Bitcoin Treasury Preferred Stock is moving from a simple income story to a credit test on Bitcoin’s balance sheet.

While Strategy remains the focus, Strive, the seventh-largest public Bitcoin holder, has publicly revealed its ramifications. Another Bitcoin treasury firm held Strategy preferred stock and had watched its position signal market stress.

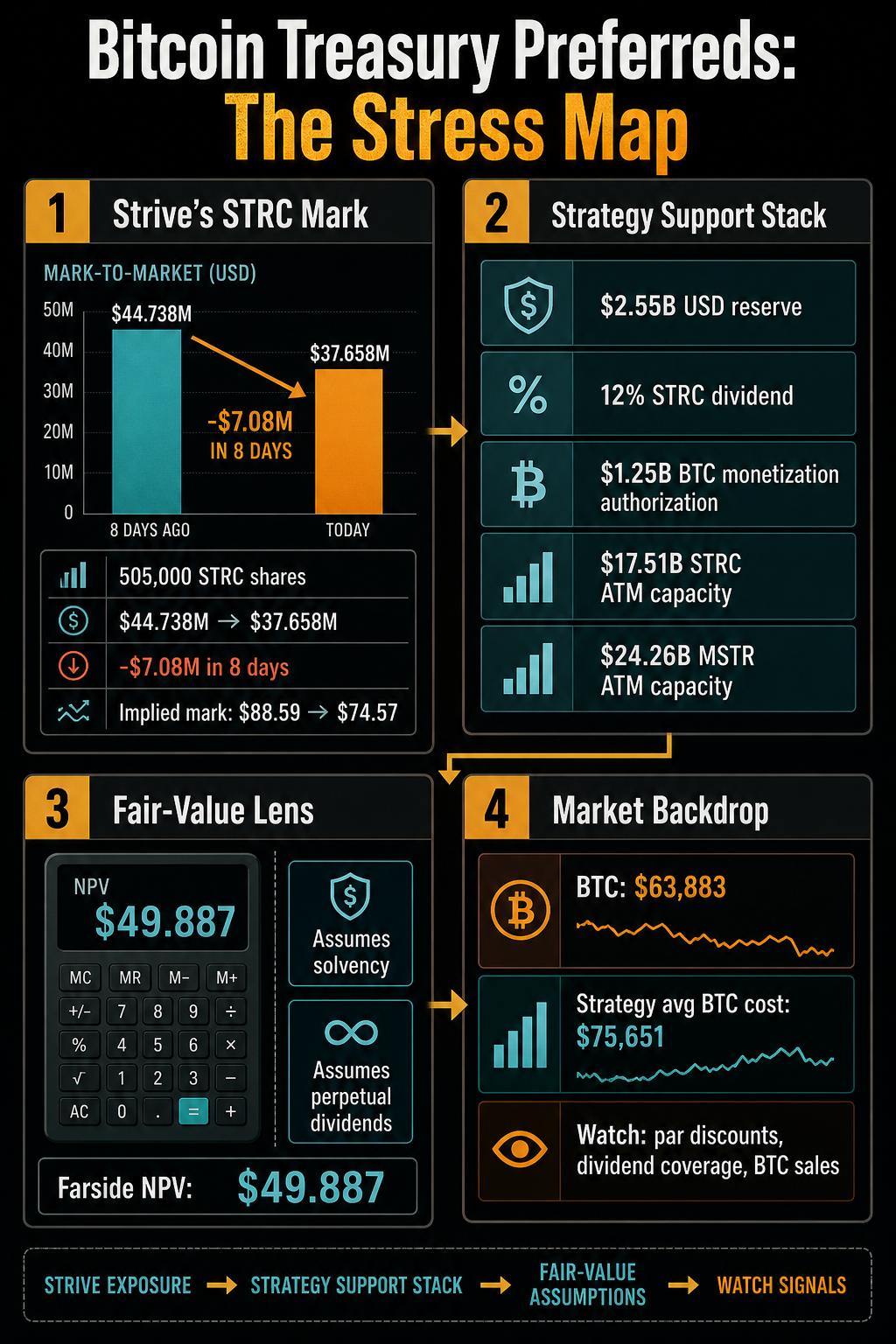

In an update on June 29, Strive revealed that while it held the same 505,000 shares of STRC stock on June 18 and June 26, the fair value of that position fell from $44,738,000 to $37,658,000.

This $7.08 million change occurred without disclosure of the change in the number of STRC shares. Simply dividing the submitted fair value numbers, Strive’s implied mark rose from approximately $88.59 per share to $74.57 per share in eight days.

This disclosure stops short of proving bankruptcy, forced sale, or a broken capital model. It shows something more specific. Stress on Bitcoin’s own preferred stock could spill over to other companies’ balance sheets before a dramatic collapse occurs.

Strive still reports holdings of 19,864 BTC, $141.7 million in cash and equivalents, and 7,829,502 shares of its SATA preferred stock outstanding as of June 26th. A stronger signal is how disclosed strategy-preferred exposures change how investors view the category.

The most powerful indicator is how disclosed strategy-first exposures change the way investors view the category.

The public question surrounding Strategy’s STRC is whether investors are still treating it as an income product or as a stress credit related to Bitcoin, market liquidity, and the Strategy’s ability to support dividends. Strive’s disclosure makes that question even bigger.

When a Bitcoin treasury company owns preferred stock in another Bitcoin treasury company, a visible intercompany channel is created. If STRC trades at a discount, Strive can represent its losses at its independently reported fair value. If SATA were to come under similar scrutiny, the market would have a way to compare whether the stress is isolated or widespread across the preferred stock financing model.

Private products of preferred stock are sold based on yield, stated value, and periodic payments. As such, it looks familiar to income investors. Commodities begin to trade like credit when the central questions become discounts to face value, reserve ranges, dividend resets, buybacks, and asset sales possibilities.

