Little-known capital controls could effectively lock banks out of Bitcoin, a group of Republican senators are warning US banking regulators, even as Congress moves to give traditional financial companies a bigger role in digital asset markets.

In a May 27 letter to Federal Reserve Vice Chair for Oversight Michelle Bowman, FDIC Chairman Travis Hill, and Comptroller of the Currency Jonathan Gould, six senators called on the agency to create a new capital framework for digital asset activity on its balance sheet.

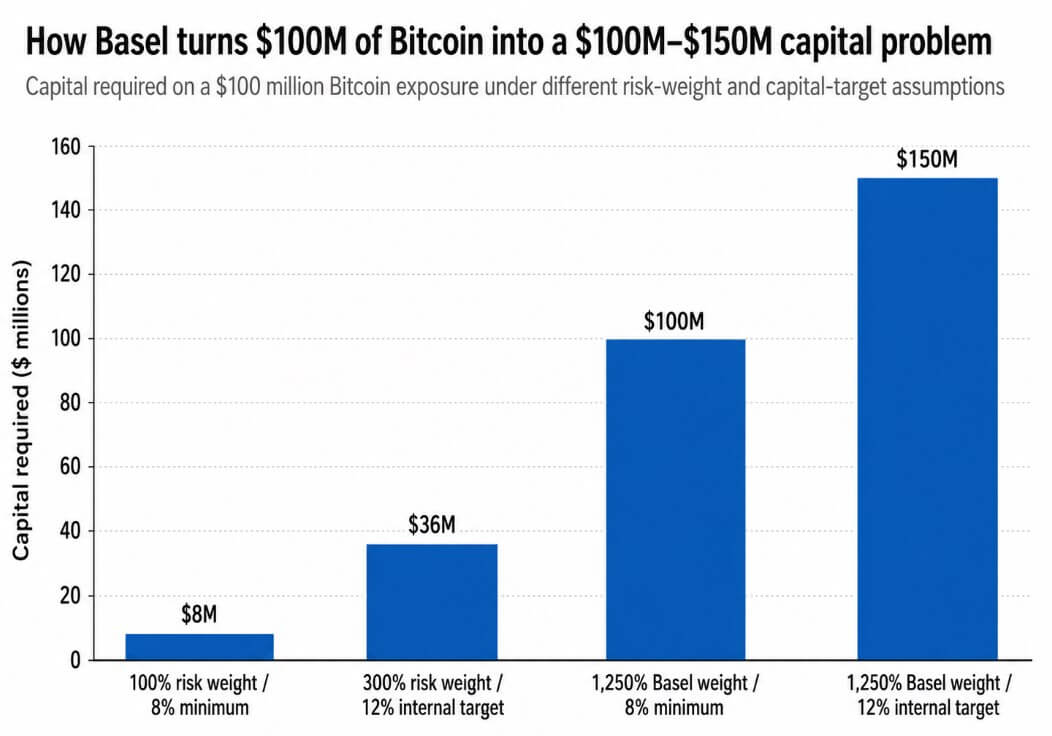

Their goal is Basel’s 1,250% risk weight for assets such as Bitcoin, which they argue will act as a de facto ban on banks holding cryptocurrencies.

A risk weight of 1,250% multiplied by a minimum capital requirement of 8% equals a 100% capital allocation. This means that a bank with $100 million in Bitcoin would need at least $100 million in capital against it.

For banks that manage to meet their internal CET1 targets above the regulatory floor, the burden increases further. A bank with a 12% internal capital target would need $150 million in capital for the same $100 million exposure, and would need about $18 million in annual net income to clear the 12% ROE hurdle.

Normal storage, trading, or customer service economics rarely result in profits at that threshold, and while banks are legally authorized to hold Bitcoin, they cannot economically justify it.

Why does this land now?

The Senate Banking Committee passed the CLARITY Act on a 15-9 vote on May 14, sending it to the Senate floor.

The bill, if passed, would give banks a clearer legal role in digital asset markets, but senators argue that legislative authorization without capital efficiency would leave banks with authorization votes they cannot afford to use. Even though banks are legally authorized to hold Bitcoin, they may be structurally prevented from doing so by capital charges that make the position uneconomical before the first transaction.

The three regulators addressed in this letter are each working toward liberalization of cryptocurrencies starting in early 2025.

In March 2025, the OCC reaffirmed that national banks can engage in virtual currency custody, stablecoin-related activities, and distributed ledger payment functions, while removing the prior supervisory non-challenge requirement.

The FDIC followed suit in the same month, rescinding notification requirements and allowing agencies under FDIC oversight to pursue permissible encryption activities without prior approval.

The Fed withdrew its guidance on crypto assets and dollar tokens in April 2025, positioning the move as a support for innovation.

