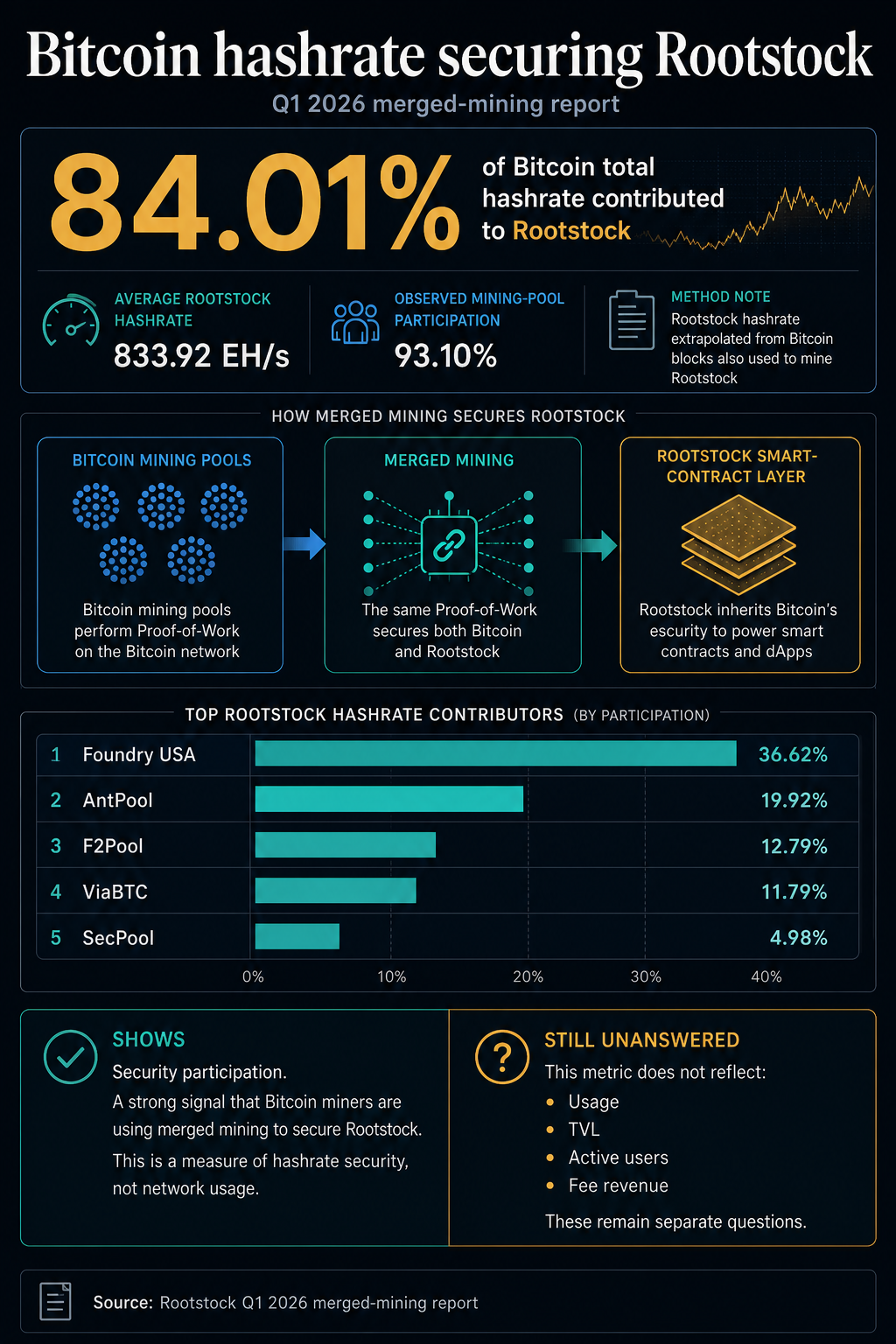

Bitcoin miners are already doing more than securing Bitcoin’s base chain. According to Rootstock’s Q1 2026 merged mining report, 84.01% of Bitcoin’s total hashrate contributed to Rootstock’s security during the quarter, giving Bitcoin DeFi a hashrate-backed security claim.

The average Rootstock hashrate of the network was 833.92 EH/s.

This number is surprising because Rootstock sits next to Bitcoin, rather than competing for another set of machines. This is a Bitcoin sidechain that uses merge mining, allowing Bitcoin mining pools to send their work to Rootstock while continuing to mine Bitcoin.

Rootstock’s framework allows miners to earn additional BTC denominated rewards from Rootstock network fees without adding hardware or disrupting Bitcoin operations.

Precision is key. This metric tracks hashrate contributed through mining pools, rather than the intent of individual miners, leaving the demand in DeFi unresolved.

This indicates that a large portion of Bitcoin’s hashpower, as measured by Rootstock’s Q1 methodology, is also used to secure the Bitcoin smart contract layer.

This turns this report into a signal for mining and Bitcoin DeFi infrastructure. Bitcoin DeFi, often referred to as BTCFi, is a broader category that Rootstock seeks to secure through merge mining.

