Bitcoin’s recent price rally stalled as it gave long-term holders and recent buyers an opportunity to sell before the cryptocurrency reached the next major resistance zone.

data from crypto slate The data shows the largest digital asset surpassed $65,000 for the first time in nearly a month on Wednesday, before retreating below $63,000 at press time. The move was Bitcoin’s strongest reaction to positive economic news in weeks, following soft US inflation data.

This setback came despite several market indicators taking a more constructive turn, and was a test of whether a recovery in demand could absorb the supply emerging during the rally and push Bitcoin above $70,000.

Long-term and short-term holders limit Bitcoin recovery

Bitcoin’s failure to sustain above $65,000 showed how quickly the rally from investors on both sides of the recent sell-off is drawing supply.

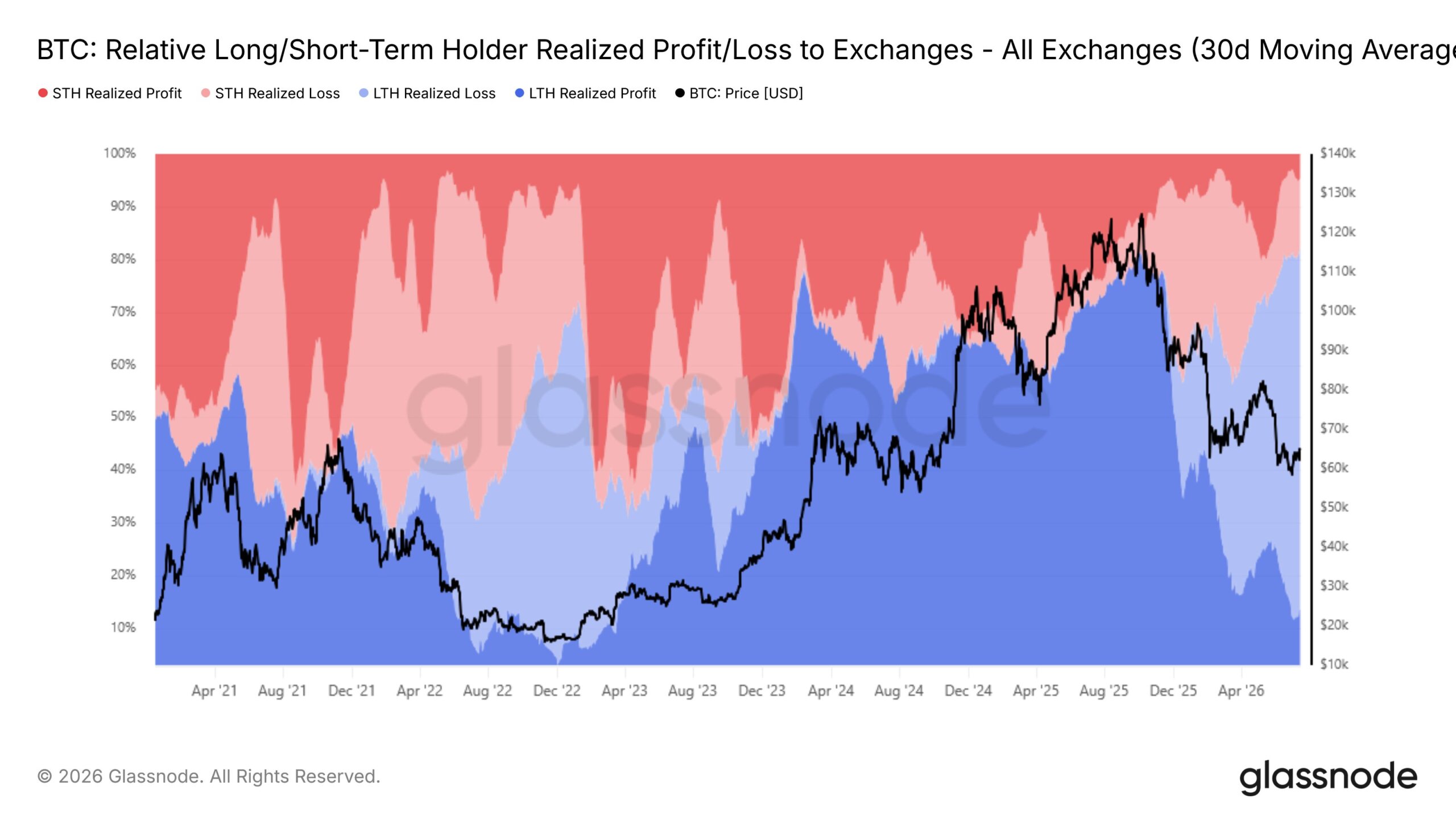

Bitcoin has been trading below the realized price of the 18-month to 2-year UTXO cohort since early June. According to CryptoQuant data. This measure estimates the average price that coins within a group last moved and serves as a proxy for the break-even level.

