Kalsi’s US-regulated live crypto perpetual futures move the story from the approval stage to the order book.

The company’s public perpetual futures page and individual product pages present the US-regulated cryptocurrency PERP as a broader trading category that goes beyond the initial Bitcoin experiment.

Kalsi’s own documentation points to markets spanning Bitcoin, Ethereum, Solana, XRP, and other crypto assets, and a dedicated HYPE permanent page shows the company has extended this product to one of the assets most closely associated with the demand for crypto-native derivatives.

Launching changes the test from allowed to working. Traders compare spreads, depth, funding, reference prices, collateral workflows, fees, APIs, leverage, and whether market makers continue to quote as volatility increases.

Bitcoin enters this test with a clear advantage as it has the deepest spot footprint and the most familiar benchmarking infrastructure. Altcoin markets can become relevant, but each market needs to earn its place one order book at a time.

Approval begins market testing

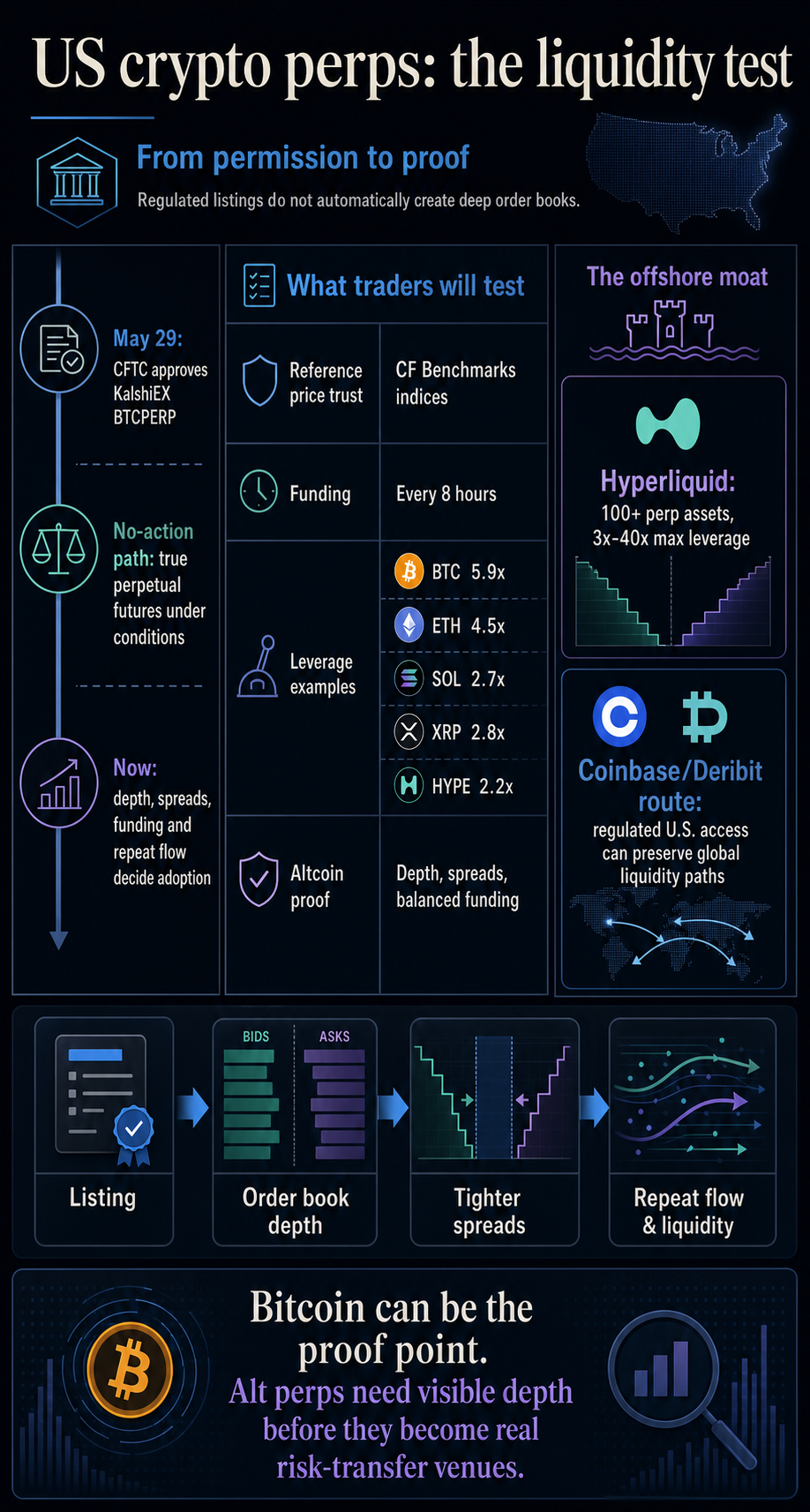

Legal opening is realistic. Adoption is another matter. On May 29, the CFTC approved KalshiEX’s BTCPERP contract as a futures contract that references the spot price of Bitcoin.

The agency subsequently issued additional no-action context for designated contract markets converting certain existing digital product perpetual-style futures into true perpetual futures, subject to customer protection and procedural conditions.

This regulatory path enables the product. No counterparty, market maker, or execution quality performance during volatile sessions is provided.

Calci’s product dynamics demonstrate why fluidity is difficult to obtain. According to the explainer, funding occurs every eight hours, and leverage examples on June 3rd varied widely by asset, with Bitcoin at 5.9x, Ethereum at 4.5x, Solana at 2.7x, XRP at 2.8x, and HYPE at 2.2x.