All three institutions opened the door to cryptocurrency activity and left the issue of Bitcoin capital untouched.

Senators found the most poignant foothold in a March 2026 interagency FAQ on tokenized securities.

| regulator | Recent cryptocurrency-friendly movements | allowed or relaxed | What remains unresolved |

|---|---|---|---|

| O.C.C. | Guidance for March 2025 | Cryptocurrency, stablecoin activities, and DLT payments. Removed no-objection requirement | Capital processing of bank-held Bitcoin |

| F.D.I.C. | Guidance for March 2025 | Cryptographic Activities Permitted Without FDIC Prior Approval | Capital treatment for direct exposure to virtual currencies |

| FRB | Withdrawal in April 2025 | Get Previous Cryptocurrency/Dollar Token Guidance | Bitcoin capital treatment on balance sheet |

| FRB/FDIC/OCC | March 2026 FAQ | Tokenized securities are generally treated the same as the underlying securities | Does that logic apply to native crypto assets? |

Joint guidance from the Federal Reserve, FDIC, and OCC stated that eligible tokenized securities should generally receive capital treatment similar to non-tokenized securities, and capital allocation should not be determined by the technology used to record or transfer ownership.

If tokenized treasuries are treated similarly to treasuries because the underlying risk profile determines their treatment, that logic should be extended to Bitcoin as well, where the asset’s volatility and operational risk can be measured and support a coordinated framework.

The March 2026 guidance targets eligible tokenized securities, and the senators are calling on regulators to apply the same technology-neutral logic to native digital assets.

A sensible case for this rule

A 2023 joint statement from the Federal Reserve, FDIC, and OCC points to price volatility, legal uncertainty regarding custody and ownership, contagion from exchange and counterparty failures, governance weaknesses in crypto networks, and operational risks associated with open or decentralized infrastructure.

The Basel standards were built around these risks after the 2022 cryptocurrency collapse revealed how quickly losses could spread to interconnected institutions.

The per-dollar capital charge reflects a genuine judgment that Bitcoin’s risk profile is not similar to the assets that make up traditional bank balance sheets.

The senators argue that the risks of volatility, custodial complexity, and operational exposures are quantifiable and that a tailored capital framework can address them without requiring more capital than the exposure itself.

The Basel Committee agreed in November 2025 to expedite a targeted review of elements of the crypto asset standard and reported on the progress of that review in February 2026.

Basel Chairman Eric Tedine said global crypto rules for banks need to be reviewed after the US and UK refused to adopt the current framework.

A coalition of major financial industry organizations sent a letter to Basel in August 2025 calling for a moratorium and modification of the standard, saying it makes meaningful bank participation uneconomical.

Senators are calling on U.S. regulators to take action now that the international framework supporting the 1,250% treatment is under public scrutiny.

There are two paths from here

If regulators respond by proposing a tailored framework for liquid digital assets rather than a comprehensive Basel weight, the capital required for a $100 million Bitcoin exposure could fall from the current range of $100 million to $150 million to nearly $8 million to $36 million, under a 100% to 300% risk weight band and standard capital targets.

| scenario | treatment of capital | The role of banks in virtual currency | Possible market effects |

|---|---|---|---|

| tailored framework | Risk weight band from 100% to 300%. $8 million to $36 million capital for $100 million exposure | Banks can hold inventory and support market making, custody, prime brokerage, and structured products. | Improving institutional liquidity. The spread is narrow. Bank becomes a balance sheet participant |

| Basel rules remain | 1,250% risk weight. $100 million to $150 million in capital with $100 million exposure | Banks primarily provide storage, settlement, and services, but avoid direct exposure to BTC | Access to Bitcoin continues to be via ETFs, non-banks, and offshore venues |

At that level, bank market making, custody, prime brokerage, and structured crypto products become viable business areas. Institutional liquidity increases, spreads compress, and banks move from service providers to balance sheet participants.

If regulators continue to open up other channels while retaining the 1,250% treatment as the de facto standard for on-balance sheet exposure of native cryptocurrencies, direct exposure to Bitcoin will remain with non-banks and ETF wrappers while banks will continue to provide custody and settlement.

U.S.-traded Spot Bitcoin ETFs have already seen outflows of around $4.4 billion from May 15 to June 3, indicating that institutional access to Bitcoin is centered on bank balance sheets.

As long as capital rules remain intact, that path will deepen.

While Congress is actively working to develop market structure rules that will govern bank participation in digital assets over the next decade, this letter increases the political cost of inaction: Legal authorization to hold Bitcoin means little if the capital charge required to hold it makes the position uneconomic from day one on the balance sheet.

(Tag translation) Bitcoin