Mark Cuban sold most of his Bitcoin because confidence in fiat currencies waned and it did not work as a hedge at a time of heightened geopolitical risks.

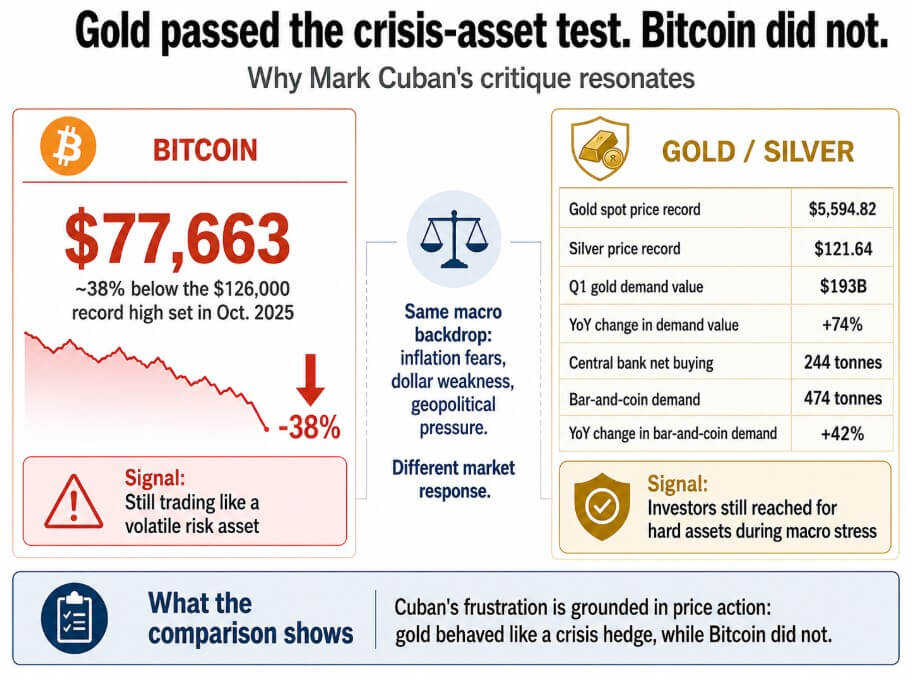

Mr. Cuban called it “not the hedge we were hoping for,” and price records bear out his complaints. Bitcoin is trading at around $77,663 as of mid-May 2026, about 38% below its all-time high of $126,000 set in early October 2025.

Spot gold reached an all-time high of $5,594.82 on January 29, and silver reached $121.64 on the same day, driven by the same macro variables cited by Cuba: inflation concerns, a weak dollar, and geopolitical pressures.

According to data from the World Gold Council, gold demand in the first quarter reached 1,231 tonnes, including OTC, and the dollar value of quarterly demand increased 74% year-on-year to a record high of $193 billion.

During the same period, the central bank purchased a net amount of 244 tonnes, and demand for bullion and coins reached 474 tonnes, an increase of 42% year-on-year. Cuban also told Portfolio Players that he is moving more money into Ethereum than Bitcoin, but the hedging criticism is specific to Bitcoin.

There has always been a problem with selling “digital gold”

Bitcoin.org describes the asset as a peer-to-peer currency with no central authority or bank, and specifies that the amount issued will halve over time, eventually stopping at 21 million Bitcoins. There is nothing in that explanation that promises Bitcoin will rise when geopolitical stress increases.

Mr. Cuban built his thesis around the “digital gold” narrative that the market constructed and that the Bitcoin White Paper never supported.

Bitcoin trades as a liquidity-sensitive high-beta asset, correlating with the Nasdaq during risk-off periods and spiking when risk appetite picks up.

Last year, cryptocurrencies were pegged to broader equities through the tariff shock in April before Bitcoin hit an October record, then suffered significant deleveraging. More recently, Glassnode’s May 20 report stated that Bitcoin is structurally resilient, but noted that spot demand has weakened, ETF accumulation has slowed, and options positioning has turned defensive.

