The old Bitcoin strategy ran on the simple logic that as global M2 expands, capital flows into risky assets and Bitcoin gains a disproportionate share.

This relationship was the driving force behind the 2020-2021 bull market, with crypto Twitter spending much of 2024 charting the M2 overlay as evidence that the next leg was imminent.

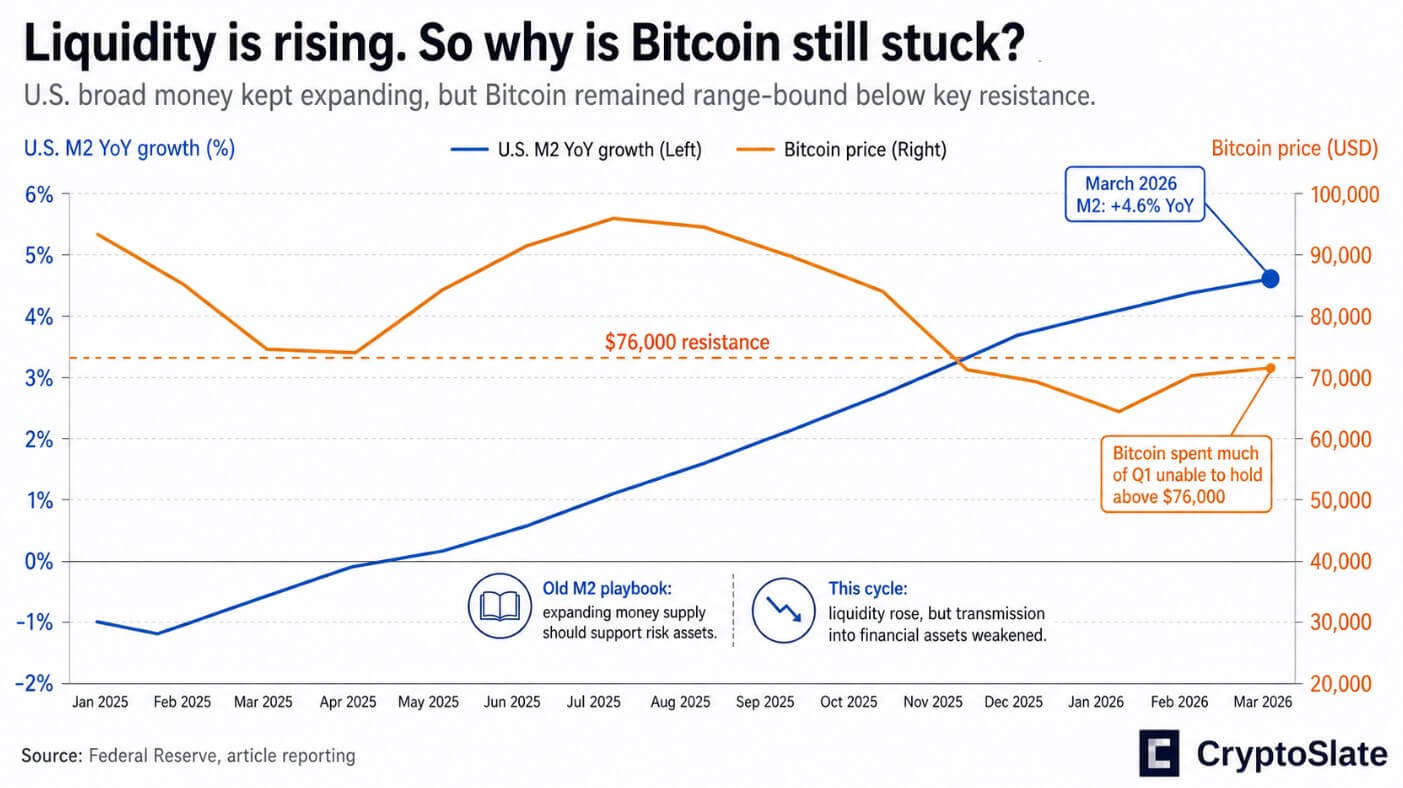

Currently, global M2 is expanding, but Bitcoin continues to underperform.

U.S. M2 issuance in March 2026 was approximately $22.7 trillion, up 4.6% year-on-year, and Bitcoin spent much of the first quarter failing to break above $76,000, a level that RealVision chief crypto analyst Jamie Coutts identified as a key resistance on CryptoQuant’s Unbiased podcast.

Coutts’ diagnosis was that the transmission mechanism had changed, as the type of liquidity determined whether the expansion actually reached financial assets.

Since Quantitative Easing in 2008, the Federal Reserve has purchased assets directly, flooding the system with bank reserves that have nowhere to go but stocks, credit, and eventually cryptocurrencies.

