With Bitcoin currently trading at just over $60,000, and the network’s estimated total cost to produce one coin being close to $84,300, the difference between the two is roughly a quarter, meaning that much of the network is mining on a total cost basis behind the scenes.

For years, the assumption was that this could never happen, that production costs would set a price floor, and that before the price of Bitcoin fell far below the cost of producing the coin, Bitcoin miners would switch off and the market would catch up. Still, prices have been below that line for several weeks and the network is still operating normally.

The collapse in mid-June is a good example of how corrections work in practice. Difficulty decreased by 10.09%, from 138.96 trillion to 124.93 trillion. Galaxy Research marked this as the second-largest downward revision of 2026 and the 11th-largest downward revision in the network’s entire history.

That epoch ran 15.6 days against a 14-day goal because so many high-cost machines fail when they run out of margin. The protocol realized that blocks were slow and lowered the standards for everyone still doing the hashing. So the self-correcting mechanism that people like to call it is real and actually works. But not in the way floor discussions tend to assume.

It was never the floor

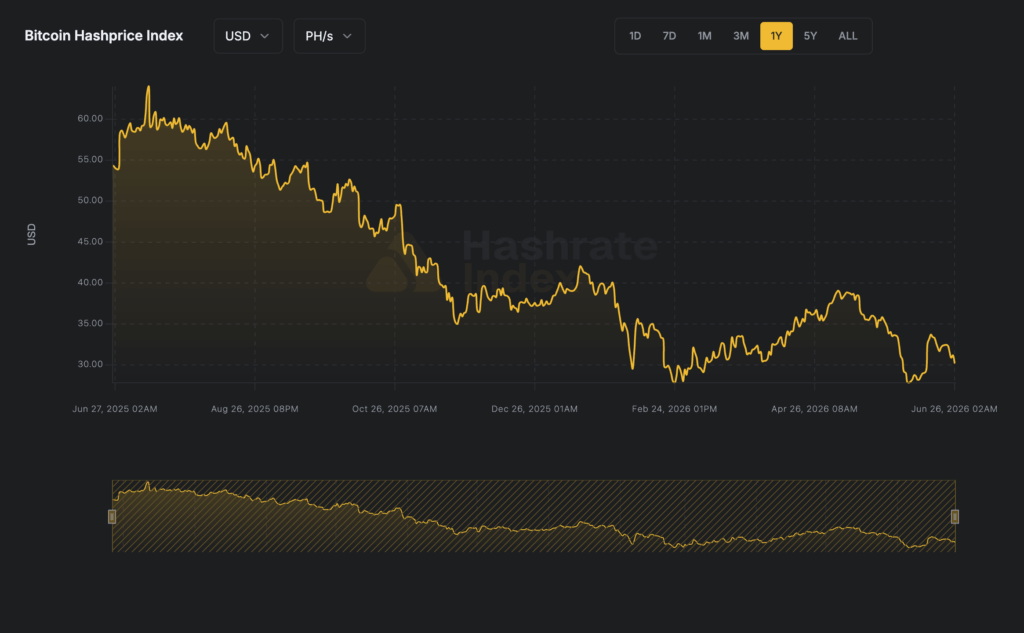

All of this comes down to the hash price, or the daily revenue that a Bitcoin miner earns per unit of computing power. If hash price falls $BTC Fees will increase if the price declines, network difficulty increases, or transaction fees decrease. $BTC In the event of a rally, rising fees, or weak enough miners left behind, the survivors will be reset to a lower difficulty level.

To put this into context, hash prices reached nearly $63 per petahash per day in July 2025, before sinking into the low $20s by early June. This is the level that the hashrate index and most operators treat as a total break-even point before debt and overhead, and has since rebounded above $30 following the June difficulty reduction.

In its Q1 2026 Mining Report, CoinShares puts the weighted average cash cost of producing one Bitcoin among public miners in Q4 2025 at approximately $79,995, with hash prices falling from a range of $36 to $38 towards $29. It is estimated that 15% to 20% of the world’s ships will be submerged if the cost of electricity becomes high enough.