The next signal is whether the security will have meaningful fee income, liquidity, and user activity.

What the hashrate number means for Bitcoin DeFi

Merge mining allows miners to mine multiple compatible proof-of-work chains simultaneously. crypto slate Our own glossary defines merge mining as mining multiple cryptocurrencies without sacrificing hashrate.

In the case of Rootstock, the practical argument is that Bitcoin miners can reuse existing infrastructure to protect Rootstock while still focusing on Bitcoin.

Rootstock said 93.10% of the observed mining pool hashrate participated in merged mining during the first quarter. The full report lists Foundry USA, AntPool, F2Pool, ViaBTC, and SecPool as the companies most contributing to Rootstock’s hashrate.

Foundry USA accounted for 36.62% of Rootstock’s reported distribution, followed by AntPool with 19.92%, F2Pool with 12.79%, ViaBTC with 11.79%, and SecPool with 4.98%.

Participation in a mining pool will determine whether merge mining remains a niche technical option or becomes a layer of security backed by the main Bitcoin infrastructure.

A chain secured by a small pool of marginal hashing power carries a different risk profile than a chain that receives work from a pool that is already near the center of Bitcoin mining.

Rootstock’s Bitcoin hashrate data uses a 7-day average from blockchain.com, and its Rootstock hashrate is estimated from the share of Bitcoin blocks that are also used to mine Rootstock blocks.

In this way, this number becomes an indicator of security participation. Wallet usage, lending activity, transaction volume, and protocol revenue require separate measures.

| What the diagram shows | What remains unresolved |

|---|---|

| In the first quarter, a large portion of Bitcoin hashrate contributed to Rootstock’s security. | Whether individual miners made Rootstock decisions independently. |

| The main Bitcoin mining pool was part of the Rootstock security base. | The amount each pool or miner earns from Rootstock fees. |

| Bitcoin’s proof of work is already being reused to secure smart contract infrastructure. | DeFi usage, TVL, active users, product-market fit. |

Hashrate explains the security floor, and fees and usage explain whether that floor is valuable to the broader Bitcoin economy.

Pool distribution also belongs at the top of the discussion. High headline ratios can hide concentration, and Rootstock’s own tables show that the security infrastructure relies heavily on a small group of large pools.

