Bitcoin’s recent recovery has pushed the flagship digital asset back to the $75,000 level, continuing a wide range of returns across risk appetites as global stock prices hit new highs on hopes of calming the situation in the Middle East.

However, this movement faces constraints that are quieter than geopolitics or crypto-specific sentiment. Bond markets remain a sign that the Federal Reserve is in no hurry to ease policy.

That context is becoming more important as the battle for succession at the U.S. central bank enters a more volatile phase.

The Senate Banking Committee has scheduled a confirmation hearing for Kevin Warsh on April 21st, and Jerome Powell’s current term as chairman ends on May 15th.

Mr. Powell’s term as Fed director ends on January 31, 2028, and he said last month that if a replacement is not confirmed by the end of his term as chairman, he would serve as interim chairman until that time.

For crypto investors, that means it’s no longer just a question of whether Warsh will become chairman. It’s whether the market starts to believe that changes at the top will actually change the path of interest rates and liquidity.

The Fed’s March meeting pointed in the opposite direction. Officials kept their target range for the federal funds rate unchanged at 3.5% to 3.75%, saying inflation remains moderately high and reiterating that further adjustments would depend on future data, evolving outlooks and the balance of risks.

Bitcoin recovery reaches a quiet ceiling

Currently, one of the most important macro variables for Bitcoin is policy pricing on the front end of the interest rate market.

CME announced this week that March brought dramatic gains in the short-term interest rate market, with two-year Treasury yields fluctuating in a 50 basis point range, and FedWatch showing “no rate hikes by December” as traders’ base case for 2026. This is not the profile of a market that is betting on a clean, aggressive easing cycle.

This indicator is prescient because Bitcoin has spent much of this recovery trading like part of a broader global risk complex.

Hopes for a ceasefire, which helped bring oil prices down from recent highs and global stocks back to record highs, reignited hopes that inflationary pressures from the Iran war might ease, a shift that helped gold and other non-yielding assets recover.

Bitcoin has been a part of the movement, but it has not been able to escape the larger debate about how long America’s restrictive policies will remain in place.

The distinction is important. A formal interest rate cut is not necessary to deal with cryptocurrencies. We need to convince the market that financial conditions are easing.

At the moment, the idea is still partial. Investors are willing to buy risk as oil prices fall and war fears recede, but interest rate markets still reflect the Fed’s desire for more evidence before taking action. Therefore, any rebound in BTC will depend on macro price repricing, which has started cautiously.

Succession disputes affecting the market

Warsh’s nomination was supposed to give the market a clearer look at the post-Powell Fed. Instead, extradition became embroiled in legal and political risks.

Treasury Secretary Scott Bessent said this week that he remains optimistic that Mr. Warsh will become chairman in time, but Republican Sen. Thom Tillis vowed to block the nomination while the Justice Department’s investigation into Mr. Powell continues. Sen. Elizabeth Warren also urged the committee not to move forward under that cloud.

Rather than resolve that uncertainty, Mr. Powell reinforced it. At a press conference in March, he said he would remain the next chair if Warsh’s approval was not received by the end of his term, and that he would not leave the board until the investigation was concluded “with transparency and finality.”

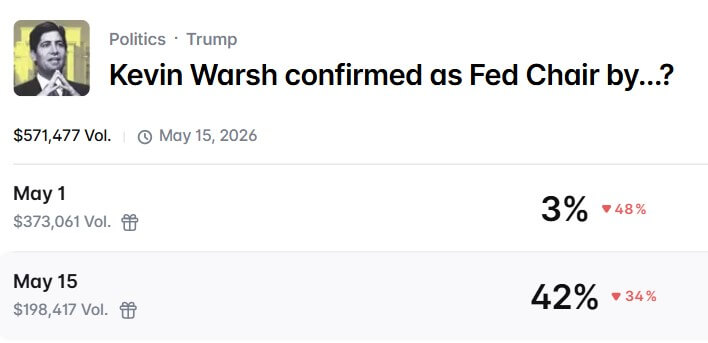

The uncertainty and impasse has caused Mr. Warsh’s odds on May 15 on prediction markets such as Polymarket to fall to 42% from a high of 80% earlier this year.

