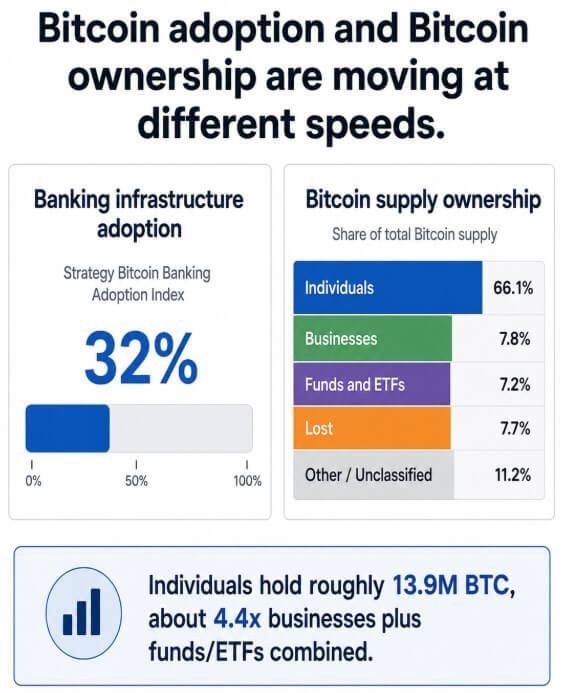

Strategy’s new Bitcoin Bank Adoption Index gives 25 largest banks and financial institutions an overall score of 32% based on activity across custody, trading, investment products, lending, and leadership support.

This number is a depth score that measures how well banks are building Bitcoin-related services across institutions tracked by the strategy.

Bitwise’s Q3 2026 Crypto Market Review estimates that 66.1% of Bitcoin’s maximum supply of 21 million (equivalent to approximately 13.9 million BTC) is held by individuals, dwarfing the 7.8% held by corporations and the 7.2% held by funds and ETFs.

The last two categories and companies, as well as funds and ETFs, together account for only about 15% of the supply, or about 3.15 million BTC worth. This means that individuals hold nearly 4.4 times as much Bitcoin as both groups combined.

Individuals first established the ownership base

Strategy’s index tracks the extent to which banks have built plumbing around Bitcoin, scoring institutions across their custodial systems, trading desks that execute orders, investment products, lending programs, and public statements that demonstrate an institution’s comfort with the asset.

Banks that score highly on this index have built the infrastructure to store, trade, lend, and package Bitcoin for their customers. Ownership of the coin itself is outside the scope of what the score attempts to measure.

The power of retail is here in the numbers, and it’s why banks are expanding in the first place.

Banks are responding to a combination of customer demand, ETF growth, corporate treasury activity, regulatory changes, and competition from crypto-native companies.

Customers already own and use Bitcoin on a scale that banks cannot ignore, and this 32% score reflects banks responding to demand created by individuals years before banks set up custodial desks.

A large ownership base allows banks to have an existing pool of owners with which to compete without having to create a market from scratch.

So the next contest will look different than most institutional adoption stories. Long before banks compete for coins that individuals might sell, they first compete with exchanges, specialized custodians, and account self-custody tools that individuals are already using.

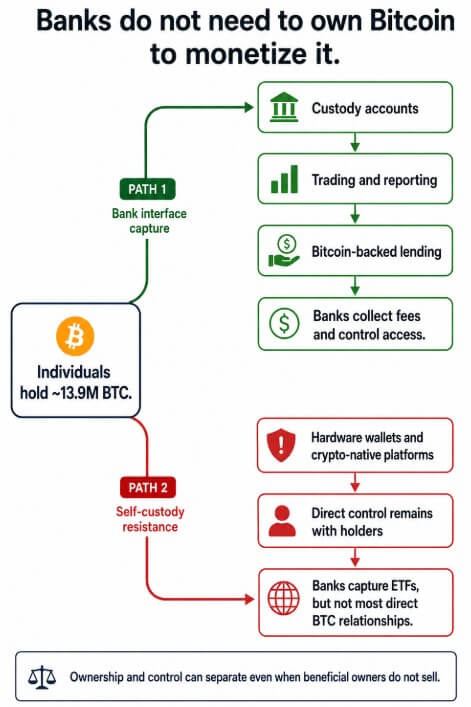

Ownership and control are becoming separated

Banks can store their customers’ Bitcoin, execute transactions, manage collateral, and charge fees for those services while the customer remains the beneficiary. A customer’s exact rights will vary depending on the custody, brokerage, or loan agreement, including the transfer or rehypothecation of assets.

This separates control of the customer interface from legal ownership of the asset. As more holders use brokered accounts, banks may have more influence over access, reporting and collateral terms, but this index does not prove that banks already have an advantage over exchanges or self-custody providers.

To put this into perspective, if 10% of the 13.9 million BTC belonging to an individual were transferred to a bank-managed custodial or securities account, approximately 1.39 million BTC would remain on the bank’s infrastructure. The remaining 90% will remain outside of these accounts, whether under self-management or held with other intermediaries.

At 25%, approximately 3.47 million BTC would be placed on bank-controlled rails. At 50%, this number would be closer to 6.94 million BTC. In each scenario, the customer’s ownership and withdrawal rights depend on the custody, brokerage, or lending agreement.

| Example of a personal BTC share moving to bank-managed rails | Affected BTC | What the bank benefits from | What an individual holds |

|---|---|---|---|

| 10% | ~1.39 million BTC | Custody fees, trade execution, reporting visibility, account relationships | Effective ownership of most coins |

| twenty five% | ~3.47 million BTC | A major foothold in Bitcoin storage, intermediation, and lending infrastructure | Ownership, but less direct control if held through an intermediary |

| 50% | ~6.94 million BTC | Plays a central role in Bitcoin storage and customer access, and has potential influence on the collateral market | Ownership of beneficial interests is subject to custody conditions, but access and enforcement of the account is transferred to the bank. |

what happens from here

The SEC’s SAB 122 rescinded SAB 121, which directed entities protecting the crypto assets of platform users to recognize liabilities and corresponding assets on their balance sheets. The changes remove accounting treatment that industry participants cited as a barrier to offering crypto custody at scale.

The Fed has lifted the requirement that state member banks provide advance notice before beginning crypto-asset activities, incorporating its oversight into its regular supervision.

The OCC said banks can buy and sell stored crypto assets at the direction of their customers as part of their permissible custody services. The Basel Committee Disclosure Framework on Banks’ Exposure to Cryptoassets will enter into force within the Basel Framework on January 1, 2026 and requires qualitative and quantitative disclosures by internationally active banks in member jurisdictions implementing the standard.

One possible path could be for Bitcoin-backed loans to become a more common asset management product, allowing banks to earn fees on collateralized loans without owning the underlying Bitcoin.

While holders can borrow against Bitcoin while maintaining price exposure, crypto-native lenders could face margin pressure if banks offer lower interest rates or broader account consolidation.

Resistance Pass keeps an individual’s Bitcoin holdings in self-custody and crypto-native platforms with no custody period suspension, withdrawal limits, fees, or counterparty risk.

Banks are still capturing customers who want ETF flows and regulated wrappers. Direct custody of individually held coins is out of reach, and an exchange built for Bitcoin from the beginning preserves the relationships banks are seeking.

Bitcoin’s institutionalization stage progresses in the order that most financial instruments follow. Individuals first built the foundation of ownership years before banks built the custodial, lending, and asset management systems that now compete for a piece of it.

Regardless of what percentage of that 13.9 million BTC ends up in bank-managed accounts, the coins already belong to the people the bank is trying to reach, and ownership arrived long before the invitations were sent.

(Tag Translation) Bitcoin