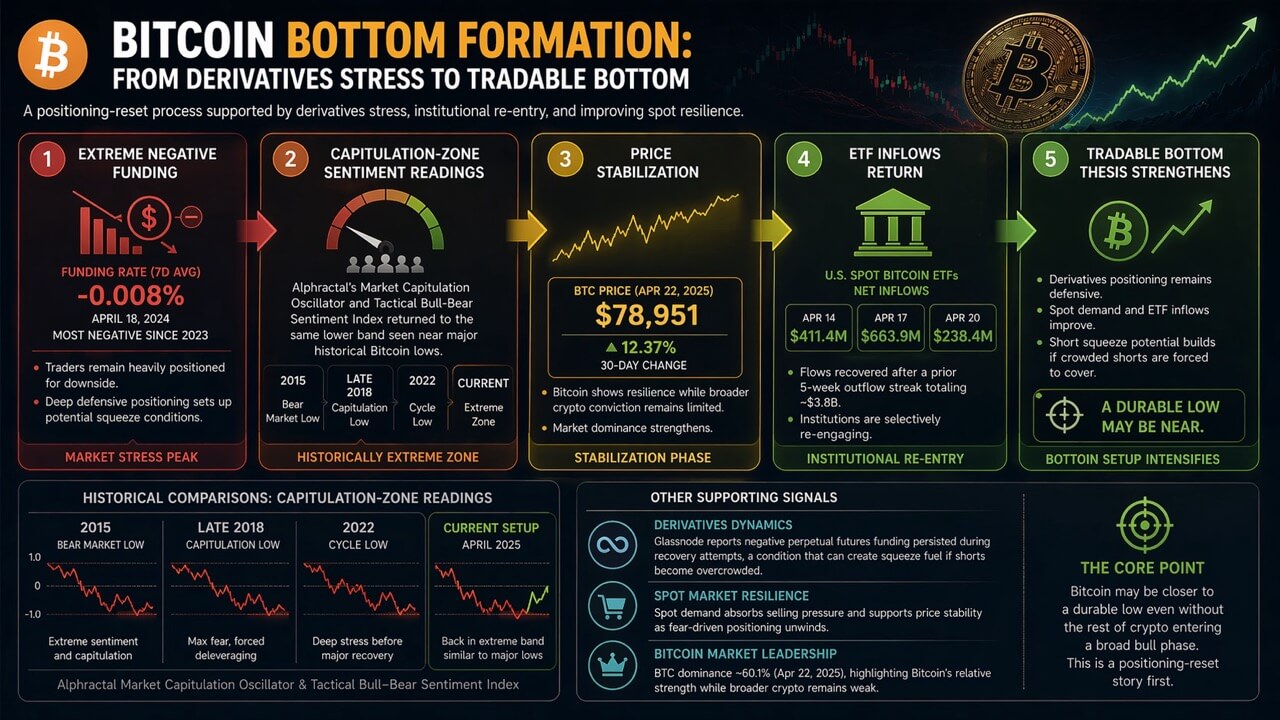

In a recent X post, Alpharactal analysts claimed that Bitcoin funding rates have reached their most negative levels since 2023, and said their proprietary model points to the possibility of a regional bottom.

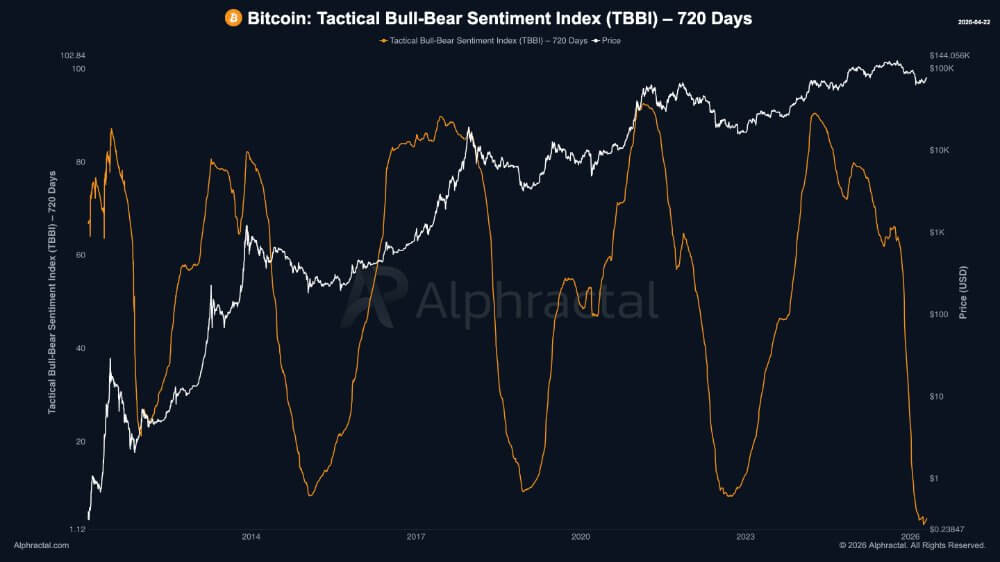

They used their “Market Calm Oscillator and Tactical Bullish-Bearish Sentiment Indicator” to claim that Bitcoin fell into the same extreme zone that previously appeared near major Bitcoin lows.

