Bitcoin’s second-quarter decline unfolded in parallel with a rare contraction in the stablecoin market, adding another sign that liquidity in cryptocurrencies is weakening beyond just spot prices.

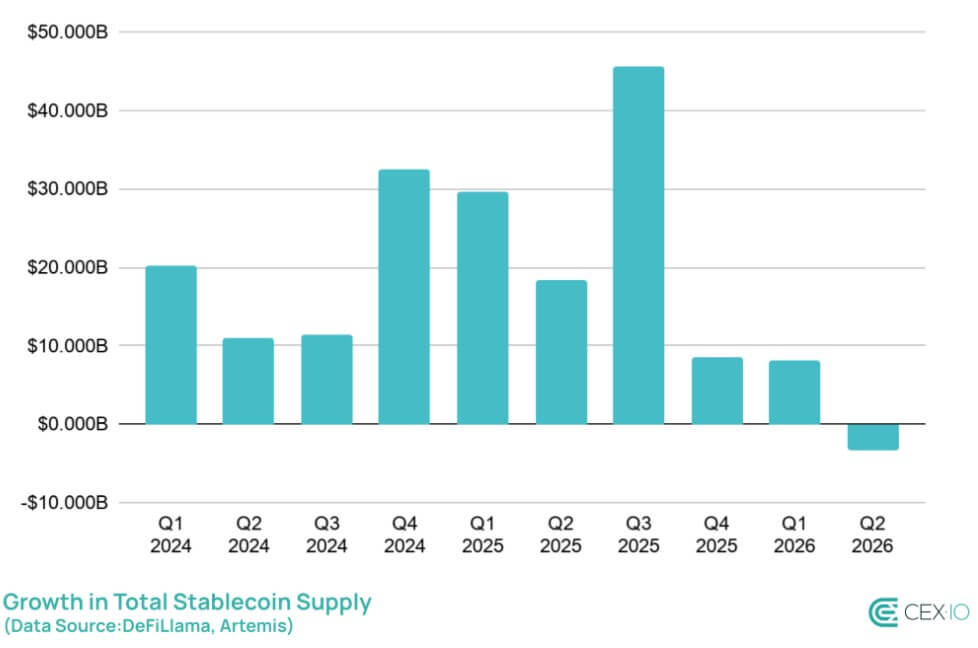

Bitcoin’s trading price fell below $60,000 during the quarter, its lowest level since 2024, and fell 14% over the second quarter. At the same time, the total stablecoin supply decreased to $312 billion, down more than $3 billion from the previous quarter, CEX.IO said in a report shared. crypto slate.

This decline marks the first quarterly decline in stablecoin supply since Q3 2023. Although the decline was small in percentage terms, it was caused by the broader crypto market losing 6.2% of its value.

This increased stablecoins’ share of total crypto market capitalization from 13% to 14%, showing that despite capital flowing out of the sector, investors still hold a large portion of the market in dollar-linked tokens.

Stablecoins are often treated as a cash layer for cryptocurrencies. Traders use them to move between exchanges, settle trades, park funds, and access decentralized finance.

Therefore, a decline in supply does not automatically mean users will abandon stablecoins, but it does indicate that fewer digital dollars are circulating in the market as trading, remittance, and speculative activity also weakens.

Products with high yields are a hindrance

The most rapid changes came from high-yielding stablecoins, which have been one of the strongest parts of the market since mid-2023.

After nearly three years of quarterly increases, the category fell by more than $3.5 billion, or 15%, in the second quarter. This decline reversed the 19% increase in the first quarter and demonstrated how quickly demand shifted away from crypto-native yield strategies as market conditions deteriorated.

Ethena’s sUSDe accounted for most of the decline. Market capitalization fell 52%, wiping out nearly $2 billion in market capitalization. Sky’s sUSDS also fell, dropping 16% during the quarter.

These two assets helped fuel the early growth of high-yield stablecoins, but became a source of pressure as users reduced their exposure.

Conversely, institutional investors’ focus on yield has shifted to products backed by real assets (RWA) and short-term U.S. government bonds. BlackRock’s BUIDL tokenized fund rose 2%, while alternative government bond-backed products such as USYC and USDY rose 16% and 66%, respectively.

This bifurcated performance signals a clear flight to the safety of the stablecoin market itself, with capital shifting away from algorithmic and synthetic DeFi mechanisms to traditional financial instruments with regulated yields.

