March and April 2026 drawdowns will have structural implications as Bitcoin ETF holders remain stable.

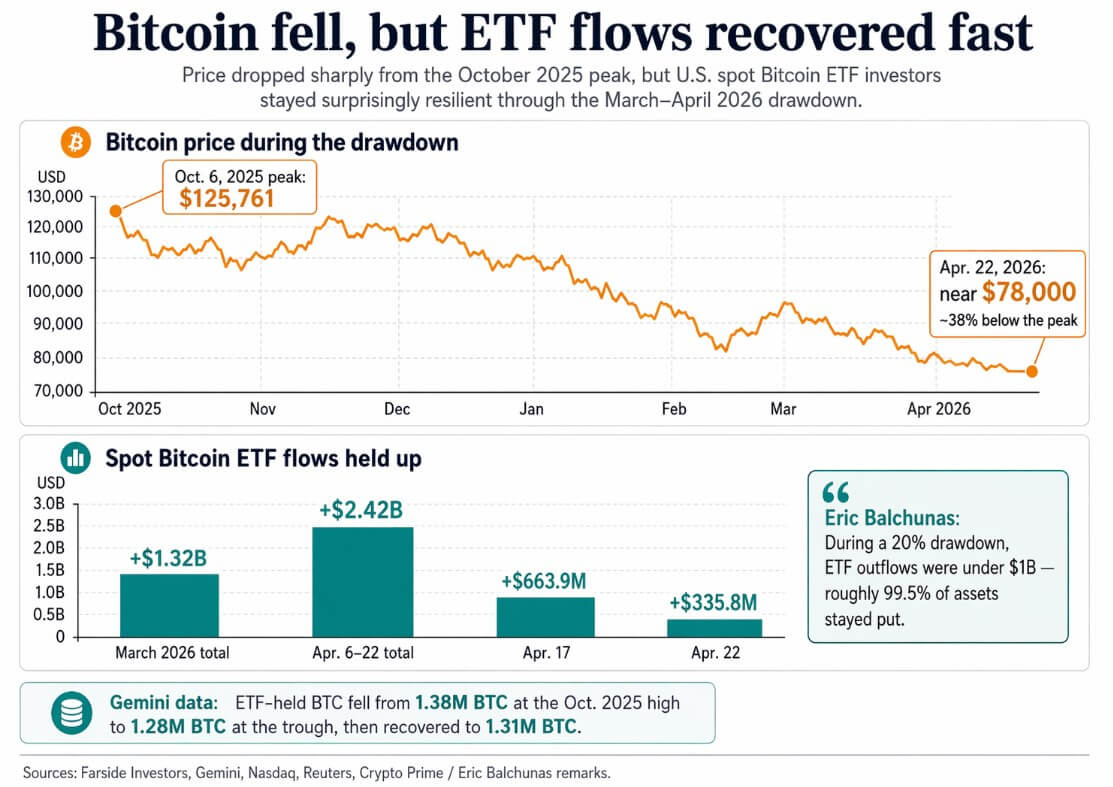

Bitcoin is hovering around $78,000, about 38% below its Oct. 6 peak of $125,761, and the U.S. Spot Bitcoin ETF saw inflows of $1.32 billion in March, reversing four consecutive months of outflows. The ETF then added an additional $2.42 billion in net inflows from April 6 to April 22.

The best days were April 17th with $663.9 million in inflows and April 22nd with $335.8 million inflows. According to Gemini’s coin-level data, the ETF’s Bitcoin holdings only fell from a high of 1.38 million BTC in October 2025 to a low of 1.28 million BTC, before quickly recovering to 1.31 million BTC.

Eric Balchunas, senior ETF analyst at Bloomberg, said in an interview with Crypto Prime that during the 20% drawdown, the ETF recorded outflows of less than $1 billion, or about 99.5% of its assets. This happened during a truly hostile macro window.

According to Nasdaq’s March update, digital asset market capitalization fell by 21% in the first quarter, with the Nasdaq 100 down 4.9% and the S&P 500 down 5.1%. ETF holders soaked it all up without creating the wave of exits that skeptics had predicted.

Balciunas argued that the selling pressure is coming from long-term crypto holders, saying the voice is “coming from within.”

ETF analysts’ interpretations are consistent with the flow data: While the ETF remained net-buying despite its historically sharp drawdown, other factors pushed prices down.

different types of buyers

The ETF wrapper places Bitcoin within a model portfolio, advisor guardrails, committee-approved position limits, and rebalancing schedules.