Mr. Cuban applied the gold benchmark to an asset that does not fluctuate as consistently as gold. As a result, the discrepancy between his expectations and the price prompted him to sell.

| test | gold | Bitcoin |

|---|---|---|

| crisis behavior | A cleaner panic shelter | Often sold along with risk assets |

| volatility profile | lower and more established | much higher and sensitive to recruitment |

| Main demand factors | Inflation fears, geopolitics, and central banks | ETF flows, liquidity, regulation and leverage cycles |

| monetary property | No publisher, physical rarity | 21 million cap, no central issuer, unauthorized transfers |

| best framing | crisis shelter now | Financial discretion can be obtained later. |

The supply of long-term Bitcoin holders increased by more than 2 million BTC during this drawdown, reaching 16.3 million BTC, with about 200,000 BTC added in the last month alone. Cubans are judging Bitcoin on whether it performs like gold in a crisis, while long-term holders are judging whether the network is still working and whether the supply cap can be maintained in 10 years.

Although hedging reduces portfolio risk during stress events with some consistency, Bitcoin’s realized volatility far exceeds that of gold, its price responds to ETF flows, regulatory headlines, leverage cycles, and is repeatedly correlated with equity drawdowns during severe stress.

These are the mechanisms of a nascent financial network that still prices in the uncertainty of implementation, and could be powerful in the long run, precisely because this asset is too volatile and liquidity sensitive to act as a short-term panic hedge.

Investors will turn to Bitcoin when the financial system itself is expected to change dramatically over the next 10 years, if the adoption theory holds true. Fixed supply, permissionless transferability, and the absence of a central issuer make Bitcoin worth considering as a long-term monetary option.

Distance between $58,000 and $165,000

Citi’s March 2026 outlook, with a base 12-month target of $112,000, a recession downside of $58,000, and a bullish outlook of $165,000, shows how widespread the resulting uncertainty is.

Glassnode has set the realized price at around $54,900 as the lower bound of the structure, with the $70,000 level carrying weight as a pre-election anchor.

| scenario | BTC level/range | market logic | the end of the story |

|---|---|---|---|

| structural floor | ~$54,900 | lower bound on realized price | Below this point, the case for employment weakens. |

| recession bear case | $58,000 | Rising yields, ETF outflows, and weak spot demand | Bitcoin is traded like a risk-mitigating asset |

| key anchor | $70,000 | Pre-election standard level | Market tests whether support is real |

| basic case | $112,000 | Citi’s 12 Month Goals | Bitcoin survives as a volatile currency option |

| bull case | $165,000 | ETF demand, regulation and risk appetite recover | Adoption theory absorbs hedging failures |

On the bearish side, rising yields, continued ETF outflows, and weak spot demand will keep Bitcoin pinned near structural support.

Bitcoin trades like a risk-averse asset, indistinguishable from the broader risk-off environment, and gold continues to absorb the crisis-hedging flow that Bitcoin marketing promised to capture.

In the bullish case, demand for ETFs recovers, U.S. regulatory developments give financial institutions a cleaner start, and risk appetite returns enough to push Bitcoin back towards $165,000, beyond the City’s $112,000 target.

Bitcoin has overcome criticism by acting as a rare, borderless, permissionless monetary network that increases in value as more institutions and sovereigns seek assets outside of traditional finance.

The 21 million supply cap and lack of a central issuer are characteristics that make Bitcoin worth holding as a long-term bet that financial mistrust will become infrastructure, and Cuba cites the same characteristics held by the drawdown as evidence of failure.

The real case for Bitcoin lies in providing exposure to a world where more people seek money outside of the traditional system, and this is true regardless of how Bitcoin performs against gold in any given crisis.

Bitcoin as a call option against financial mistrust

Cuban wanted Bitcoin to serve as a predictable and consistent protection against certain risks he saw coming.

However, Bitcoin may be more like a call option for financial mistrust. While it has value if the theory lasts more than 10 years, it is unstable over that time and is a poor substitute for gold in times of severe stress.

Gold remains the cleanest crisis asset by any recent metric, as shown by record prices, record quarterly demand, continued central bank buying, and consistent performance against the macro variables that define true panic.

The asset, for which Cuban sold most of his holdings, still has a supply cap of 21 million BTC, still operates without a central issuer, and still has accumulated long-term holder supply of 200,000 BTC last month.

Whether that’s enough to justify the $58,000 to $165,000 price range over the next year will depend on whether the adoption theory can replenish what the hedging theory loses.

(Tag translation) Bitcoin