Congress is moving to modify how U.S. tax law treats crypto mining and staking rewards, and the changes are long overdue for validators and their institutional customers.

HR 9175, the Mining and Staking Tax Clarity Act, would allow miners and stakers to defer taxes until they sell newly minted tokens, ending the cash flow penalty that has pushed validation infrastructure and its largest customers to offshore jurisdictions with clearer rules.

For Bitcoin miners, the bill barely touches on the actual competition that determines where to build the next megawatt, consisting of land availability, power contracts, permitting schedules, grid reliability, and more.

Staking tax issues

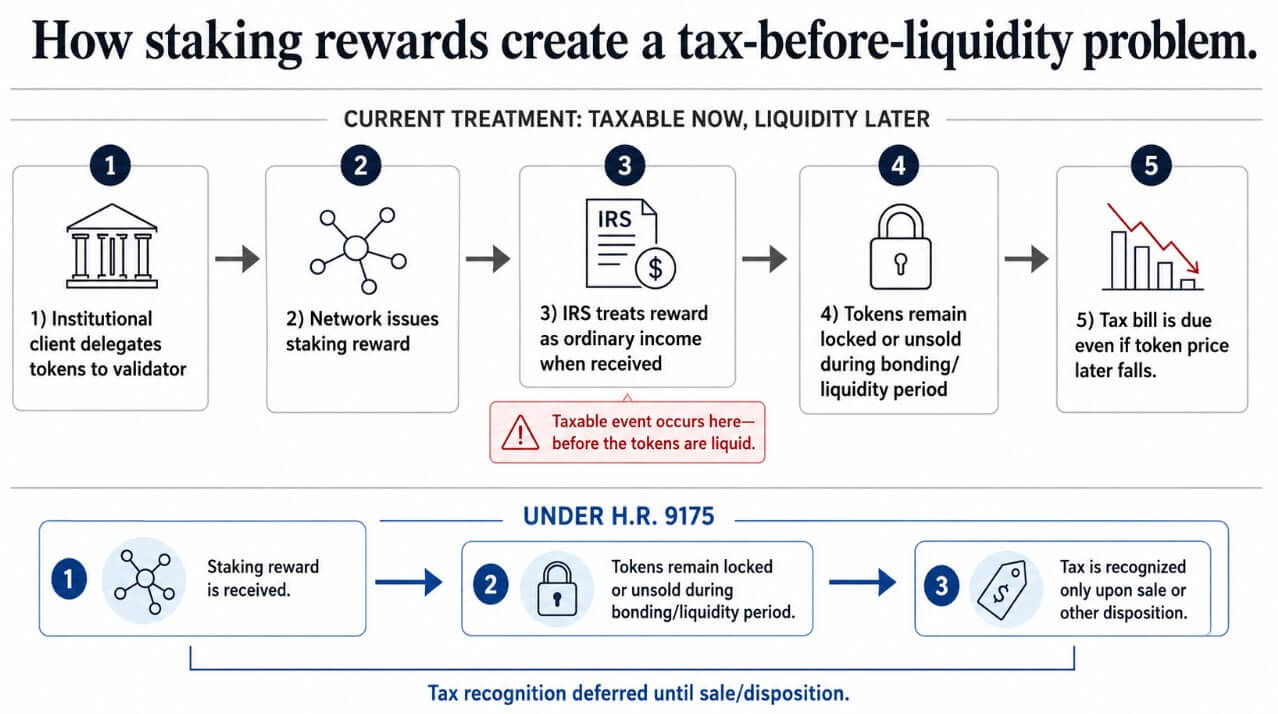

Under IRS Revenue Regulation 2023-14, validators and their clients are liable to pay regular income tax at the price on that day the moment they receive their staking rewards, regardless of whether they sell a single token.

In the staking-as-a-service model, institutional customers delegate their tokens to a validator while locking them up for a guarantee period, so customers are liable to pay cash taxes on assets that cannot yet be liquidated. Infrastructure providers are liable to pay taxes on fees collected from the same illiquid tokens.

Jenny Levin, chief legal and executive officer at the Algorand Foundation and former Staking as a Service operator, calls this a “constant waste of cash,” and every reward on any network must be valued at the time it is received. If the price falls before anyone sells, the liability is already set at a higher number.

