Bitcoin prices hit $70,000 after Strategy, the world’s largest publicly traded holder of top cryptocurrencies, sold part of its BTC vault for the first time since 2022.

data from crypto slate The price of BTC fell 4% on this news, dropping to $69,690 before rebounding to $70,120 at the time of writing. This is the lowest level in six weeks.

The price change comes after Strategy revealed on June 1 that it had sold 32 Bitcoins between May 26 and May 31. The sale generated approximately $2.5 million at an average execution price of $77,135.

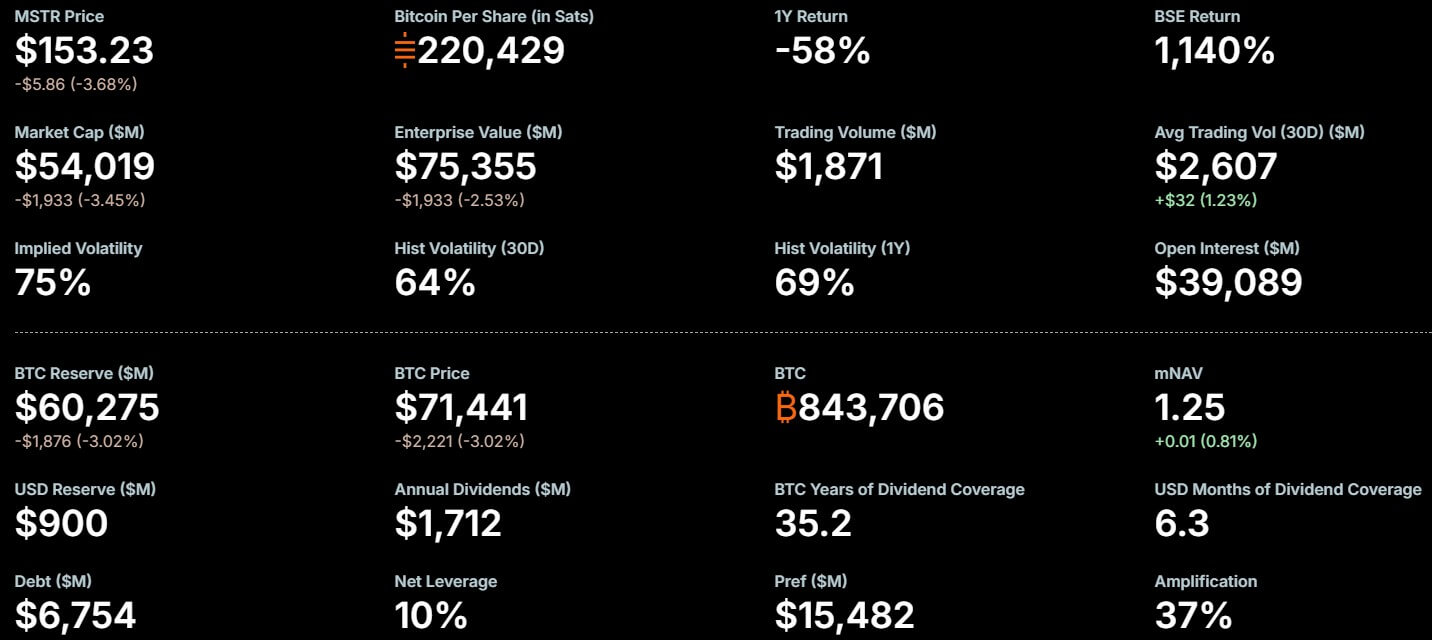

The digital asset sale represented just 0.0038% of total holdings, compared to a total corporate stockpile of 843,706 Bitcoins acquired at an average price of $75,699.

Market participants were quick to emphasize the significance of Strategy’s decision to sell, marking a formal departure from founder Michael Saylor’s long-held policy of absolute retention. Jim Cramer, host of CNBC’s Mad Money, said:

“Strategy (Micro) is selling Bitcoin for $2.5 million. Given how much Strategy has supported Bitcoin, it may need to reevaluate its pro-Bitcoin stance. It’s been an important trampoline for years. Some say it’s manipulation. I think that’s too strong.”

More importantly, the sale highlights potential structural risks as Strategy increases its reliance on volatile assets to fund fixed dollar-denominated corporate debt.

STRC takes strategy deeper into credit markets

According to the filing, Strategy said it sold its BTC holdings “to fund preferred stock distributions.”