Investors are now asking whether issuers have enough cash support, market access, and Bitcoin liquidity to maintain the credibility of their coupons.

Strategy’s new strategy is similar to credit management

Strategy’s own June 29 filing reinforces that change. The company announced its Digital Credit Capital Framework, which consists of a USD reserve policy, a revised STRC dividend policy, preferred securities repurchases, common stock repurchases, and a BTC monetization program. These are tools for managing capital structure under market pressures.

Strategy said its U.S. dollar reserves stood at $2.55 billion as of June 28, and management must maintain expected annual preferred stock dividend payments and interest debt for at least 12 months, unless the board approves a lower level. The filing states that reserves can be replenished through BTC sales under the monetization program and other capital market activities.

This provision is significant because Strategy has also increased STRC’s regular dividend rate to 12.00% per year, with record dates on or after July 1 and payable semi-monthly. Strategies said it declared cash dividends of $0.50 per share for the periods ending July 31 and August 15, pursuant to the terms of STRC’s designation certificate.

While increasing dividends can support the income vehicle, it also raises the question of how durable the payments are if the security remains discounted.

The strategy made that feedback loop clear. STRC’s dividend policy takes into account STRC’s trading levels, market yields, credit spreads, Bitcoin price and volatility, reserve coverage, capital market conditions, and the company’s overall capital structure. The filing also states that STRC’s dividends are not guaranteed and will not necessarily increase just because STRC is trading below the stated amount.

That is the language of active credit management. The strategy has also authorized the repurchase of up to $1 billion of digital credit securities, with STRC expected to be the first priority if management determines that repurchases will increase and support the capital structure. Authorized an additional $1 billion for the repurchase of Class A common stock. These authorizations do not require companies to purchase securities, but they do indicate a range of tools available to management if discounts become too harmful.

By the same framework, selling BTC will also be part of the discussion. Strategy’s board of directors has approved a BTC monetization program that will sell Bitcoin and generate up to $1.25 billion in U.S. dollar reserves, allowing management to fund or replenish preferred dividend and interest payments and fund security repurchases rather than issuing common stock or using other capital market transactions.

The company made it clear that the program does not mandate the sale of Bitcoin. Still, authorization changes the discussion. Balance sheets built around accumulation now have a formal path to using BTC to protect part of the credit stack.

Fair value test is about durability

Farside’s public STRC fair value calculator provides one way to see why the discussion is moving beyond the headline yield. As confirmed by firememecoins on July 7, the calculator shows an estimated net present value of $49.887 per STRC share under the assumptions shown, with a dividend schedule starting at an 11.50% coupon and decreasing to 3.60% after the 33rd month.

The most important thing to note is that the calculation assumes the company remains solvent and will pay dividends forever.

This is not the Strategy’s official valuation and should not be confused with the Strategy’s separate 12.00% STRC dividend disclosure. It’s useful because you can see what preferred stock investors are actually testing. This value is highly sensitive to assumptions regarding dividend durability, discount rates, and whether the issuing company will be able to continue making payments as Bitcoin and capital market conditions change.

Bitcoin’s background makes this test difficult to ignore. According to Bitcoin market data from firememecoins, BTC was trading at around $62,000 as of July 8, down 1.8% in 24 hours but up 5.5% in 7 days, giving it a market cap of $1.24 trillion and control of 58%.

However, Strategy’s June 28 BTC update reported that 847,363 BTC were held at an average purchase price of $75,651. This gap did not force a sell-off, with Strategy magazine reporting that there were no Bitcoin purchases between June 22nd and June 28th. However, this explains why the market is focused on reserve policy, ATM issuance, and BTC monetization language.

The strategy’s ATM table shows how much capital market power is still behind the model. Strategy reported that from June 22nd to June 28th, there were no preferred stock ATM sales and 12,669,017 shares of MSTR stock were sold, resulting in MSTR net income of $1,152.4 million. It also listed remaining issuance capacity of $17,510.8 million for STRC, $24,257.5 million for MSTR, and other priority programs.

The model still has tools. The question is how much those tools will cost if investors demand higher yields, larger discounts, or more visible backstops.

What proves that stress is more widespread?

There are currently two main ways to read the next phase in the market. There are currently two main ways to read the next phase in the market. In a subdued scenario, STRC’s discount strengthens, Strategy’s USD reserves and dividend policy calm the market, BTC sales remain optional rather than mandatory, and Strive’s price drop looks like a temporary blow to a single cross-shareholding. That way the pressure will mostly stay within the trajectory of the strategy.

In a broader stress scenario, discounts continue, dividend rate changes no longer reassure investors, reliance on common stock ATMs increases, BTC monetization moves from authorization to use, and Strive’s own preferred SATA begins trading as an equivalent stress point rather than a separate product. In that case, the priority issue for Bitcoin government bonds will be category trading rather than a single company issue.

The submitted documents do not prove that the second scenario has arrived. They indicate why the question was asked. Strive’s STRC position turned Strategy’s discount into another company’s fair value movement.

Strategy’s framework turned dividends, reserves, buybacks, ATM issuance, and potential BTC sales into a single, consistent support system. Farside’s calculator showed why solvency and perpetual payment assumptions are important to preferred value.

The market tests are now real: whether STRC and SATA close or widen the parity gap, whether dividend coverage looks more reliable, whether Strategy places more emphasis on a common stock issue or a preferred issue, and whether the BTC sale will be more than just an approval.

Strive’s upcoming disclosures will help clarify whether the company’s strategy exposure was an isolated mark or the first public indication that Bitcoin Treasury credit stress is spreading across the preferred stock model.

(Tag Translation)Bitcoin