On June 4th, the US Tax Court issued its first opinion directly addressing the taxation of staking rewards, further strengthening that position. Pascal v. Commissioner, TC Memo. 2026-2046, the court held that if the taxpayer acquires control and control over the remuneration, the remuneration constitutes gross income under Section 61.

The ruling is unprecedented, and Jarrett v. United States and other pending cases could complicate it further, but it comes just as Congress is deciding whether to legislate a different answer.

HR 9175 gives taxpayers the option to treat newly minted tokens as self-created property and defer recognition until they are disposed of.

The Blockchain Association, Crypto Council for Innovation, and The Digital Chamber support this as a “balanced compromise” that preserves the classification of ordinary income while eliminating the pre-liquidity tax penalty that drives staking infrastructure offshore.

If passed, it would allow institutional investors to build U.S.-based verification businesses without treating every compensation cycle as a potential cash flow crisis. This change is most valuable when the price increases and the phantom tax liability on locked tokens is at its maximum.

Switzerland and Singapore are already moving toward providing more defined treatments, thereby nudging institutional staking business.

Mr. Levin pointed out where the bill’s scope would be.

“This tax bill moves the United States from a punitive position to a viable position. Securities and custody clarity is what makes America competitive.”

The SEC’s Division of Corporate Finance issued a statement in May 2025 noting that certain protocol staking activities do not involve securities offerings, and in January 2025 rescinded SAB 121, which required companies that hold digital assets to record them as liabilities on their balance sheets.

Both moves reduce friction and remain staff-level guidance that a future Commission can overturn without rulemaking, leaving securities classification, custody rules, and licensing as barriers between a viable U.S. verification sector and a truly competitive sector.

Bitcoin mining follows infrastructure

President Donald Trump’s campaign promise of “American-made Bitcoin” has become a reality. Executives are deploying capacity building in locations where power is cheap, land is granted and grid contracts are maintained for 10 years.