In the chart below, the sentiment index has fallen into deep troughs near early cycle washouts, including the 2015 bear market bottom, late 2018 capitulation, and 2022 low.

The latest readings show the indicator returning to the same lower range, supporting the broader argument that market positioning has once again reached an unusually stressed level.

Therefore, Bitcoin appears to be trading in a zone where capitulation and eventual reversal previously occurred simultaneously. Other market data shows similar findings.

Crypto.com announced on April 18 that its seven-day average funding rate had fallen to approximately -0.008%, the lowest figure since 2023, while Glassnode said negative funding continued despite Bitcoin stabilizing and spot conditions improving.

As a result, the market falls into an abnormal state. Bitcoin may be emerging from a positioning washout that could support a tradeable rebound. Alternatively, the same macro pressures that caused the drawdown may still be strong enough to cause an even deeper leg down.

crypto slate The Bitcoin price page shows BTC at $78,951 as of April 22nd, with an increase of 12.37% in 30 days and a market power of 60.1%. While the market is not indicative of a widespread speculative breakout, it does indicate that the asset is regaining leadership while confidence remains thin elsewhere.

This distinction is at the heart of the real problem. Bitcoin could approach a permanent low while the rest of the cryptocurrencies are not yet ready for a full bull market expansion.

Why has it become harder to dismiss bottoming cases?

The bullish case is gaining support as spot demand holds up while derivatives positioning remains defensive.

Glassnode described a market where perpetual futures funding remained negative even as Bitcoin tried to recover from a drawdown. Continued negative funding could provide upside potential if short funding becomes more concentrated and prices start to move against the shorts, but it also shows that leveraged conviction remains cautious.

The signal becomes more interesting now that the price has stopped following the same bearish script. Bitcoin is trading less like an asset trapped in a one-way liquidation and more like an asset that has found a buyer willing to absorb macro fears.

Those buyers are showing up in one of the cycle’s most important channels: the ETF complex. According to Farside Investors, the US Spot Bitcoin ETF attracted $411.4 million on April 14, $663.9 million on April 17, and another $238.4 million on April 20.

This flow pattern indicates that larger allocators did not disappear when the market became tense.

The rebound also looks more believable because it involves an actual institutional reset. By early March, The Spot Bitcoin ETF had already experienced five consecutive weeks of outflows totaling about $3.8 billion by the time inflows began to pick up in early March.

This initial washout helps define your current setup. Agencies appear to have hedged their risks and are now resuming efforts more selectively.

If this process continues while funding remains negative or only gradually normalizes, the short side will become more vulnerable to pressure than the current mood suggests. This is the strongest version of the bottoming case, and there is no need to declare that a full-cycle bull market has already begun.

Why Macro and Policy Still Suppress Upsides

The market will decide whether this tactical rebound turns into something broader and more sustained. This makes it difficult to ignore constraints.

