The CME gap should close on Friday.

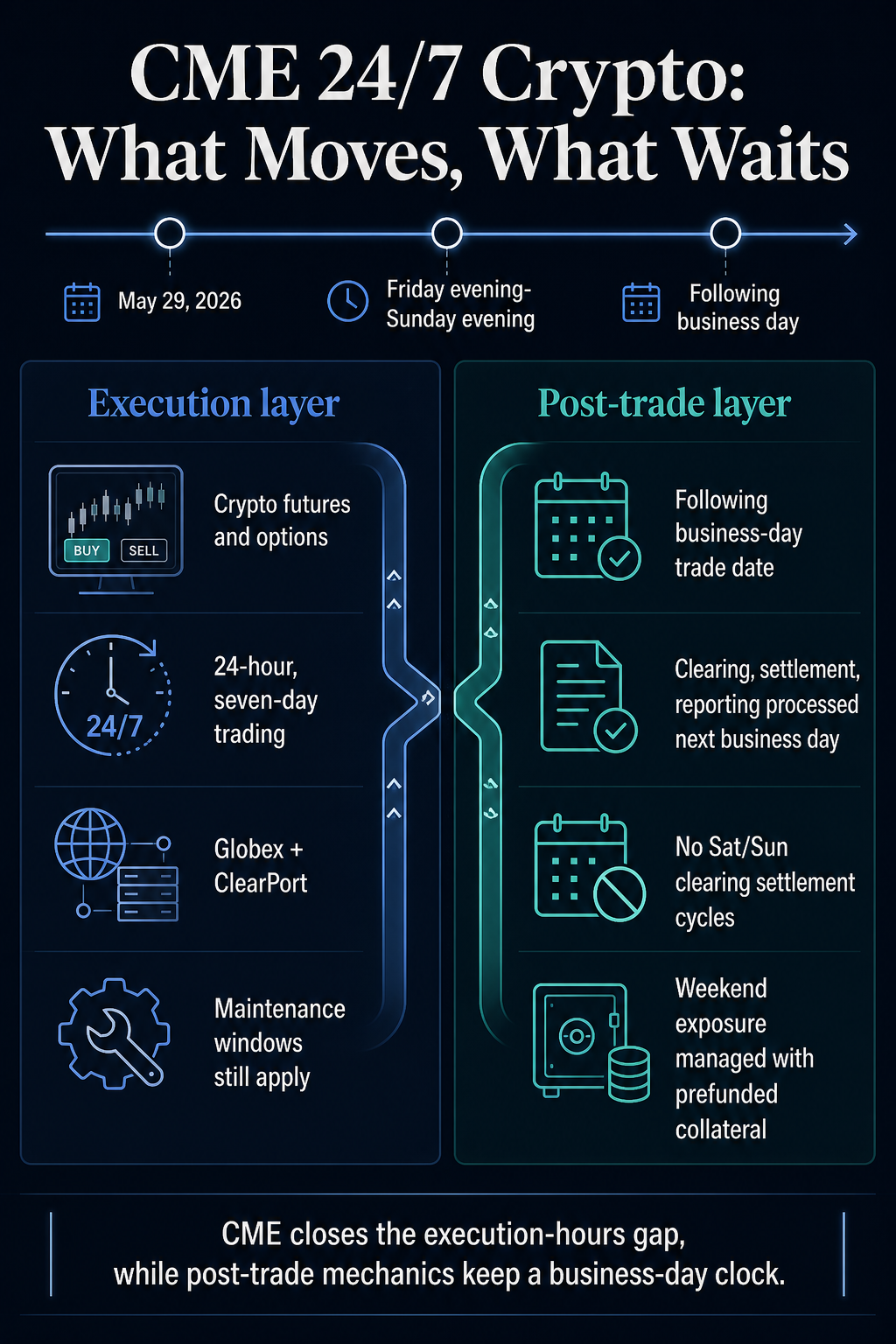

CME Group has announced that it will move its regulated cryptocurrency futures and options to 24/7 trading pending regulatory review starting May 29, cutting into one of Bitcoin’s more familiar institutional markets.

The weekday venue that sparked the CME Gap discussion over the weekend is gearing up to continue matching trades as crypto prices continue to fluctuate.

While CME is extending the hours traders can fill, the rest of the regulated futures stack still maintains a business-day clock.

Weekend and holiday trades between Friday evening and Sunday evening will continue to include the next business day, and CME said that clearing, settlement and regulatory reporting related to those trades will be processed on the next business day.

For participating institutional users, the execution gap is smaller. The more difficult questions shift to liquidity quality, clearing behavior, and post-trade processing on Monday.

Changes in CME

CME announced that regulated virtual currency futures and options will be available for trading 24 hours a day, 7 days a week, starting May 29, pending regulatory review.

The move applies to the exchange’s crypto futures and options complex, is subject to a maintenance period, and will be implemented through CME Globex and ClearPort.

The commercial case is clear. CME said customer demand for risk management of digital assets has reached record levels, with total notional value across crypto futures and options reaching $3 trillion in 2025.

It also reported that the average number of contracts per day from the beginning of 2026 to date was 407,200, an increase of 46% from the previous year.

These numbers show why the weekend access problem goes beyond a meme. In firememecoins’s May 27 snapshot, Bitcoin was trading at around $75,782, with a market cap of nearly $1.52 trillion and 24-hour volume of nearly $35.17 billion.

In a market of this size, the closure of regulated derivatives exchanges through the weekend could leave the desks of financial institutions managing price risk in a time zone mismatch.