Over the past year, Strategy has introduced several publicly traded perpetual preferred stocks, including STRK, STRC, STRF, and STRD, to provide fixed income returns alongside Bitcoin treasury operations.

The most popular among them is STRC, a perpetual preferred stock introduced in July 2025, nicknamed Stretch.

In recent months, security has been central to Saylor’s efforts to transform the company’s Bitcoin holdings from passive reserves into a funding platform that can attract investors looking for yield rather than direct exposure to the token.

Thaler said Strategy wants STRC to become one of the leading credit products in the global market, and that that goal hinges on whether it can remain stable enough to function as an income vehicle rather than a volatile crypto-related stock.

STRC pays cash dividends monthly and currently maintains an annualized dividend rate of 11.5%. This is the level Strategy has maintained for four consecutive months. The rate is reviewed monthly and can be adjusted to bring the stock closer to its $100 par value.

This price anchor is important to the company’s broader financing strategy.

If STRC remains close to par, Strategy can issue additional shares at more favorable terms through market programs, thereby raising funds to purchase more Bitcoin, meet dividend obligations, and manage debt.

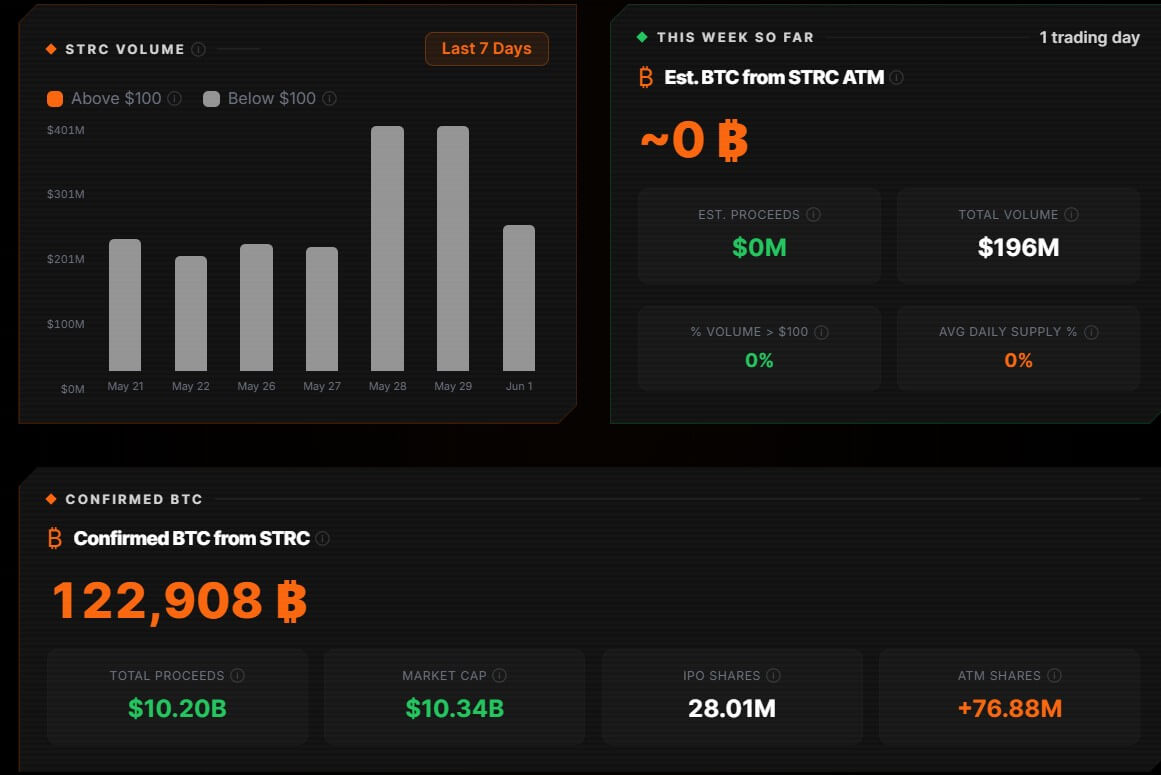

However, this product has been showing some distortion recently. STRC has not traded at par since mid-May, dropping to $97.11 last week before recovering to around $99.10. Still, this product funded purchases of over 122,000 BTC.

Meanwhile, the stock could approach $100 ahead of the June 15 ex-dividend date, when investors must own the stock to receive the next dividend.