Layer 2 network loses stablecoin balance

This shrinkage also manifested itself in the entire blockchain network, particularly in layer 2 of Ethereum.

The supply of stablecoins on the Ethereum scaling network fell by 24%, or $4.34 billion, in the second quarter. This was the sector’s largest quarterly decline since the fourth quarter of 2022.

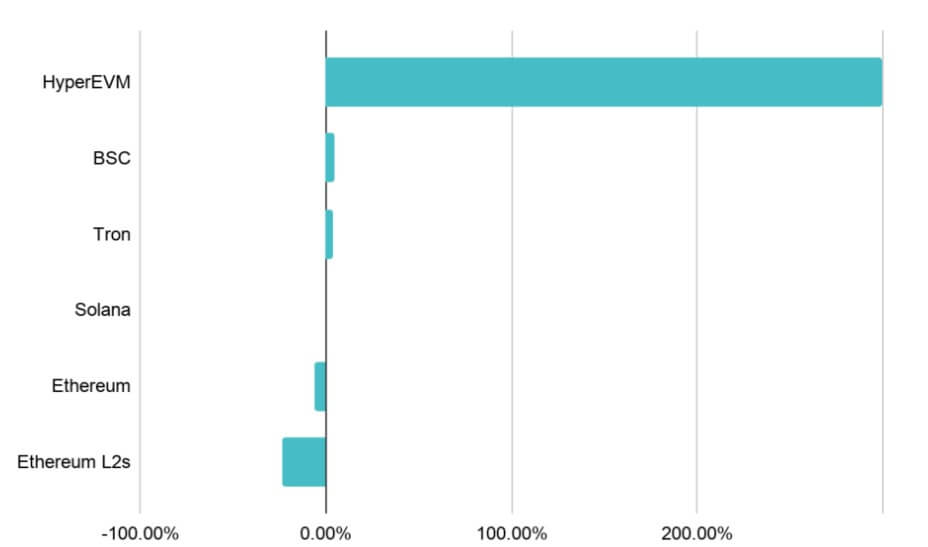

Arbitrum accounted for most of the decline. The company’s stablecoin supply decreased by 45%, losing $3.5 billion during the quarter. This network previously benefited from its role as the primary route to Hyperliquid.

HyperEVM’s own stablecoin supply increased by 300% to $5.6 billion, indicating that some liquidity moved away from Arbitrum rather than leaving the market entirely.

Ethereum’s base layer recorded an even bigger absolute decline, with more than $10 billion in stablecoin supply lost. According to CEX.IO, this was Ethereum’s steepest quarterly decline since Q1 2023.

Other networks moved in the opposite direction. Tron added $3.4 billion to the stablecoin supply, and BNB Chain gained $700 million.

The increase in these chains is primarily related to payment activities, indicating that stablecoins used for remittances and payments are more resilient than stablecoins associated with DeFi and transaction flows.

Network-level data shows that the market is not shrinking evenly. While some crypto-native liquidity channels weakened sharply, payment-focused chains continued to grow.

This difference could dictate how quickly the market stabilizes if trading activity remains subdued.

USDC expands share as transactions decline

Clearer confirmation of the overall slowdown appeared in network activity metrics, but USDC stood out as an exception.

CEX.io said total stablecoin trading volume decreased by 18% to $6.8 trillion. USDT trading volume decreased by 24%, reflecting a broader decline in crypto trading activity.

Meanwhile, USDC’s trading volume increased by 34%, making it the only major stablecoin to record an increase in absolute trading volume during the quarter. As a result, USDC’s share of the total virtual currency trading volume rose to 12.5%, a record high. The previous high was 11%, recorded in the fourth quarter of 2023.

This change partly reflects changes in centralized foreign exchange markets, particularly in Europe. Tether has not secured authorization under the European Union’s Market for Cryptoassets (MiCA) framework, and the exchange has reduced its USDT support at regulated facilities in Europe.

This creates more room for USDC to benefit from Circle’s compliance position in the region.

CEX.IO’s platform data showed a similar pattern. USDC accounted for 60% of stablecoin-related financial activity on exchanges in Q2, up from 58% in Q1 and 27% in Q1 2025.

This number shows that USDC is on the rise despite a cooling overall trading environment. This will give Circle’s tokens a stronger position in regulated exchange activity, while putting USDT’s dominance under further pressure in a market with increasingly stringent compliance requirements.