Treasury issuance, reserve management, cash balance fluctuations, and bank credit creation have now replaced the fire hose of central bank balance sheets.

plumbing problems

U.S. public debt ended the fourth quarter of 2025 at more than $38.5 trillion, up 6.3% from the same period last year. Meanwhile, US M2 grew by 4.6% over the same period.

Based on the most basic numbers available, debt outpaces common money by almost 2 percentage points each year. The outstanding debt is currently equivalent to approximately 1.70 times the total amount of M2, an unprecedented ratio in today’s accommodative financial environment.

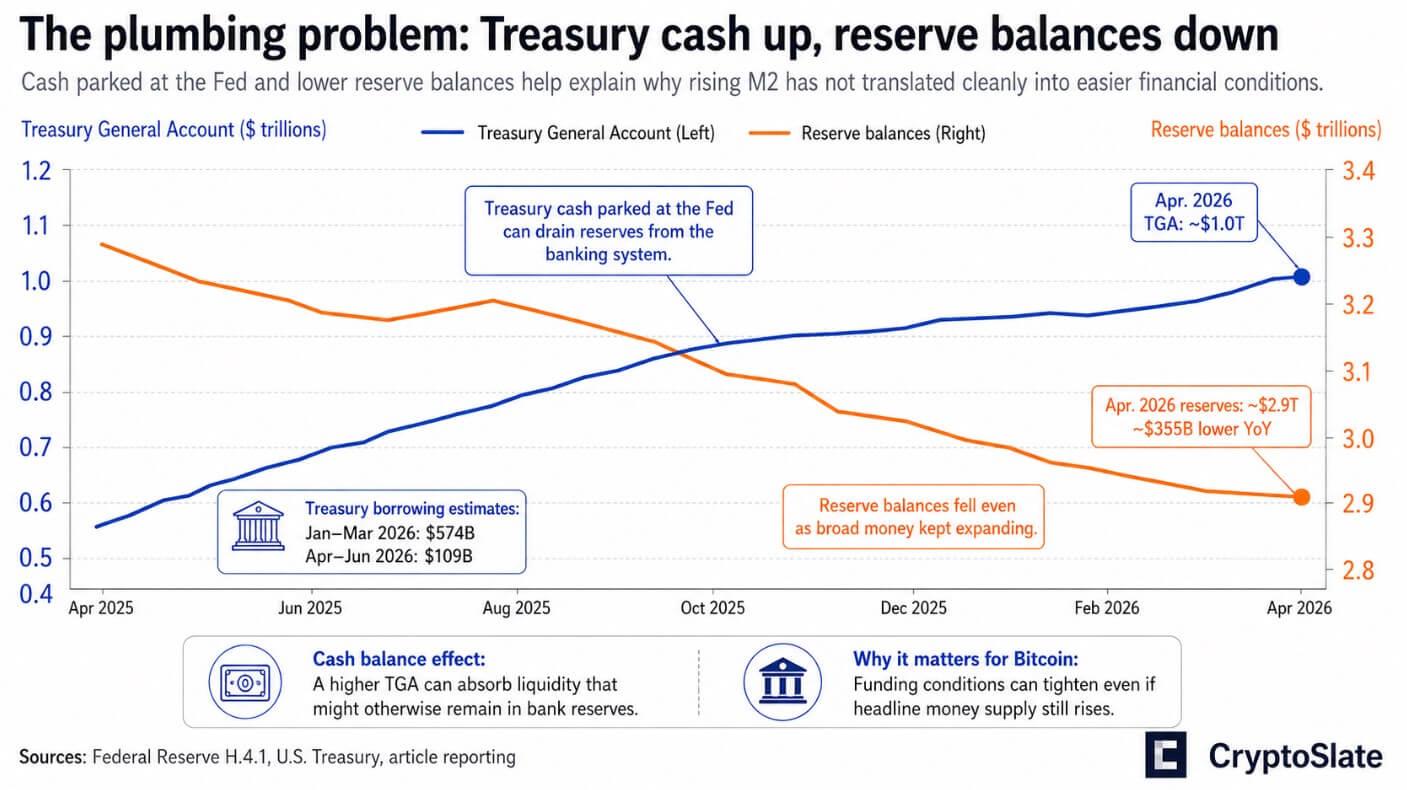

According to the Ministry of Finance’s own borrowing estimates, net marketable debt will rise to $574 billion in the January-March period of 2026, and an additional $109 billion in the April-June period, with the cash balance exceeding $1 trillion.

The Treasury Department’s General Account, part of the Federal Reserve Board, has approximately $1 trillion of up-to-date H.4.1 data. Even as M2 continues to rise, cash held at the Fed drains reserves from the banking system.