Buyers in these buildings operate during normal trading hours and are therefore constrained by regulations. In drawdown, constraints look like discipline.

| Buyer type | typical rapper | behavioral constraints | Behavior that may result in drawdown |

|---|---|---|---|

| Spot Bitcoin ETF holders | ETF/Security account | Model portfolios, advisor rules, position limits, trading hours, rebalancing schedules | Likely to hold or rebalance gradually |

| Traditional Crypto Native Holders | Direct ownership of coins | Fewer formal portfolio guardrails | Increase in discretionary sales |

| leverage trader | Permanent/margin venue | Liquidation risk, collateral pressure | Forced sales may accelerate |

| Legal entity/financial holder | Balance sheet allocation | Financial policy, liquidity needs | Possibility of divestiture based on company-level constraints |

| miner | Native BTC holdings | Operating costs, financial needs | Selling may occur in search of liquidity |

Bitwise and VettaFi’s 2026 Advisor Survey found that 32% of financial advisors had an allocation to cryptocurrencies in their client accounts in 2025, up from 22% the previous year, 42% said they were able to purchase cryptocurrencies in their client accounts, and 77% cited ETFs as their preferred vehicle.

EY-Parthenon and Coinbase’s 2026 Institutional Survey found that 73% of respondents plan to increase their digital asset allocation this year, 66% already access spot crypto through an ETF or ETP, and 81% prefer registered vehicles to direct storage of their coins.

The framework for EY’s behavioral findings is that volatility is driving more formal risk discipline.

BlackRock strengthened its sizing logic in late 2024, recommending a maximum allocation of 2% for investors interested in Bitcoin, noting that larger weights can disproportionately change overall portfolio risk.

A 2% sleeve absorbs a 38% drawdown of assets, an acceptable resistance for a diversified portfolio. This will result in a slower hand.

On January 5, 2026, the distribution infrastructure continues to deepen, with Bank of America publishing recommendations for crypto ETPs to advisors across Merrill, Merrill Edge, and its private banks.

Morgan Stanley filed for a Bitcoin ETF in January, launched MSBT on April 8, and Charles Schwab announced spot crypto trading.

Each move directs more Bitcoin purchases through channels where compliance reviews, position sizing rules, and customer agreement constraints control execution. Discretionary panic selling is more difficult to execute in these channels.

Different cases of this behavior

In the bulls’ case, the ownership base has already started to change and will become more complex over time.

As access by advisors and institutional investors expands, marginal buyers of Bitcoin have started holding small, long-term allocations based on rebalancing rules.

At the next drawdown, we see that buyers are less likely to withdraw and more likely to add. The preference for registered vehicles in both advisor and institutional surveys, the modest contraction in ETF holdings during a severe drawdown, and the speed of flow recovery in April are all pointing in the same direction.

Citi’s 12-month bullish scenario for Bitcoin targets $165,000, supported by sustained institutional demand and a constructive regulatory backdrop in the US.

The bearish case pinpoints the limits of that argument in a situation where the recent drawdown was never reached. ETF holders may prove to be disciplined only up to a threshold as stop losses are triggered, margin calls hit model portfolios, and allocation bands force reductions.

In that scenario, the same rules that created restraint during the decline would cause the sell-off to accelerate rapidly. Citi’s unfavorable 12-month scenario puts the price of Bitcoin at $58,000, a floor clearly tied to stalled U.S. regulatory progress, depleting a major ETF demand catalyst.

The bear case is also done through redistribution. A more disciplined set of ETF buyers may simply push Bitcoin volatility onto different actors, such as leveraged traders, perpetual futures markets, miners, and corporate treasury holders, who operate without guardrail rebalancing.

According to this reading, the recent resilience of ETFs reflects a benign macro window.

| scenario | What happens to ETF holders? | What happens to other holders? | Market impact |

|---|---|---|---|

| bull case | Stay steady, rebalance, and maybe add more | Increased selling by leveraged traders, miners, and legacy holders | The composition of ownership is structurally changing. Drawdown is more relaxed |

| basic case | Outflow is moderate, but there is no sudden increase. | Mixed selling pressure among crypto-native cohorts | ETFs cushion volatility on the margin, but do not rewrite market behavior |

| bear case | Allocation bands, stop losses, or macro stress cause increased ETF selling | Broad spread of risk-off selling across all cohorts | ETF resilience proves to be conditional, not structural |

| Key metrics to watch | ETF holdings BTC and net flows during the next 20%-30% decline | Relative selling strength other than ETFs | The best real-world test of Balchunas’ paper |

The next 20% to 30% drawdown will be a test to see if the ETF’s BTC holdings contract rapidly, or if flows quickly stabilize like they did in April. If recent patterns repeat, Balciunas’ interpretation will move closer to documented market facts.

A large-scale exit from the ETF under sufficient macro stress would confirm that the composition is maintained as long as conditions allow.

(Tag translation) Bitcoin