Since then, as the coin moves in and out of the cohort, its moving cost basis has increased to around $80,800, leaving many of its holders with significant unrealized losses at current prices.

According to data from Glassnode, realized losses for long-term holders increased as Bitcoin approached $66,000. This pullback allowed underground investors to sell at a smaller loss than they faced when the cryptocurrency was trading below $60,000.

Glassnod says:

“More than 65% of currency inflows now come from long-term holders realizing losses, a number consistent with previous bear market phases when this group dominated the sell side.”

This data suggests that rather than waiting for Bitcoin to return to its estimated break-even price, some holders used this pullback to reduce their exposure and add supply to a market already struggling to extend its response to soft inflation data.

At the same time, short-term holders were selling on the same recovery for the opposite reason. Investors who piled into Bitcoin near the June lows began taking profits in volumes last seen near the market’s May peak.

The two groups entered at different prices and recorded different results. Long-term holders are cutting their losses and recent buyers are protecting their gains, but both are supplying Bitcoin as it tries to rise.

Bitcoin remains below its short-term holder cost base of around $69,000, but joint selling by the two companies has increased pressure while another group of recent buyers has fallen below breakeven levels. This level sits near a concentration of options exposure between $70,000 and $80,000, creating an overlapping potential source of resistance.

ETF inflows return as Bitcoin market regime improves

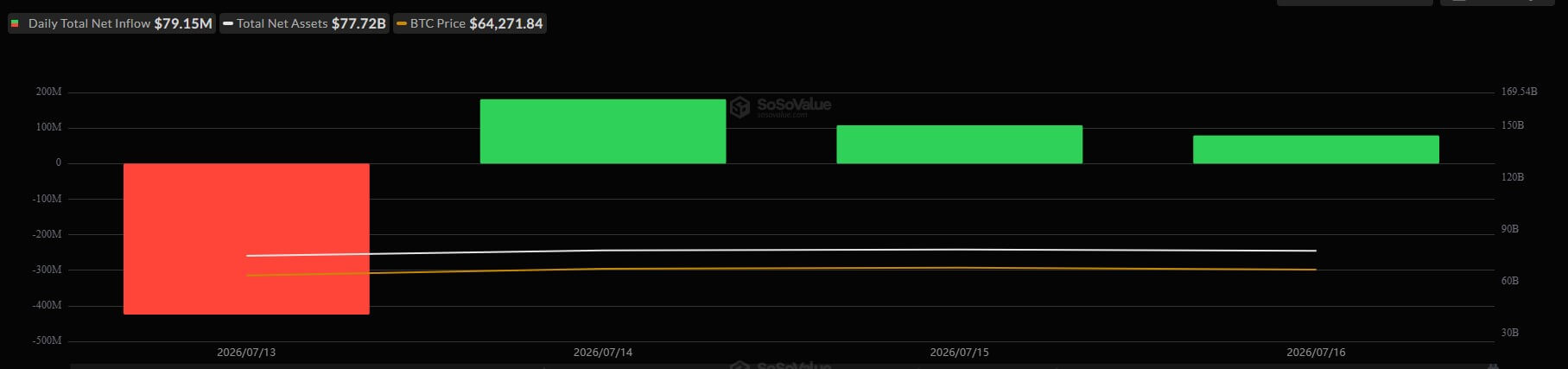

Selling pressure hasn’t erased signs of improving demand, with U.S. spot Bitcoin exchange-traded funds rallying for the third consecutive session after starting the week with a sharp withdrawal.

The fund recorded net inflows of $181.1 million on Tuesday, $107.7 million on Wednesday and another $79 million on Thursday. The $367.8 million total recovered nearly 87% of Monday’s outflow of $424 million, for a net withdrawal of about $56 million.