This trading pattern draws attention to the mechanics behind Strategy’s new model.

STRC works best when investor demand keeps the security roughly equal. If that support weakens, the company may have to rely more on higher yields, equity issuance, or Bitcoin treasury to keep the structure running smoothly.

The harder question is not whether Bitcoin can be sold.

Strategy and its supporters presented the sale of 32 Bitcoins as a way to show that its treasury is not locked out of the market.

The company maintains that it can sell if it supports its balance sheet, improves its per-share metrics, and helps meet obligations related to its Bitcoin-centered securities issued.

But critics argue that this explanation is only part of the concerns currently surrounding the company.

Glenn Cameron, Global Head of Institutional Investing at OnRamp Bitcoin, noted that Bitcoin’s liquidity was not the biggest question for institutional investors. The asset is continuously traded on exchanges around the world, regularly settling tens of billions of dollars in trading volume every day.

A more difficult question, he said, is whether Strategy can rely on its liquidity during an ongoing drawdown when fixed dollar payments remain due and other funding channels may be less attractive.

He wrote that the company’s model is partially based on the idea that over the long term, Bitcoin would only need to appreciate about 2.3% annually to cover the estimated $1.6 billion in STRC dividends.

He said the calculation is based on the dividend claim on the current notional value of Strategy’s Bitcoin holdings. At today’s prices, it may seem that a small profit to the treasury would be enough to offset the cash costs of the payments.

However, dividends are not paid using mark-to-market gains. I need dollars. This distinction becomes more important when the value of the underlying Treasury falls.

If the price of Bitcoin were to fall in half, the same dividend obligation would consume a larger portion of the company’s asset base.

However, if Strategy continues to issue preferred stock, its cash burden will likely increase. Manageable break-even rates in a rising market can become tighter if bond values shrink and dividend claims are fixed.

This is where the 32 Bitcoin sale becomes more significant than its size would suggest. This transaction is not a test of Strategy’s ability to sell Bitcoin at scale. This was a demonstration of how the Treasury could use the cash obligations associated with the preferred stock structure as they came due.

Economic downturn will narrow strategic options

In a supportive market, Strategy can utilize multiple funding channels simultaneously. Cash can be raised by issuing common stock. Preferred stock may trade near par. Bitcoin sales may be restricted and viewed as selective balance sheet management. Rising Bitcoin prices also strengthen the value of the Treasury underlying its structure.

It becomes difficult to rely on these conditions during a drawdown. As the price of common stock declines, the stock issue becomes more diluted. If STRC prices fall, companies may be forced to offer more yield to restore demand.

On the other hand, dividend payments must still be made in cash, regardless of where Bitcoin is traded.

It’s a scenario that’s drawing scrutiny from analysts. If capital markets remain open, Strategy will be able to meet its obligations without relying heavily on Bitcoin Stack. As market access tightens, the Treasury becomes a more visible source of liquidity.

Selling repeatedly in declining markets comes with its own risks. As Bitcoin’s price falls, more coins will be needed to meet the same dollar obligation, while each sale could deepen investors’ concerns that the preferred stock structure is starting to eat into their underlying assets.

Jeff Dorman, Arca’s chief investment officer, argued that this small sale could be preparing investors for a larger sale later.

He also warned that Strategy’s $900 million cash reserves would only cover about five months of dividend obligations, putting its preferred stock structure at further risk if it became difficult to issue.

Dorman described the setup as a “ticking time bomb” and said the interests of common shareholders, preferred holders, and Bitcoin investors aren’t necessarily aligned when fixed cash payments are piled up on a volatile Treasury.

Meanwhile, the tension extends beyond strategy. Public Bitcoin treasury companies are no longer just holders of reserve assets.

Issuing high-yield securities and relying on traditional capital markets creates obligations to shareholders and capital providers that can complicate pure hold-through volatility strategies.

Bitcoin analyst Simon Dixon said investors should recognize that managers of public finance companies are now operating within a broader financial structure. he said:

“Those interested in Bitcoin should understand who Adam, Saylor, and the others running Bitcoin Treasury companies are ultimately working for at this point, and adjust their expectations accordingly.”

This strategy has turned Bitcoin into the base layer of corporate credit strategies. The question now is how that structure will behave if the market no longer provides the conditions that make it work: rising Bitcoin prices, steady investor demand, and open access to new capital.

(Tag translation) Bitcoin