Why miners care now

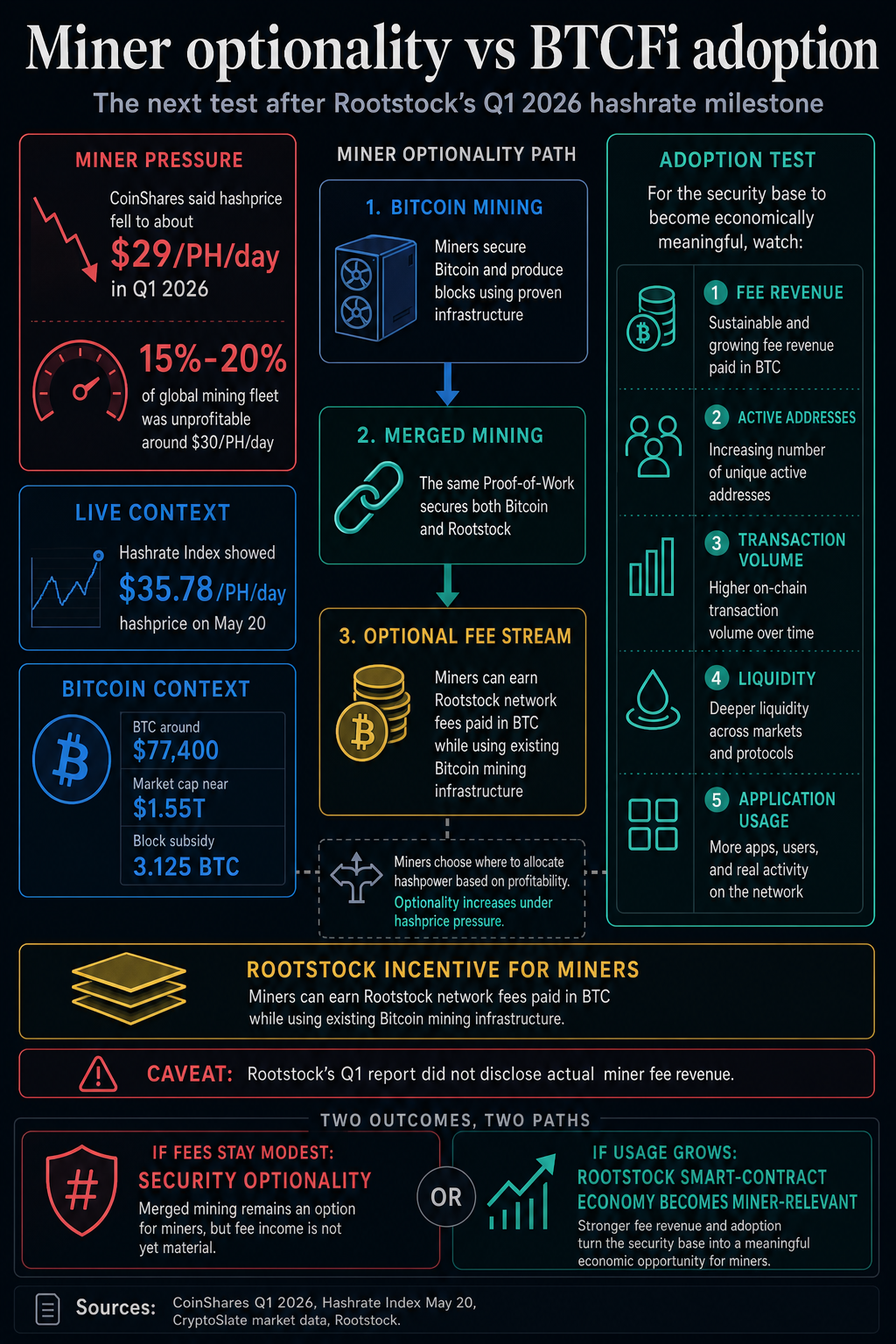

Bitcoin mining margins are under pressure. CoinShares’ Q1 2026 Bitcoin Mining Report states that Q4 2025 will be the toughest quarter for miners since the April 2024 halving.

The company said that the hash price was compressed due to Bitcoin’s price decline in late 2025 and increased network competition. In the first quarter, it fell further to around $29/PH/day, with CoinShares estimating that 15% to 20% of the world’s mining fleet is unprofitable at around $30/PH/day.

The hash rate index hash price is $35.78 PH/day, and the hash rate of the Bitcoin network is 984.34 EH/s.

According to firememecoins market data, BTC is trading at around $77,300, with a market capitalization of nearly $1.55 trillion, while Bitcoin has a 60.1% edge in its market rankings.

At that price, the 3.125 BTC block subsidy remains the core mining reward. If miners manage hardware updates, power costs, financial turnover, AI or high-performance computing opportunities, the flow of additional fees is easier to understand from a business perspective.

Rootstock’s suggestion to miners is that pools can use the same proof of work but add another source of fees. This is a modest claim, but it’s also why Q1’s hashrate numbers are more broadly relevant.

Merged mining allows Bitcoin miners to keep their main operations fixed in Bitcoin while gaining the option of increasing BTCFi fees.

For BTC holders, the meaning is different. If miners can secure Bitcoin’s native smart contract infrastructure without redirecting hashing power away from Bitcoin, then part of the BTCFi stack is already connected to Bitcoin’s economic engine.

The security foundation exists before the market value of that infrastructure is determined.

The Q1 number comes first as an option for miners and second as a challenge for builders. This means translating a strong security infrastructure into normal economic activity.

The impact on revenue remains to be quantified. According to Rootstock’s scheme, merge mining makes sense even with small fees because the incremental operational burden is limited, but the importance still depends on the actual flow of fees.

When security needs to turn into usage

Hashrate can increase faster than usage. According to Messari’s State of Rootstock Q1 2025 report, Rootstock’s combined mining participation rate averaged 81% in the same quarter after the Foundry and SpiderPool merger.

In the same report, Messari recorded a decline in user metrics, including a decrease in active addresses, a decrease in new addresses, and a decline in DeFi TVL.

This early split is an important caveat to the new numbers for Q1 2026. A large number of participants in merge mining can make the network difficult to attack, but whether a secure network becomes economically viable depends on the borrowers, traders, stablecoin liquidity, and developers.

While security is a prerequisite for financial activity, toll revenue and usage indicate whether people are using the rails.

The available Q1 2026 mining report leaves off the table the most important number regarding miner economics: the actual Rootstock fee income to miners.

Rootstock said that although rewards are paid in Bitcoin from network fees, the first quarter mining report focuses on hashrate participation and pool distribution rather than a breakdown of miners’ revenue.

The small size of Rootstock’s token economy further strengthens that warning. crypto slate According to market data, rBTC, the Bitcoin-pegged asset used by Rootstock, has a market capitalization of approximately $19.9 million. RIF, the Rootstock Infrastructure Framework token, is large at approximately $74.4 million, but still modest by crypto sector standards.

Taken together, these numbers show that Rootstock’s security footprint is much larger than the market value currently attached to its core ecosystem assets.

Rootstock showed that most Bitcoin hash rates can secure the BTCFi infrastructure through merge mining. However, activity and fee data are still needed to show that the infrastructure has become economically important to miners and BTC holders.

The next test is economics. If Rootstock’s fee income, active addresses, trading volume, liquidity, and application usage remain modest, merge mining will appear to be a valuable option for miners and a security feature for users.

If these metrics grow with continued participation in the mining pool, the discussion changes. Bitcoin hashrate will help miners earn revenue from the real Rootstock smart contract economy secured through merge mining.

For now, Rootstock’s 84.01% figure makes the case for Bitcoin DeFi infrastructure even stronger. This shows that Bitcoin’s smart contract layer can do most of the Bitcoin mining work on top of it, while miners continue with their day jobs.

What is more difficult is converting the security headlines into enough activity and fees for miners and BTC holders to care about more than the hashrate number.

(Tag translation) Bitcoin