The Fed announced on April 22 that its reserve balance had fallen to about $2.9 trillion, a decrease of about $355 billion from the same period last year.

While broad money is expanding on paper, the lines that actually move reserves into financial markets are straining at the last minute.

Bank credit is still expanding, with commercial loans and leases reaching about $13.7 trillion by mid-April, but it appears to be being absorbed into the real economy.

At the FOMC meeting on April 29, the policy interest rate remained unchanged at 3.5% to 3.75%, and total assets remained at approximately $6.7 trillion. Officials cite inflation as the main restraint, and expanding the balance sheet is not on the agenda.

Why the old chart broke

In his podcast, Coutts argued that Bitcoin’s weakness reflects friction in the plumbing.

The decline in late 2024 and early 2025 was triggered by tightening of reserve requirements in the fourth quarter, Treasury actions related to the government shutdown, derivative-led deleveraging, and the growing role of ETFs and derivatives markets in Bitcoin’s price structure.

None of these forces appear in the global M2 overlay because they are characteristics of the financial system, where Treasury supply, reserve management, and funding conditions are the real battlegrounds.

Gold provides the clearest confirmation between markets. According to the World Gold Council, central banks purchased 244 tonnes of gold in the first quarter, an increase of 3% year-on-year, bringing total demand for gold to 1,231 tonnes and a record $193 billion in value terms.

Public institutions are hedging the credit of government bonds on a large scale, and they are doing so through gold, an asset that central banks can legally hold.

The IMF’s latest fiscal monitor reveals that global public debt is on track to reach 100% of GDP by 2029, with the US and China driving much of the acceleration.

The Congressional Budget Office projects that the federal deficit will be $1.9 trillion in 2026, and public debt will grow from 101% to 120% of GDP by 2036, creating a structural oversupply that will continue to compete with risk appetite for the same pool of reserves and capital.

2 results

In the bullish case, inflation cools toward the path the Fed expects, Treasury cash balances decline, reserves are rebuilt, and bank credit continues to expand without fear of growth.

In this situation, the theory that “liquidity is still expanding” regains momentum. Bitcoin could be rapidly revalued as the debt and liquidity mismatch prevents marginal financial tightening.

Coutts treated the $60,000 zone as a value floor, predicting better than 50-50 odds with the cycle low already in place.

In the bearish case, debt issuance remains heavy, inflation remains high, Treasury funding remains tight, and the Fed cannot ease the inflation it has suppressed for two years without reigniting it.

Bitcoin then behaves less like a financial hedge and more like a high-beta risk asset that is exposed to interest rates, funding conditions, and periodic deleveraging.

S&P Global’s preliminary PMI numbers for April already explain that growth is running at a pace close to 1% per year. This fragile expansion does not need to fall into recession to cause the kind of funding shock that will hit Bitcoin the hardest.

| element | bull case | bear case |

|---|---|---|

| inflation | Cooling down for Fed’s expected path | Remain sticky enough to keep policymakers cautious |

| Treasury cash balance | decreases and the outflow of reserves decreases. | Maintain high standards and continue absorbing liquidity |

| reserve balance | Rebuild from current level | Stay firm or fall further |

| issuance of debt | Continues to be manageable for increased liquidity | Remains heavy and outpaces liquidity growth |

| Fed’s stance | can ease or ease inflation without reigniting it; | No meaningful easing is possible without risking another wave of inflation |

| bank credit | Continue to expand without fear of growth | Expansion is weaker or offset by tighter financing conditions |

| financial situation | loosen the blank space | Restrictive and stressful |

| market plumbing | Treasury supply and reserves cease to act as headwinds | Treasury funding tensions and reserve friction remain key battlegrounds |

| Bitcoin movement | As liquidity theory gains momentum again, re-rates will rise. $60,000 is held as a floor value | Trading like high-beta risky assets with sharp drawdowns, failed breakouts, and potential for retesting lower support |

| Key points for investors | Increased liquidity is sufficient to absorb debt and support risk assets | Liquidity may still be expanding, but not fast enough to offset debt, reserves, and Treasury supplies |

Coutts distinguishes between Bitcoin’s long-term financial problems and the medium-term price movement that reserve flows actually cause.

In a regime where debt exceeds broad funds, the Fed manages a restrictive floor, and Treasury cash balances deplete reserves even as M2 rises, a valid question for investors is whether the expansion is occurring fast enough to simultaneously absorb debt, reserves, and Treasury supply.

Until the debt and reserve situation conclusively favors Bitcoin, the asset will continue to experience the sharp drawdowns and frustrating consolidations that characterize a market caught between long-term constructive theory and a tougher-than-expected short-term funding environment.

(Tag translation) Bitcoin