However, what these average values hide is the large variation between operators, which is the entire reason why production costs cannot serve as a floor. Bitcoin miners running the latest generation hardware with less than 15 joules per terahash on less than 5 cents of power maintain healthy margins in the same market where older fleets paying 6 to 7 cents are hemorrhaging cash every time they find a block.

As the price of Bitcoin falls, the revenue per unit of hash falls at the same time, and the most costly machines start to become uneconomical, at which point operators start doing the obvious thing: selling. $BTCshut down rigs, delay expansion, renegotiate power contracts, or raise new capital to get through it.

Once enough hashrate leaves the network, the difficulty adjustment is lowered and miners who stay online are able to collect a larger share of the same block subsidy, thus relieving pressure, but that achievement is slow and uneven, and it doesn’t stop the price from falling while everything slips by.

Therefore, production costs ultimately determine who can continue production during a Bitcoin slide, but they do not determine where the actual slide stops.

The best Bitcoin miners survive by not being like miners.

During previous economic downturns, stressed miners really had only two options. Either keep the hash or turn it off. But the largest utility now has a third option: to transform the company into an AI and high-performance computing business.

CoinShares estimates that the cumulative value of AI and HPC contracts announced across the public sector currently exceeds $70 billion, and publicly traded miners could derive up to 70% of their revenue from AI by the end of 2026, up from nearly 30% currently.

The size of individual deals is similar, with Core Scientific’s expansion deal with CoreWeave alone reaching $10.2 billion over 12 years, TeraWulf posting $12.8 billion in contracted HPC revenue, Hut 8 signing a 15-year, $7 billion lease for its AI infrastructure, while Bitfarms went so far as to drop Bitcoin from its name entirely.

This divides the sector into three factions. A small number of miners have signed AI contracts and have already transferred production capacity and financed the transition with debt. The best example is Cipher. The company’s $1.7 billion in senior secured notes resulted in single-quarter interest expense of $33.4 million.

The second group is working on frameworks and early pilots that have not yet led to revenue, and the third group is still almost entirely tied to Bitcoin and thus exposed to Hashprice’s every move.

This difference is starting to show up in how the market values these companies. This is because hybrid infrastructure names are traded partially based on contract delivery and execution risk, while pure miners are traded as a cleaner bet. $BTCDifficulty, Financial Policy. And low-cost, niche carriers sit apart from all of that, being small and flexible enough to benefit when the hardships reset and cheap power is released.

Public Bitcoin miner reduced holdings by more than 15,000 $BTC Core Scientific released about 1,900 coins in January and plans to dispose of most of its remaining coins, Bitdia reduced its balance to zero in February, and Riot sold 1,818 coins in December.

put At this rate, in the first quarter of 2026 alone, public miners’ emissions increased even more. $BTC The pace of treasury liquidation is more than it did in all of 2025. Even the dumping seen in the market during the collapse of Terra Luna.

If Bitcoin recovers towards $100,000, the hash price will fall towards $37, Treasury sales will slow and the hardware refresh cycle will restart.

If it levels off around production costs, the sector will become exhausted as public miners sell coins and chase AI trades while hardship does some of the repair work.

And if it drops further, high-cost hashrates will continue to go offline, the capital gap between hybrid names and pure play names will widen, and the carriers sitting on the cheapest power will gain share.

Importantly, none of these paths breaks the network, which is the part where bear markets tend to be oversold. We can already see this in the partial reversal of the mid-June decline, with block times returning to near 10 minutes, and the return of some of the reduced capacity as prices stabilize. All of this suggests that the remaining hashrate was reacting to thin margins rather than abandoning the network.

Of course, the transition to AI comes with risks to network security, and the AI cooling cycle could hit hybrids before Bitcoin itself is mitigated, so the best signals to watch going forward are hash prices, the pace of difficulty adjustments, public miner treasury balances, and the coins miners send to exchanges.

What survives all this is what the House of Commons argument continues to get wrong. That means Bitcoin can be traded for far less than it costs the average Bitcoin miner to produce the coins. It’s likely to stay there for a while as production costs screen out producers. It could never support the price.

And the longer the longer $BTC The lower spending falls below that level, the more sharply the network becomes fragmented, separating operators with cheap power, modern machinery, and reliable second businesses from those who simply have no way to wait.