Asset management firm Grayscale said a small group of blockchain companies are already working on decentralized finance (DeFi) and tokenized assets, including Ethereum, Solana, $BNB Chain and Canton Network are best positioned to absorb the first wave of institutional capital if the US passes the Clarity Act, the long-promised cryptocurrency rulebook.

The CLARITY Act passed the Senate Banking Committee on May 14 by a vote of 15-9. It now requires a full vote in the Senate, reconciliation in the House of Representatives, and a signature by the president.

But the current calendar poses another constraint. Cryptopolitan reported in a May 21 post that the bill will compete for consideration time in June with reconciliation, the Foreign Intelligence Surveillance Act, and the housing bill that passed the House this week.

Which network does Grayscale say will absorb the first wave of institutional capital?

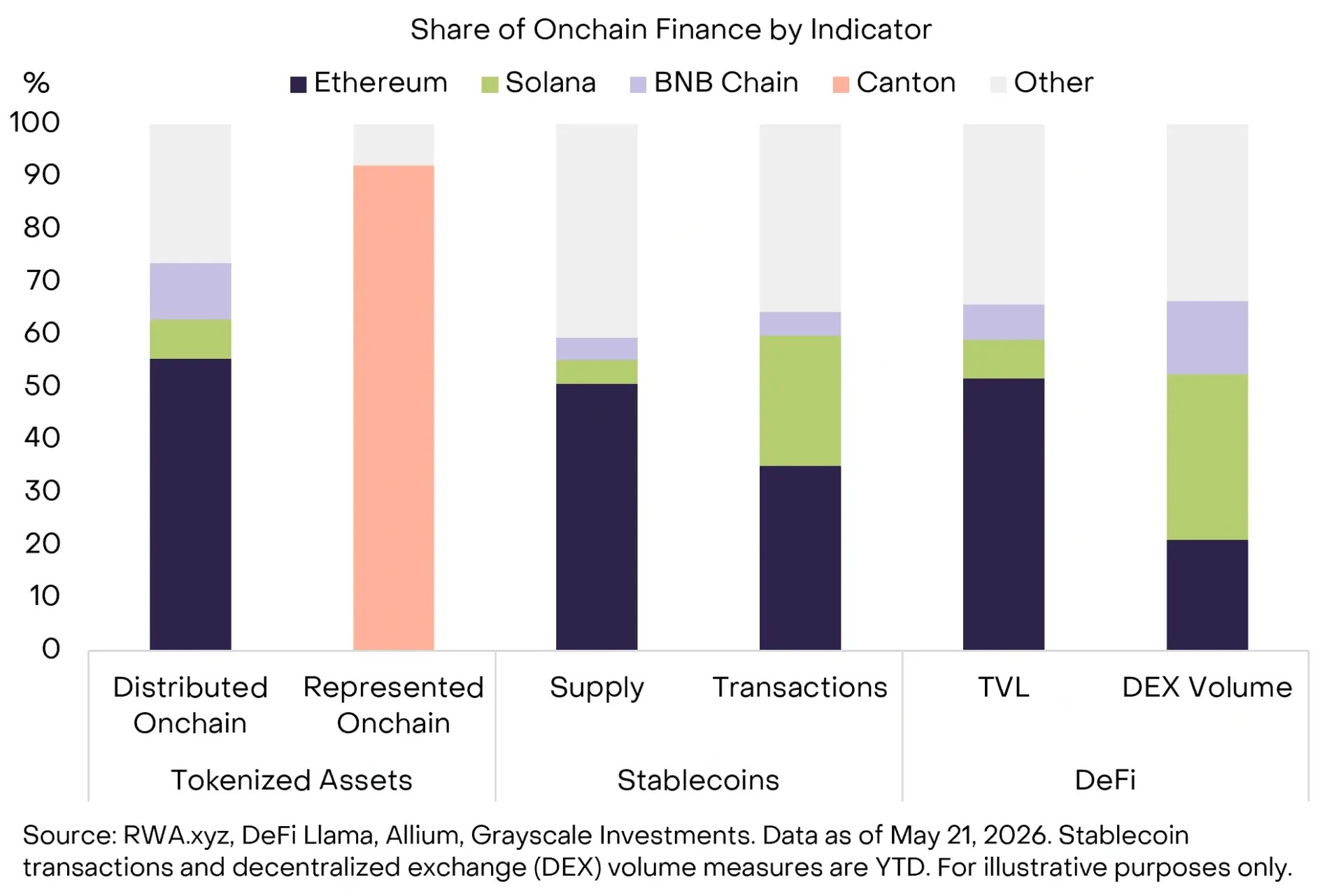

Ethereum currently leads in tokenized assets with full on-chain functionality, followed by Ethereum. $BNB Chain and Solana.

Canton Network also has a reputation for being a major organizational niche. According to the previous grayscale Tokenization Megatrend ReportCanton leads all blockchains in total on-chain capital with over $348 billion in tokenized asset value, backed by DTCC’s selection of the network under the SEC’s No-Action Letter Framework.

When it comes to stablecoins, the same blockchain stands out in terms of supply and transaction volume. The current TVL in DeFi is: $82.08 billionEthereum, Solana, $BNB Chains are a big part of that. They also lead application activities.

Grayscale highlighting The list of second-tier platforms includes Avalanche, Ethereum Layer 2 networks Base and Arbitrum, perpetual currency-focused Hyperliquid, and stablecoin-focused Tron as beneficiaries.

Zach Pandl, head of research at Grayscale, noted that although Bitcoin does not natively support smart contracts and has a more limited Layer 2 ecosystem, it will still benefit from regulatory clarity as the industry’s safest asset and primary collateral.

When will the CLARITY Act be passed? What could derail it?

According to Eleanor Terret, host of the “Crypto in America” podcast, “The reality is beginning to set in whether the Senate will be able to pass two major pieces of legislation amidst time constraints and competing priorities, and the question now is whether one will inevitably be pushed into July.”

He pointed out that there will be four working weeks in June and three working weeks in July before the August holidays.

Sen. Cynthia Lummis said a Congressional vote in June is likely quite optimistic.

DeFi may also be subject to stricter regulation.

These deliberations are ongoing, but the SEC is not waiting. The agency announced on March 17th, published a joint interpretation The Commodity Futures Trading Commission (CFTC) has established consistent definitions and classifications across digital products, collectibles, tools, stablecoins, and digital securities.

We also discussed airdrops, protocol mining, staking, and wrapping of non-security assets, as well as clarifying how non-security crypto assets may or may not be subject to investment contracts.

“This work is an important bridge for entrepreneurs and investors as Congress works to advance bipartisan market structure legislation,” said SEC Chairman Paul S. Atkins. “I look forward to working with Chairman Selig to implement it in the near future.”

Regulations are being clarified in the DeFi field as well. As Cryptopolitan reported in April, the DeFi Education Fund (DEF) and 35 other co-signatories called on the Securities and Exchange Commission (SEC) to elevate the staff guidance on DeFi interfaces into law, ensuring that there is no turning back once the new regime is in place.

As it stands, this guidance is only an interim staff statement and is considered to be withdrawn five years after its publication date, unless the Commission specifies otherwise or makes it into a regulation.

A staff statement released by the SEC’s Division of Trading and Markets on April 13 clarifies that certain virtual currency trading interface operators are exempt from registering as broker-dealers.