Morgan Stanley launched the Spot Bitcoin ETF on NYSE Arca on April 8th, calling MSBT the first crypto ETP from a US bank-affiliated asset manager, and setting the sponsor fee at 0.14%, the lowest sponsor fee for a Bitcoin ETP.

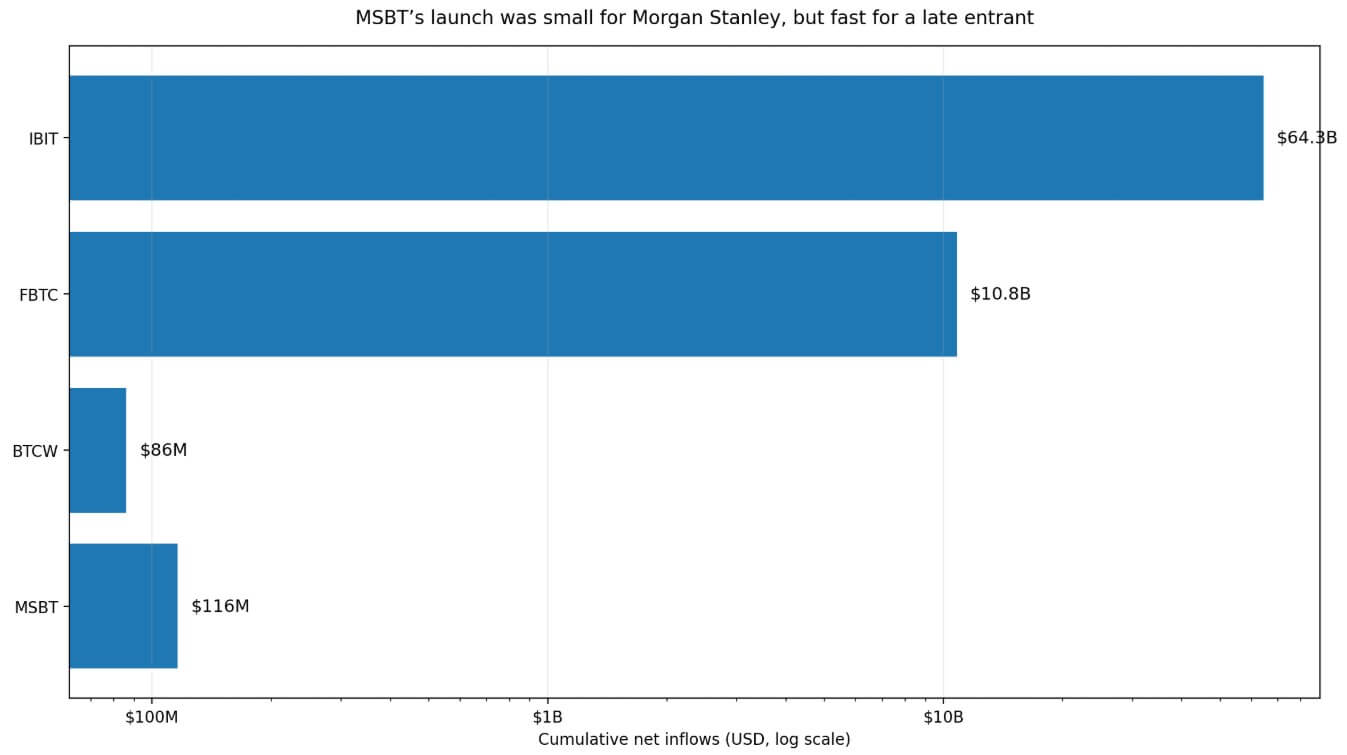

Cumulative net inflows totaled $116 million over seven trading sessions through April 16, according to data from Pharside Investors.

This figure represents about 0.006% of Morgan Stanley Investment Management’s $1.9 trillion in assets under management as of December 31, 2025. At a fee rate of 0.14%, if the assets were held at that level, the total annual return would be only about $162,400.

What makes MSBT’s launch difficult to ignore is the competitive calculation.

traveling numbers

With net inflows of approximately $16.6 million per session, MSBT has already surpassed BTCW, with cumulative inflows of $86 million, according to Farside.

For a latecomer to the volatile Bitcoin market, clearing the total of existing competitors in less than two weeks would prove that brand, price and distribution can still generate demand in a space already dominated by BlackRock’s IBIT ($64.3 billion) and Fidelity’s FBTC ($10.8 billion).

Morgan Stanley has transformed “cryptocurrency access” into “cryptocurrency manufacturing.”

The filing marks the first move by a major U.S. bank, and Morningstar’s Brian Armor told Reuters the bank’s entry into the crypto ETF market lends legitimacy and could encourage other banks to follow suit.

Goldman Sachs filed its first Bitcoin ETF product on April 14, six days after the launch of MSBT. The timing reinforces the sense that reputational barriers to bank-branded Bitcoin products are rapidly shrinking.

Morgan Stanley’s own statement positions MSBT as part of its company-wide digital asset drive across custody, trading and product development. A fund is both a product decision and a positioning decision.

The 0.14% fee sets a price anchor that signals to the market that Morgan Stanley intends to compete on cost and reliability, and reveals how it expects the category to evolve.

the battlefield is wide

Bank of America has announced that advisors on its Private Bank, Merrill, and Merrill Edge platforms will be able to recommend cryptocurrency allocations without asset criteria starting January 5th.