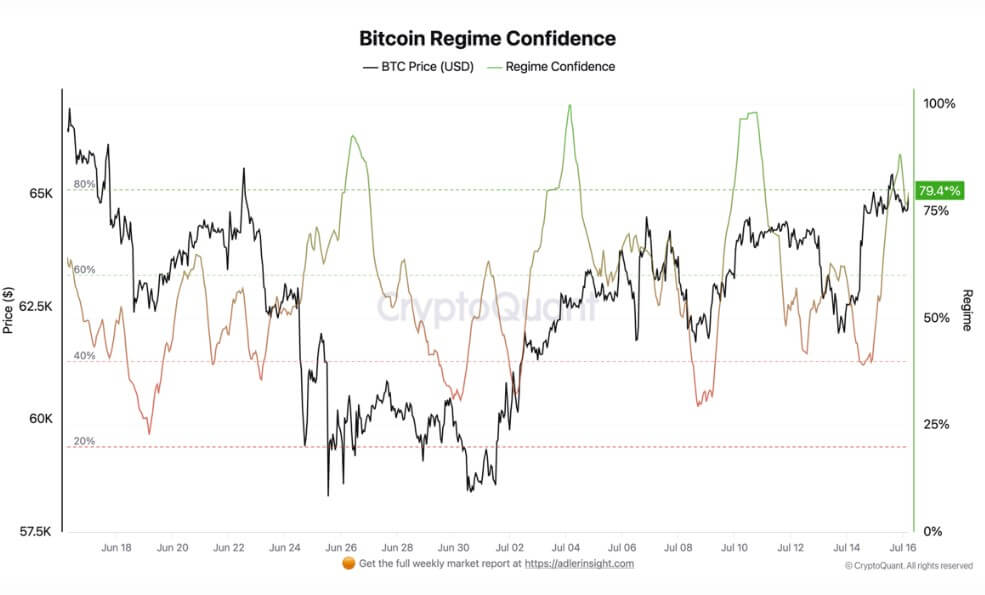

This improvement coincided with a bullish turn in CryptoQuant analyst Axel Adler’s Bitcoin Regime Score. The Bitcoin Regime Score combines taker flows, open interest pressure, funding rates, ETF activity, currency flows, and price trends.

This indicator rose to 34.7 on a scale of -100 to +100. It fell to -42.9 on June 26, when Bitcoin traded around $58,300, but has rarely stayed below zero since July 2.

The score has spent about four-fifths of the past week in positive territory, but about three-fifths of the way through the month. It reached 65.3 on July 10 and retreated toward neutrality four days later, but the decline did not develop into a sustained negative reading.

The agreement between the components of the model was also strengthened. In the past 24 hours, confidence in the regime increased from 54.9% to 79.4%, just below the model’s high confidence threshold of 80%.

The 7-day average increased to 64.3%, while the 1-month average was 57.3%. The rise in both scores and confidence suggests that the improvement is supported by several market launches rather than a single unusually strong factor.

However, the indicator has not yet triggered a definitive price breakout. A rebound in regime scores above 50, with confidence near 80%, would provide stronger evidence that the recovery has regained momentum.