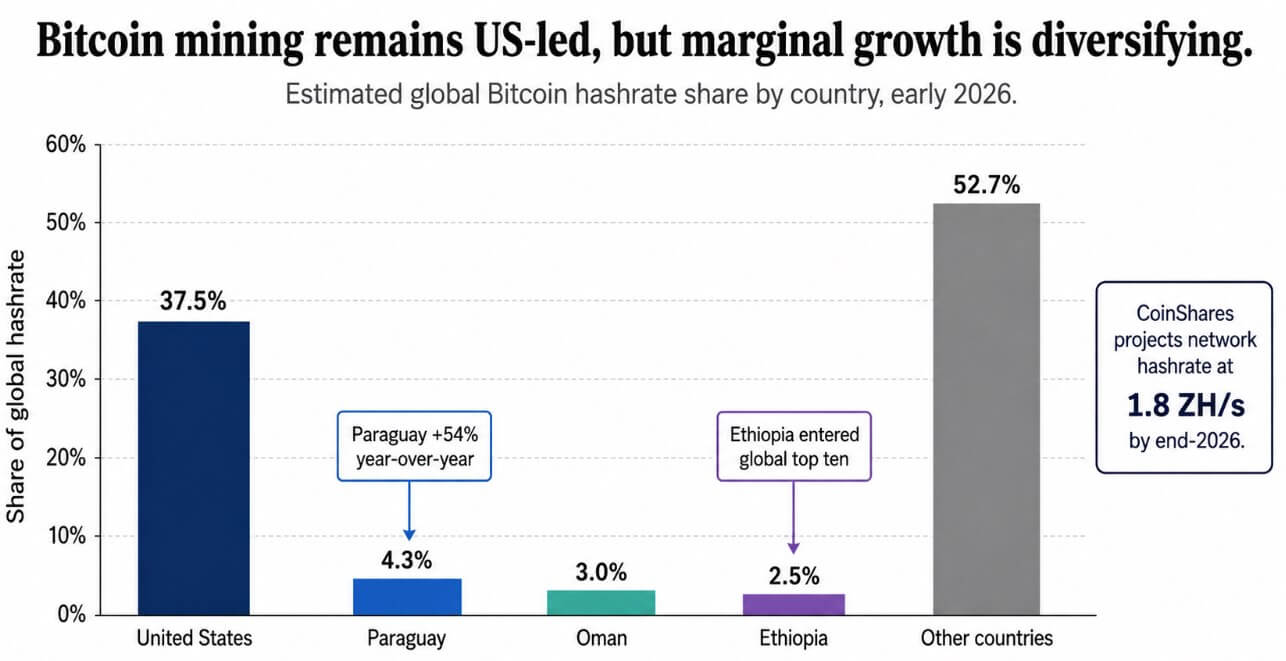

As of January 2026, the United States holds about 37.5% of the world’s Bitcoin hash rate, making it the largest country in the country’s share, while Paraguay has increased by 54% year-on-year to 4.3%, and Ethiopia has risen to 2.5%, ranking 8th in the world. CoinShares predicts that by the end of 2026, the network will reach 1.8 ZH/s, with Paraguay, Ethiopia, and Oman all in the world’s top 10.

HIVE Digital Technologies operates in large capacity in Canada, Sweden, Paraguay and the United States, and CEO Aydin Kilic noted that the first question is whether HIVE owns the land and can run it efficiently on-site, then off-taker demand, and long-term power availability and economics.

Regarding U.S. competitiveness in particular, Kilic pointed to permitting and zoning efficiency, large and reliable power contracts and attractive prices, and long-term grid certainty. At the company’s Iguazu campus in Paraguay, the ANDE power contract reached 300 MW of output because land and utility relationships were already in place.

In Sweden, HIVE has signed a non-binding LOI for a potential lease of the Boden facility for up to 10 years. This will cover 25 MW of critical IT workloads, with a planned refurbishment of 10,000 NVIDIA GB300 GPUs based on a long-term relationship with the country’s energy provider.

Both extensions followed the same logic. First, we secured the power relationships and then decided whether the site would perform Bitcoin mining or high-performance computing.

As Bitcoin has fallen about 50% from its October 2025 peak of around $124,000, hash price fell to an all-time low of $27.89 per PH/s per day in the second quarter, with CoinShares estimating that previous generation equipment running at about $0.05 per kWh was running at negative gross margins.

In Paraguay, Laos, and Finland, operations that combined new hardware and true power cost benefits remained profitable during the downcycle, with hash prices hitting record lows of $27.89 per PH/s per day, and all efficiency benefits delivered significant returns.

FERC’s move to require all six regional grid operators to justify or reform their interconnection rules for large loads, combined with ERCOT’s increased oversight of crypto projects as reliability declines heading into summer 2026, has increased the cost and schedule of new construction in the United States.

two bottlenecks

The pre-liquidity tax mechanism that Mr. Levin describes is a real driver of offshore structuring for institutional investors and the validators that serve them, and Mr. Pascal confirmed that the courts will enforce current law.

Sen. Cynthia Lummis, one of the bill’s most consistent supporters in the Senate, is retiring in January 2027, making the most realistic chance for passage before the August recess.

| infrastructure truck | Major bottlenecks in the US | Changes in HR 9175 | things that don’t get resolved | future implications |

|---|---|---|---|---|

| Staking/Verification | Clarity on tax payment timing, handling of securities, storage rules, and licenses | Defer taxes on newly minted rewards until sale or disposition | Whether staking is treated as a securities activity in any structure. Custody and licensing uncertainty | US-based verification could become more viable, especially for institutional customers |

| bitcoin mining | Power costs, land management, grid access, permits, zoning, operating hours | Tax friction on mined tokens could be reduced | Does not create cheap power, interconnection capacity, permitting, or long-term grid certainty | Miners will continue to diversify into jurisdictions with reliable and scalable power |

| AI/HPC overlap | Competition for receiving sites, substations, transformers and long-term energy contracts | No direct impact | Competition between miners and AI data centers for grid capacity persists | Mining sites with powerful power rights become valuable computing infrastructure |

In the case of Bitcoin mining, tax clarification slightly improves location decisions determined by substations, utility contracts, and permit queues.

President Trump’s “American-made Bitcoin” pledge suggested that the federal government’s intentions could generate the physical infrastructure necessary for such a process. The actual geographic expansion of the mining industry into Paraguay, Northern Europe, East Africa, and the Gulf Coast along U.S. bases provides a realistic answer to that assumption.

(Tag translation) Bitcoin