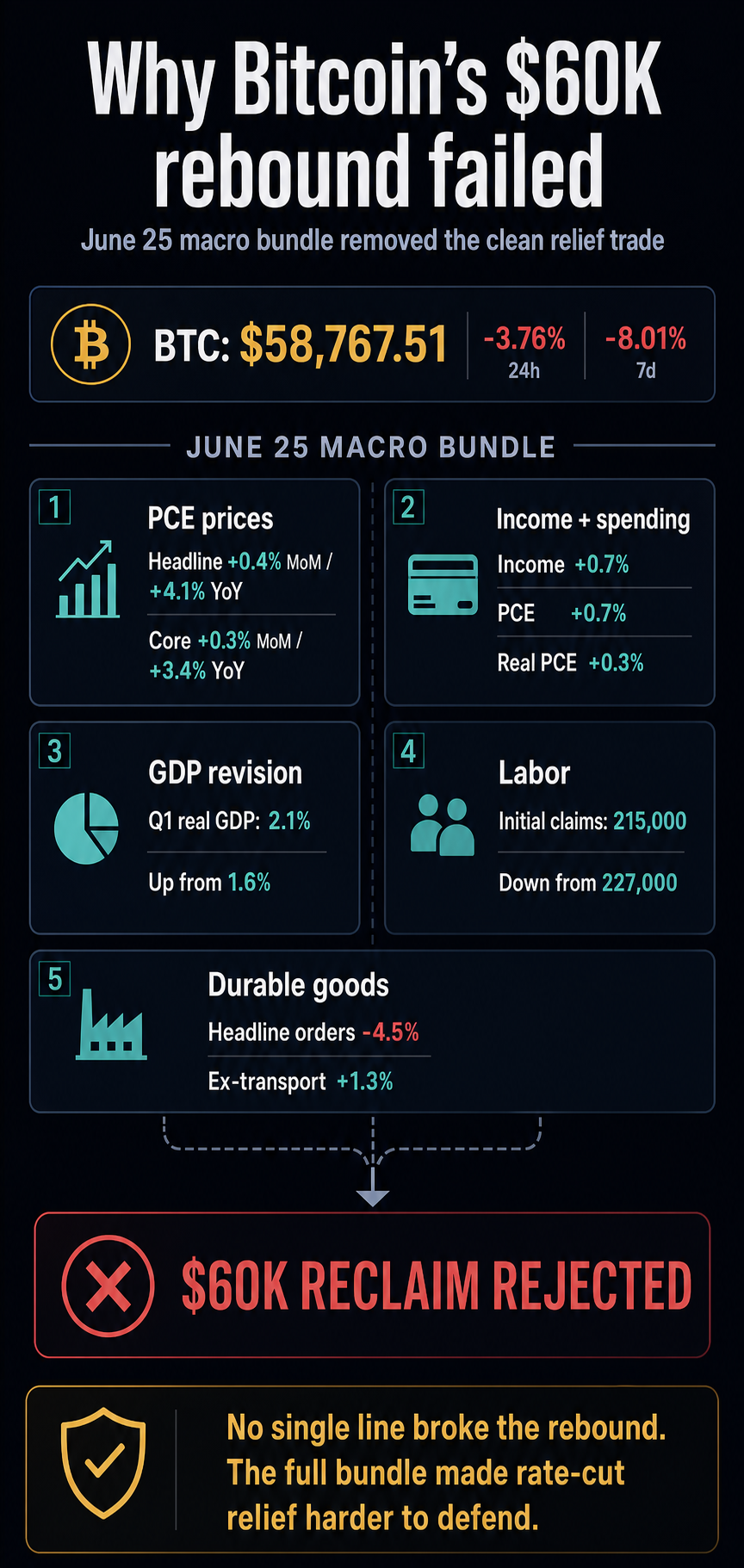

Bitcoin’s rally above $60,000 failed as a series of US macro statistics released on June 25 gave risk traders the opposite of a clean relief: sticky inflation, resilient demand, stronger growth corrections, lower unemployment claims, and resilient transportation orders.

Bitcoin briefly flash-crashed on a liquidation-driven flush, falling from an intraday high of around $61,844 to a low of around $58,189, before recovering some of its price action and trading around $59,630. This rebound has moved BTC off its intraday lows at the time of writing, but the price is still below its pre-crash range.

This move coincided with a highly unilateral liquidation event. According to CoinGlass’ liquidation results, the amount of virtual currency liquidation in one hour was about $482 million, of which about $427 million was long and only about $54 million was short, of which BTC accounted for about $272 million.

Stocks also moved sharply, but partially retreated. SPY fell from the low $730s to the $728-$730 area before rebounding to $737 on the latest 30-minute candlestick. This candle showed an open price of $735, a high price of $737, a low price of $734, and a close price of $737, while the chart label indicated that SPY was down about 1.30%.