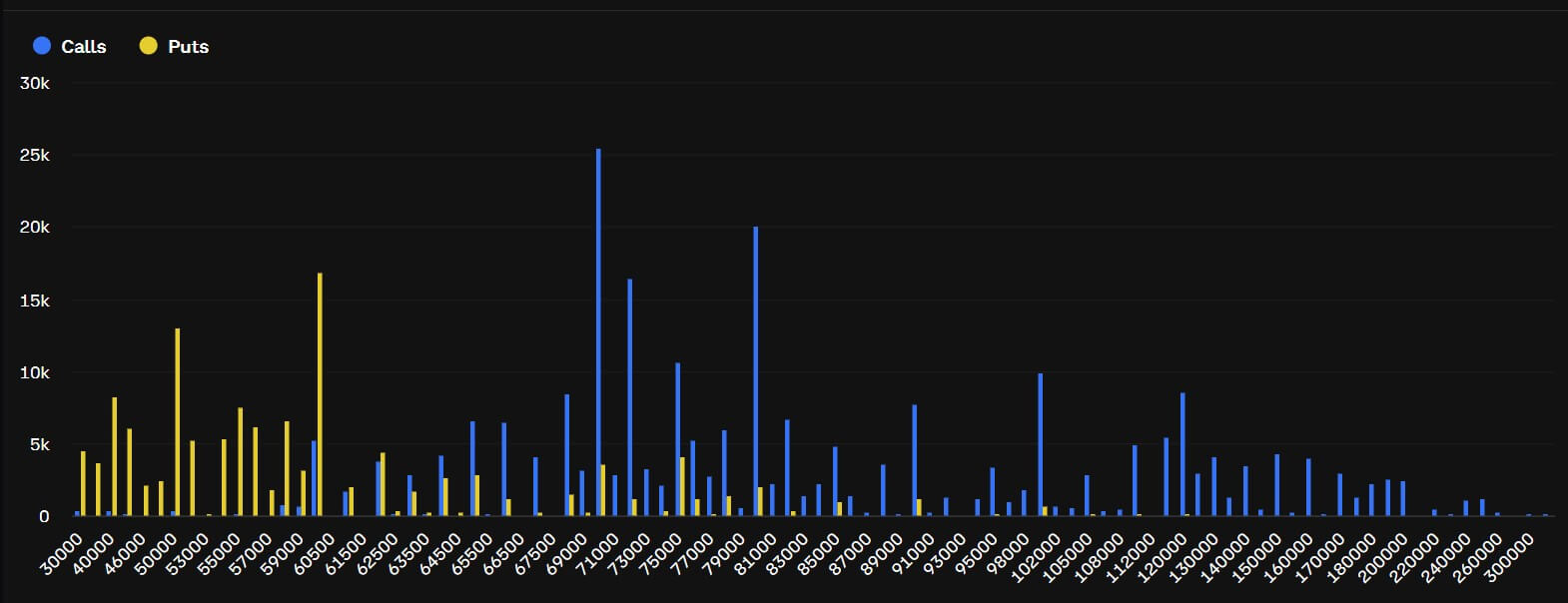

Option exposure exceeds $70,000

The improving system is now facing its first major test in an area where the supply of short-term holders coincides with a concentration of call interest.

According to Deribit data, open call interest in Bitcoin was approximately $1.6 billion at a strike price of $70,000, $1 billion at $72,000, and $686 million at $75,000. Another $1.2 billion is concentrated in $80,000.

These four strikes account for nearly $4.5 billion in open interest and create a broad option corridor that outperforms current market prices.

The short-term holder’s cost basis is close to $69,000 and close to that corridor. Therefore, just as options traders and market makers begin to adjust their positions around the largest call strike, Bitcoin could encounter selling from recent buyers who have returned to breakeven.

Open interest alone does not tell you whether the positioning reflects an outright bull trade, covered call selling, volatility strategy, or portfolio hedging. All options contracts have both buyers and sellers, so the total is an imperfect measure of directional confidence.

Nevertheless, this concentration identifies a level where hedging activity is likely to increase as Bitcoin approaches a strike, especially around large expirations. These corrections can amplify price movements in either direction.

Bitcoin needs stronger demand to clear $70,000

Clearing the options corridor will depend on whether the recent improvement in demand leads to a broader and sustained recovery.

The U.S. Spot Bitcoin ETF posted inflows for the third consecutive session, but reversals remain limited compared to the withdrawals recorded across the two largest funds over the past month.

According to Glassnode data, the combined flows of BlackRock’s IBIT and Fidelity’s FBTC have averaged over 1,250 BTC per day in net outflows over the past 30 days. Trading activity across the ETF market has also declined, suggesting that participation remains subdued despite recent inflows.

Bitcoin will therefore require continued spot and ETF purchases to absorb sales from recent buyers who have returned to break-even, as well as older holders who are taking advantage of the rally to cut their losses.

There are early signs that pressure from long-term holders may be easing. The 30-day average realized losses for this cohort are starting to retreat from recent highs.

The previous bear market established a firmer footing after its measures peaked and entered a sustained decline. However, the current rollover remains too short to ensure that the heaviest distribution has finished.

Until demand strengthens and holder selling eases more definitively, Bitcoin will continue to be caught between improving market signals and the supply that emerges during the recovery.

If the bears fail to clear the overlapping resistance between $70,000 and $80,000, all eyes will be on the downside again. Open interest in puts totals approximately $1 billion at $60,000 and approximately $840 million at $50,000, creating an even greater concentration of options below the current market.

The $60,000 level will be the first big test after being rejected again by a combination of large put concentrations and areas where buyers were previously defending the market.

(Tag translation) Bitcoin