For traders who use futures to hedge spot exposures, manage basis, or offset ETF-linked flows, the real question is whether the regulated products they are allowed or required to use will be able to respond if prices move beyond the previous CME week.

CME’s move will give eligible participants a regulated execution channel during a period that was previously outside the trading window.

This access could change the way you absorb shock over the weekend. Instead of compressing all moves into a Sunday night or Monday restart, participating desks can hedge, roll, quote, or adjust their exposure while the broader crypto market is already trading.

This improvement has implications for basis trading, ETF-linked exposures, liquidation risk, and headline-driven volatility, even though the rest of the regulatory workflow remains more constrained.

For CME, this scale also moves the launch from product housekeeping to market structure work. A leading derivatives franchise is adapting its access model to asset classes that maintain pricing risk throughout the weekend.

After-trade clock runs even on business days

CME’s clearing and global operating guidelines specify limits on changes. Business days from Monday to Friday will continue to be five days, and Saturday and Sunday payment cycles are outside the scope of the new settings, the document said.

This distinction is operationally important. Execution will be continuous, but the official mechanism for turning trades into cleared obligations is still biased towards the next business day.

| layer | weekend changes | business day mechanic |

|---|---|---|

| trading access | Cryptocurrency futures and options are subject to maintenance periods and can be traded through weekends and holidays. | Some clients may maintain 5 days of access instead of enabling 7 days of trading. |

| trading date | Trading can be carried out from Friday evening until Sunday evening. | The next business day’s trading date applies to these transactions. |

| Clearing and settlement | Weekend trading is accepted into a regulated workflow. | Payment cycles will wait until the next business day to process. |

| regulatory reporting | Weekend activities join the reporting chain. | Reports related to weekend and holiday activities will be processed the next business day, CME said. |

Its design reflects unresolved operational issues in regulated crypto markets. Although the price of cryptocurrencies can fluctuate continuously, futures markets rely on clearing members, collateral, risk management, settlement cycles, reporting records, and operating staffs built on the discipline of the business day.

CME’s guidelines outline how exchanges seek to bridge the discrepancy. Clearing members participating in supplementary trading hours must be approved by CME Clearing.

Risk policies and procedures are required to cover extra time, such as account monitoring, credit management, position limits, daytime and nighttime monitoring, and defined liquidity sources.

At certain times during the weekend, CME Clearing monitors exposure to posted performance bonds and available liquidity. Clearing members must submit a weekly liquidity template and deposit the required collateral for anticipated weekend clearing activity into a separate weekend clearing account by Friday afternoon.

These mechanisms are the back-office version of 24/7 trading. This means preparing your risk tolerance in advance and monitoring it until the working day cycle catches up.

weekend liquidity needs to be proven

The old CME Gap was simplified as Bitcoin and other crypto assets continued to trade while CME’s institutional facilities were closed. If spot prices spiked on Saturday, CME futures subsequently resumed at a different level, creating a visible gap on the chart.

That chart pattern was only part of the problem. Even more serious was the suspension of regulated access at the very time that native cryptocurrency exchanges, offshore platforms, ETFs, market makers, and leveraged traders could still be forced to respond.

CME’s BTIC document shows how weekend access goes beyond directional betting, as well as basis trading and ETF workflows centered around crypto futures.

Simply put, basis trading at index closing prices allows participants to trade crypto futures basis against the CME CF reference rate, including closing reference rates in London, New York, and APAC. CME also cited NAV risk from ETF creation and redemption as a use case.

This puts CME’s derivatives complex closer to the pipes for institutional exposure. Desks that manage benchmarking against reference rates, hedging ETF-linked exposures, or forward carryovers against cash needs products, margin processes and liquidity during price movements.

Access alone does not yet prove market quality. If weekend trading is thin, spreads widen, or constraints are difficult to clear during times of stress, the market can feel more available and less fully continuous.

CME appears to be aware of that risk. Separate CFTC filings show a weekend market maker program for virtual currency futures and options.

The option program requires participants to quote continuous two-sided markets for the target product at the maximum bid-ask spread and minimum quote size within the required market time.

These filings do not indicate an active weekend market, but rather support the launch liquidity program. The first real measurements will be practical, such as which clearing members will provide 7-day access, what the trading volume will be in the old after-hours period, how weekend bid/ask spreads will compare to weekdays, whether options quotes will remain reliable, and whether exposure alerts and prefunding requirements will shape behavior during volatile periods.

There are two possible paths. In the enhanced version, CME’s weekend access becomes a genuine pressure valve.

Institutional traders can hedge, roll, quote, and adjust their exposure while the crypto-native market is already moving, making Monday more of a paperwork point than a delayed risk event.

In the weaker version, although the venue is technically open, liquidity remains uneven and many users still treat Monday as the real moment when weekend activity becomes visible in clearing, settlement, and reporting.

The launch will still be important. It would indicate that the weekend gap has moved from the price chart to market depth and operations.

CME’s 24/7 launch will provide institutional investors with access to familiar futures and options products during weekend and holiday fluctuations in Bitcoin and the broader crypto market.

It also reveals the limits of the shift. Regulated cryptocurrencies can be traded like cryptocurrencies, but are cleared and reported through machinery built for business days.

As for the weekend difference, the divide became clearer. CME is likely to discontinue the most visible version for traders who have access to the venue throughout the weekend.

The more difficult part is moving to a less obvious location. It’s whether liquidity, risk management, and settlement behavior will make regulated cryptocurrencies continue to make themselves felt when the back office still keeps the clock on the business day.

(Tag translation) Bitcoin