Meanwhile, President Donald Trump has since threatened to fire Powell if he remains in office beyond May 15, raising the risk of an institutional clash just as markets are trying to figure out the next policy regime.

As a result, the practical outcome for the market is continuity. Even if Mr. Warsh is ultimately confirmed, any delay would extend the life of the same cautious policy framework that has characterized the Fed this year.

The current lineup of the commission is still led by Powell, and the March vote itself had only one dissent, with Gov. Stephen Milan supporting the quarter-point cut, but the rest did not support the change.

This points to at least one visible division, although the committee still appears to be broadly aligned.

Price is only half the story

The reasons for restraint are clear from the data. According to the Labor Department, the unemployment rate was 4.3% in March, while core CPI rose 2.6% year-on-year.

New York Fed President William Williams said Thursday that wars in the Middle East are already adding to inflationary pressures through higher energy and transportation costs. St. Louis Fed President Albert Moussallem said the recent oil crisis will keep core inflation at around 3% for the rest of the year, and interest rates may remain unchanged for some time.

However, the federal funds rate is only part of the transmission mechanism for cryptocurrencies. A more serious issue is liquidity, which brings balance sheets back into focus.

According to Fed data published by FRED, the Fed’s total assets were approximately $6.69 trillion as of April 8.

More importantly, the March policy directive indicated that the central bank is still increasing its holdings in the system open market account through the purchase of Treasury bills and, if necessary, other Treasury securities with maturities of three years or less, in order to maintain adequate levels of reserves.

It also carries forward principal payments from Treasury stock holdings and reinvests agency principal in Treasury bills.

This plumbing is not the same as a full mitigation cycle, but it is important for a market built around a liquidity narrative.

Mr. Warsh is perceived as having a different personality, with a lower tolerance for the Fed’s huge balance sheet and more skepticism about bond-buying programs that stretch the Fed’s balance sheet.

In fact, Reuters reports that he criticized the Fed’s balance sheet management and pushed for tapering quantitative easing and shrinking its portfolio. This combination could be interpreted as being hawkish on liquidity in the short term, even if investors find it pro-growth in the long term.

What virtual currency traders are paying attention to now

The next clue appears quickly. Mr. Warsh’s April 21 hearing will reveal to the market whether senators see him as a full-fledged candidate to take over or as part of a broader fight over the Fed’s independence.

Investors will hear his views on three related issues: whether to consider supply-driven inflation from the Iran war, whether lower interest rates and shrinking balance sheets can coexist, and whether he will maintain the Fed’s cautious, data-dependent stance or attempt to redefine it.

Attention then returns to the calendar that actually drives asset prices. The next FOMC meeting is scheduled for April 28-29, according to the March meeting minutes.

Even if Mr. Warsh is not yet confirmed, Mr. Powell remains the face of policy, and the market is likely to read any statement in the same wait-and-see framework that it has been trading in all year.

Even if Warsh later succeeds, the criteria for a lasting crypto breakout will likely remain the same. Traders must begin to believe that front-end interest rates and reserve management are moving towards easing financial conditions, rather than simply preventing stress.

Therefore, quiet signals are more important than loud signals. Bitcoin could rise on ceasefire reports, ETF demand, and improving risk appetite, all three of which contributed to Bitcoin’s recovery.

But unless interest rate markets start pricing in the Fed’s easing path, or at least a more accommodative liquidity backdrop, the bull market will remain exposed to the ceiling that has held it back for much of this year.

For Bitcoin, the biggest drama is in Washington. The more important variables are still trading at the short end of the US curve.

(Tag Translation) Bitcoin