Migration shows widespread slowdown

Notably, the clearest sign of low activity in the stablecoin sector comes from transaction data.

The number of stablecoin transactions in the second quarter fell to 4.48 billion, down 530 million from the previous quarter. CEX.IO said this was the largest absolute quarterly decline ever. The 11% decline was also the largest percentage decline since Q4 2022.

Even after eliminating bots, automated non-economic activities, the slowdown was still noticeable. The adjusted number of transactions decreased to 613 million, down approximately 11 million from the first quarter.

The small decrease in adjusted activity suggests that most of the overall decrease is due to infrastructure-related and automated flows, rather than ordinary users alone.

Adjusted trading volume also decreased. Organic stablecoin remittances decreased by 5.5% to $4.09 trillion, ending 10 consecutive quarters of growth. The 18.3% increase in the first quarter was followed by a reversal, with a more pronounced decline in the second quarter.

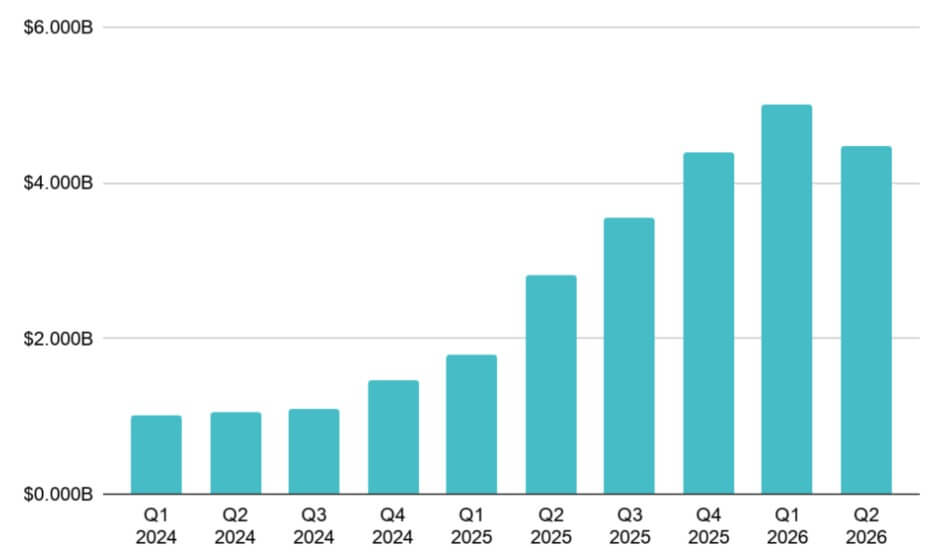

Still, smaller transfers were better tolerated. Remittances of less than $250 rose 5% to $19.39 billion. This increase suggests that retail-scale payments and peer-to-peer activity remained active even as large-scale remittances slowed.

The difference between small and large transfers is important for the second half of the year. If small-value payments continue to increase while high-value transactions and infrastructure flows decline, stablecoins could become less tied to crypto market cycles over time. However, if larger flows continue to decline, the market could face a longer liquidity reset.

Regulations respond to market downturn

The outlook for the second half of the year will depend in part on whether regulations bring in new demand fast enough to offset the slump in crypto-native activity.

In Europe, the MiCA transition period ended on July 1, forcing crypto-asset service providers to operate under the bloc’s licensing regime or cease services to EU customers.

This could continue to reshape stablecoin trading pairs, especially if exchanges move away from USDT to regulated alternatives.

In the United States, the GENIUS Act requires clearer provisioning, redemption, and oversight standards for stablecoin issuers. The CLARITY Act could add a broader market structure framework for digital assets, but its path remains tied to the Senate agenda and unresolved political battles.

Traditional financial companies are also getting deeper into stablecoins. By way of background, SoFi and MoneyGram have announced plans for a stablecoin, and Japan’s three largest banks are developing a joint yen-pegged token.

These efforts suggest that even though crypto-native demand weakened in the second quarter, institutional investor interest remains.

The question is whether new payments, banking and real-world asset use cases can offset the pressure from lower trading activity.

During the 2022-2023 recession, it took about a year for stablecoin supply to return to sustained growth.

However, the current cycle may not align with that timing, as the market is more diverse than it was three years ago.

(Tag translation) Bitcoin