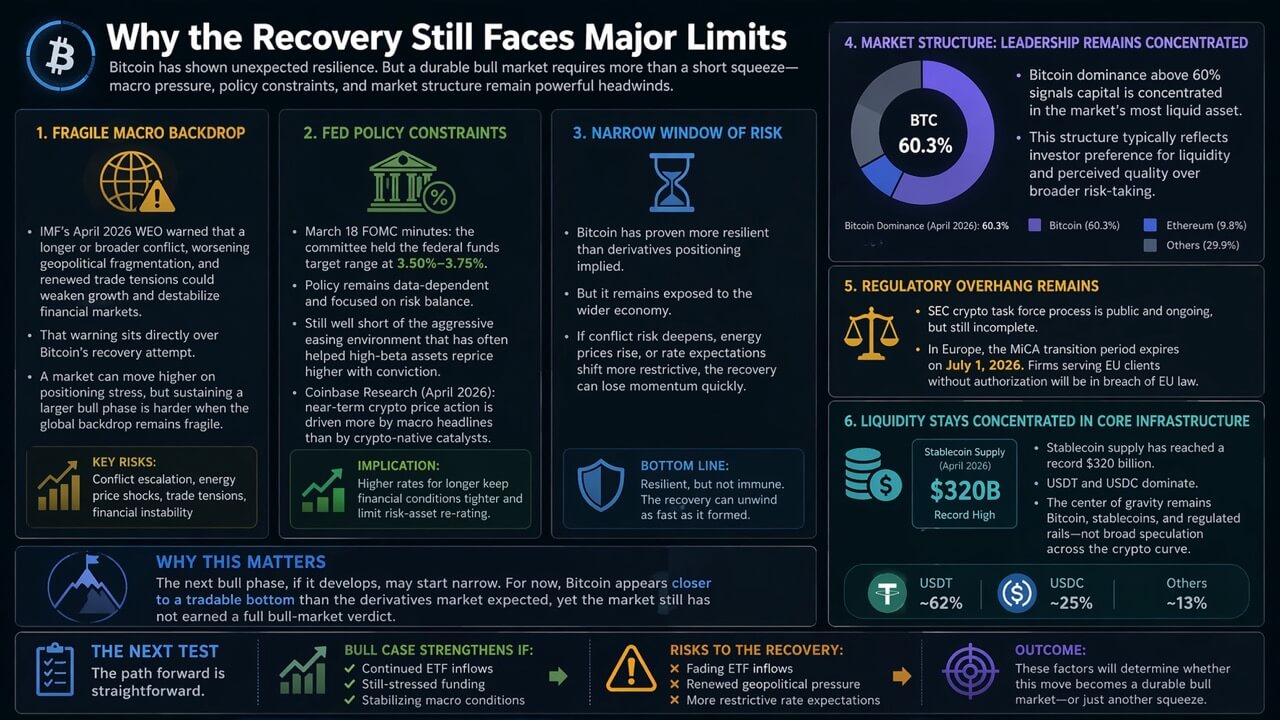

The IMF’s World Economic Outlook for April 2026 warned that prolonged or widespread conflicts, worsening geopolitical divisions, and renewed trade tensions could significantly weaken growth and destabilize financial markets. This warning applies directly to Bitcoin’s current recovery attempt.

The market may be further compressed by positioning stress. If the global macro environment continues to deteriorate, it will be difficult to sustain the broad bullish trend.

The pricing situation reinforces that ceiling. Minutes from the March 18 Federal Reserve Board meeting showed that the committee maintained its target range for federal funds at 3.5% to 3.75% and remains focused on available data and risk balance.

This is still a long way from the aggressive easing cycle that has historically contributed convincingly to a rally in prices for high-beta assets. Coinbase Research reached a similar conclusion in its April outlook, arguing that short-term crypto price movements are driven more by macro headlines than crypto-native catalysts.

Therefore, Bitcoin remains within a narrow but important window. While derivatives markets appear to be more resilient than expected, they still don’t appear to be isolated from the broader economy.

The recovery could quickly decline in altitude if conflict risks worsen, energy prices tighten financial conditions further, or interest rate expectations move in a more restrictive direction.

Why the next bull phase could start narrow

The broader crypto market structure also argues against calling for a full-spectrum bull market right away. According to , Bitcoin’s dominance is over 60% crypto slate Market data suggests that leadership is concentrated in the most liquid assets in the market.

This typically occurs when investors prioritize liquidity and perceived quality over broader risk. It fits into the current environment and policy context.

The SEC’s Crypto Task Force page shows a regulatory process that is currently underway and open to the public, but is still incomplete. In Europe, the MiCA transition period ends on July 1, 2026, after which any company providing services to EU customers without authorization will be in breach of EU law.

This is a more formal setup than the loosely regulated period that drove previous crypto rallies. The market is maturing, but under greater scrutiny.

At the same time, money within cryptocurrencies continues to flow through the industry’s pipes. Even as the US government continues to work on market structure legislation, stablecoin supply has reached an all-time high of $320 billion, with USDT and USDC dominating liquidity.

This proves that the current cryptocurrency zeitgeist is still centered around Bitcoin, stablecoins, and regulated rails rather than broad speculative breadth.

If a larger bullish phase eventually occurs, it may start from a narrower base rather than reaching it all at once across the risk curve.

For now, Bitcoin appears to be closer to a tradeable bottom than the derivatives industry expected, but the market has yet to reach a full bull market verdict.

AlphaRactal’s chart shows the sentiment index plummeting to extreme lows near several major bottoms for Bitcoin, indicating that sentiment and positioning appear to be returning to historic capitulation zones rather than a normal decline.

Still, while static charts can support the pattern qualitatively, they are not accurate enough by themselves to verify the timing language of local bottoms that form within 21 days.

The next test is clear. If ETF inflows continue to rise, funding remains negative or normalizes only slowly, and macro stress stabilizes, the bottom becomes more likely to persist.

If capital inflows weaken or geopolitical and interest rate pressures pick up again, the current rally could become more of a squeeze than the beginning of a new bull market.

(Tag translation) Bitcoin