According to the company’s help center, all of Karshi’s crypto criminals use the CF Benchmark Index for reference pricing for funding and settlement, and Bitcoin is tied to the Bitcoin Real-Time Index.

These mechanisms set the conditions for recruitment. Reference prices impact funding and clearing confidence. Leverage limits determine the type of traders a product attracts.

Minimum order size influences whether a market feels easy to use for small active traders or primarily for large positions. For non-BTC contracts, their details are included in the initial liquidity screen.

The real market requires tight spreads, durable double-sided books, and sustained volume long after the attention of the launch fades. They should also exhibit orderly fundraising behavior even when sentiment is heavily tilted either long or short.

These enforcement signals now carry more weight than another complete legal summary. Small frictions can quickly determine whether an active trader returns or not.

Details of the legal battle, including the initial approval process and the challenge to CME, have already been detailed. Market action will determine the next step. Where thickness builds, where spreads tighten, and where active traders continue to return.

Bitcoin has the clearest path to details

Bitcoin is the easiest asset for regulated US criminals to organize. firememecoins’s Bitcoin market data showed much larger 24-hour spot trading volumes than the major alternative assets within the company’s market set, while its broader cryptocurrency market page showed Bitcoin’s overwhelming share.

While these numbers are in the context of the broader spot market, rather than the trading volume of Karshi venues, they do explain why Bitcoin is a natural first anchor for regulated venues.

Perp contracts rely on more than symbols. There needs to be a reference price that traders trust, enough spot liquidity for arbitrage and hedging, and enough flows on both sides to prevent funds from becoming one-sided.

Based on the available evidence, Bitcoin is in the best position as it has the largest market share and the clearest institutional benchmarking background.

The same logic raises the bar for altcoin adoption. Ethereum, Solana, XRP, and HYPE can be listed, and Kalshi’s materials support a wide set of assets across the help center, commentary, and product pages.

Tryouts begin when you list an alternative market. Sustained depth, spread quality, and balanced funding will determine whether it becomes a primary risk transfer venue.

Each alternative market has different burdens. Although Ethereum has a deeper market infrastructure than most crypto assets, it still competes with established offshore and crypto-native derivatives exchanges.

Solana and XRP have a large profile in the spot market, but their PERP liquidity depends on whether professional traders see enough consistent depth to justify routing flows.

HYPE is more unusual as its token is closely tied to the Hyperliquid ecosystem, and its proprietary documentation describes an extensive range of PERP assets and leverage beyond Kalshi’s date-stamped examples.

HYPE provides Karshi with timely assets that are directly tied to the derivatives story. It also highlights the issue of competition. Hyperliquid’s documented Perp Surface provides traders with familiar crypto-native benchmarks for asset coverage and leverage.

Venue customs are a noteworthy inference, but actual transition to Karshi still requires data of visible depth and breadth.

Offshore venues still have trader habits

The global PERP market is already large and deeply familiar. CoinGecko’s 2026 Perpetual Trading Report frames the cryptocurrency PERP as a large global derivatives category, with centralized exchanges still accounting for the majority of open interest.

Hyperliquid’s proprietary materials list more than 100 permanent assets and maximum leverages of 3x to 40x, giving crypto-native traders a broader and more aggressive product profile than early US-regulated examples.

Offshore and crypto-native venues still pose potential challenges. U.S. regulated shipping lanes have a clearer compliance story for traders who want land access, which could have important implications.

The competition has now shifted to execution quality, product coverage, collateral workflow, APIs, fees, and whether market makers see enough repeat flow to actively quote.

Coinbase adds new issues. The CFTC’s May 29 interpretation and no-action position against Coinbase Financial Markets concerned access to Deribit products through regulated U.S. futures traders.

Coinbase’s own announcement describes the route as a way for US customers to access the power and options of the world’s cryptocurrencies without offshore workarounds.

This route could preserve some of the existing global liquidity patterns, rather than forcing all new US demand onto the domestic order book. This arrangement confirms the meaning of the access path without proving the actual flow movement.

Regulated access may mean a new domestic listing venue or a regulated gateway to products connected to existing global derivatives infrastructure.

For traders, this choice will become a reality. Compare spreads, depth, funding history, fees, available leverage, collateral mechanics, order types, reliability, and asset coverage.

If Kalsi’s Bitcoin PERP becomes easier to trade with low friction and reliable two-sided liquidity, Bitcoin could become the proof of a regulated US cryptocurrency PERP. If alt markets remain thin or transaction costs are high, a broader board may act more like option coverage than an actual liquidity transition.

Tests are measurable. We will be watching to see if Bitcoin continues to dominate the volume mix even as more assets emerge. We will be watching to see if HYPE, SOL, and XRP spreads can remain competitive during volatile sessions.

It will be interesting to see if the funding stays in order or if taxes start to fall on one side of the crowd. It will be interesting to see if market makers continue to quote non-Bitcoin prices even after the launch incentive wears off. And watch to see if traders take advantage of this trading venue when volatility spikes. Because that’s when you’ll face the real test of your liquidity claim.

Criminals subject to U.S. regulations now have access to permits they previously lacked. The market still needs to see if they can become a habit. For now, this evidence supports Bitcoin First’s hypothesis that the alternative currency purp is an actual listing, but durable non-BTC liquidity centers still require proof.

(Tag translation) Bitcoin