Charles Schwab announced on April 16 that it will phase in direct spot trading of Bitcoin and Ethereum for retail customers in the coming weeks. Taken together, these moves indicate that the fight for Bitcoin’s next wave of funds will be fought through a customer experience that integrates advice, intermediary access, and custody.

| hard | move | date | what to control | why is it important |

|---|---|---|---|---|

| morgan stanley | Start MSBT | April 8th | ETF wrapper | Proving that bank-branded products can attract assets |

| goldman sachs | Apply for the first Bitcoin ETF product | April 14th | ETF pipeline | Signaling Peer Reactions/Reducing Prejudice |

| bank of america | Advisors can recommend cryptocurrency allocations | January 5th | Advice/Distribution | Opening up cryptocurrencies to mainstream wealth channels |

| charles schwab | Expanding direct trading between BTC and ETH | April 16th | trading interface | Capture client flows without the need for your own ETF |

MSBT is demonstrating that banks can attract capital by wrapping Bitcoin in a familiar product, while Bank of America and Schwab are demonstrating that banks can capture the same customer relationships simply by controlling the recommendations and transaction interfaces.

Companies with neither wrapper nor client touchpoints now face particular competitive pressures as rivals accumulate either wrappers or client touchpoints, and in some cases both.

Citi projects that U.S. ETF assets will more than double from about $10.4 trillion to $25 trillion by 2030, with active ETFs increasing their share. Bitcoin products compete within an ETF industry already organized around fee compression, distribution control, and the inclusion of model portfolios.

Latecomers to the environment tend to win on price and platform, which is exactly the bet Morgan Stanley’s 0.14% fee suggests.

The permission signal becomes a wave

If MSBT’s opening pace continues, far-side calculations would result in close to $498 million after 30 trading sessions and over $1 billion after 63 trading sessions.

Linear projection extrapolates the current pace to the scenario, and the direction it shows has real strategic importance.

Goldman’s application could turn into a launch product by late June, while other firms monitoring the two big banks’ moves in the coming days face weak internal complaints of inaction.

Morningstar argues that the bank’s entry increases legitimacy, and other banks could follow suit, gaining more power as new institutions move in.

In the case of Bitcoin, that path produces results measured in more bank-branded wrappers. This means a more traditional allocation path through advisor model portfolios, standard brokerage workflows, and custody integrated access for customers who have never opened a crypto exchange account.

As such, demand is more sticky, slower-moving, and less dependent on retail sentiment cycles.

Citi’s 12-month baseline target of $112,000 and bull case’s $165,000 represent the outside of what broader institutional normalization can support if the current series of launches and sales expansions continues.

Fed Director Christopher Waller said a quick resolution to the Middle East conflict could keep hopes of lowering interest rates by the end of the year. Goldman Sachs, Morgan Stanley and Bank of America all predict two rate cuts starting in September.

Easing financial conditions will support risk assets across the board, and Bitcoin will derive further tailwinds from a significant change in the interest rate path.

crowded category

A less constructive interpretation of the same data would suggest that early inflows into MSBT support the feasibility of launching a banking brand while leaving the category leader’s distribution moat intact.

IBIT’s $64.3 billion and FBTC’s $10.8 billion represent advantages in scale, liquidity, and advisor familiarity that have accumulated over several years and favorable regulatory moments.

If flows flatten out after the launch window, a common pattern for new ETF entrants, rivals could conclude that the distribution moat around IBIT and FBTC is wider than Morgan Stanley’s launch suggested.

| scenario | MSBT flow path | What is being said about Wall Street | What it means for Bitcoin |

|---|---|---|---|

| Launch pace maintained | Approximately $498 million after 30 sessions. More than $1 billion since 1963 | Bank-branded Bitcoin wrappers are commercially viable | Access to more formalized institutions |

| Slow flow but stay healthy | ~$250 million to $500 million | A viable niche product, but not a category disruptor | Positive for access, but limited direct impact on prices |

| the flow suddenly disappears | ~$250 million or less | IBIT/FBTC distribution moat remains dominant | Symbolic verification but limited support range |

In that scenario, the industry’s response would shift from “launching its own ETFs” to “expanding access through advice and direct trading,” which Bank of America and Schwab are already doing.

In the case of Bitcoin, the result provides symbolic validation. Glassnode’s cumulative trend score is 0, and the company’s language regarding the recovery is cautious, with Bitcoin remaining approximately 40% below its all-time high of $126,223.

In such an environment, markets sustained by selective flows and limited buyer coalitions remain vulnerable to macro reversals and shifts in sentiment.

Citi’s $58,000 recession downside case represents a 12-month bearish envelope if financial conditions remain tight and institutional bids lose depth.

As weekly inflows for MSBT remain above $50 million or compress to single digit numbers as launch premiums fade, Goldman’s application turns into an actual listed product, other firms respond through manufacturing or alternative advice and intermediary access, and fee competition intensifies, it will become clear which path is taking shape.

A second or third bank entrant below 0.14% will point out that the category is entering a distribution war. This tends to expand access while compressing margins for all participants.

Major banks have now established that bank-branded Bitcoin exposure is commercially viable with physical products and a real asset base. Goldman filed a few days later.

Every company following this trend calculates that moving costs are lower than they were a month ago.

(Tag translation) Bitcoin