DXY rose toward the 101.8 area before reversing and falling, dropping to 101.376 in the latest print. The yield on the US 10-year Treasury note also fell significantly, moving from the high 4.4% range to around 4.374%, and the interest rate after the temporary fluctuation remained near the lower end of the indicated range.

This move moved Bitcoin closer to the $58,000 area than the recovered upward range, turning $60,000 from a recovery target to a line where buyers still have to prove it.

This rejection was more than a chart-level failure. The release came after Bitcoin had already fallen below $60,000, subsequently negating traders to any soft data narrative that could help the risky asset recover.

The June 25 release showed weak headlines softened by persistent price pressures, higher incomes and spending, a more robust downward revision to growth, lower unemployment claims, and solid transportation sector data.

Data hurts relief trade

The most direct pressure came from the release of personal income and expenditures in May. BEA announced that personal income increased by 0.7%, personal disposable income increased by 0.7%, PCE increased by 0.7%, and real PCE increased by 0.3%.

Prices also remained elevated. The composite PCE price index increased by 0.4% month-on-month and 4.1% year-on-year, and core PCE increased by 0.3% month-on-month and 3.4% year-on-year.

This combination put the market in a difficult situation. Although spending and revenues were still expanding, inflation had not cooled enough to make it easier to factor in rapid policy easing.

For Bitcoin, this meant the rebound was battling the same macro headwinds that often hit long-term, high-beta assets first.

Growth data reinforced that message. BEA’s third estimate of first-quarter GDP has revised the real growth rate to an annualized pace of 2.1% from 1.6% in the second estimate.

Stronger growth corrections in tandem with persistent inflation typically make immediate interest rate easing less likely.

Labor statistics added a new element. The number of new unemployment insurance claims for the week ending June 20 was 215,000, down from the previous week’s revised figure of 227,000, according to the Labor Department’s weekly claims report.

The slowdown in the labor market did not result in a rebound in risk assets as insurance claims fell.

Durable goods were more mixed, but the details still tilted towards a facile dovish interpretation. Orders fell 4.5% in May, led by transportation equipment, according to the Census Bureau’s Advance Durable Goods Report.

Orders excluding transportation rose 1.3%, with underlying signals showing more resilience than the overall decline would suggest.

| data points | latest reading | Reasons for pressure on risk assets |

|---|---|---|

| May PCE price | Headline is +0.4% for the month, +4.1% for the year. Core Monthly +0.3%, Annually +3.4% | Inflation was too viscous for a clean relief trade |

| income and expenses | Personal income +0.7%. PCE +0.7%;Actual PCE +0.3% | Demand was not clearly slowing down and appeared to be strong. |

| 1st quarter real GDP | Revised annual rate from +1.6% to +2.1% | Growth rate looks stronger than expected |

| Unemployment insurance claims and durable goods | The number of claims decreased to 215,000. Orders for durable goods for transportation increased by 1.3% | Details of labor orders limited discussion of economic slowdown |

Bitcoin is now in high beta expression

The market reaction required a smaller catalyst than a uniform downside surprise would. This comprehensive policy only weakened the idea that US statistics had softened enough to lower policy expectations.

That’s why the nearly $60,000 failed recovery is different from the standalone support test. Bitcoin was already vulnerable after its recent selloff, and the macro release arrived at a moment when buyers needed a reason to defend against the rebound.

The data showed that the economy still has enough demand and labor to keep inflationary pressures in place.

firememecoins’s Bitcoin data showed how far the asset had already moved. BTC fell 8.01% in 7 days with a 24-hour trading volume of $48 billion, indicating active trading around the break.

The $60,000 level was both a test of confidence and a rough number.

The market also entered the release having already taken into account the stress points specific to other cryptocurrencies. A recent report from firememecoins mapped liquidation risk near $57,300, ETF flow pressure near $58,000, and the potential for Bitcoin’s PCE reaction to collide with quarterly option expiration.

These factors could strengthen the move once prices start to fall, but the macro release was a widespread reason for the rebound to lose support.

Bitcoin’s next challenge to $60,000 appears to be tied to broader liquidity conditions, not just crypto-native buy-in.

Once risk assets stabilize after absorbing the June 25th release, BTC can treat the data shock as another failed push and attempt to rebuild beyond the recovery line.

To do so, markets will need to stop treating strong activity data and persistent inflation as new reasons to maintain pressure on high-beta assets.

If dollar and interest rate sensitive parts of the market continue to weigh on risks, the $58,000 area remains at risk. That would keep liquidation zones and ETF flow pressures in place as accelerators, especially if option expirations are close enough to impact positioning.

The next signal is bigger than the crypto-native push buy. Bitcoin needs a macro backdrop to stop fighting the rebound before buyers return to $60,000 support.

(Tag translation) Bitcoin