Just as Bitcoin enters one of the year’s most important macro tests, the old “Sell in May” warning is losing its validity.

While US stocks have endured repeatedly from May to October, Bitcoin’s next move will depend on whether inflation, employment, and Fed signals sustain risk appetite.

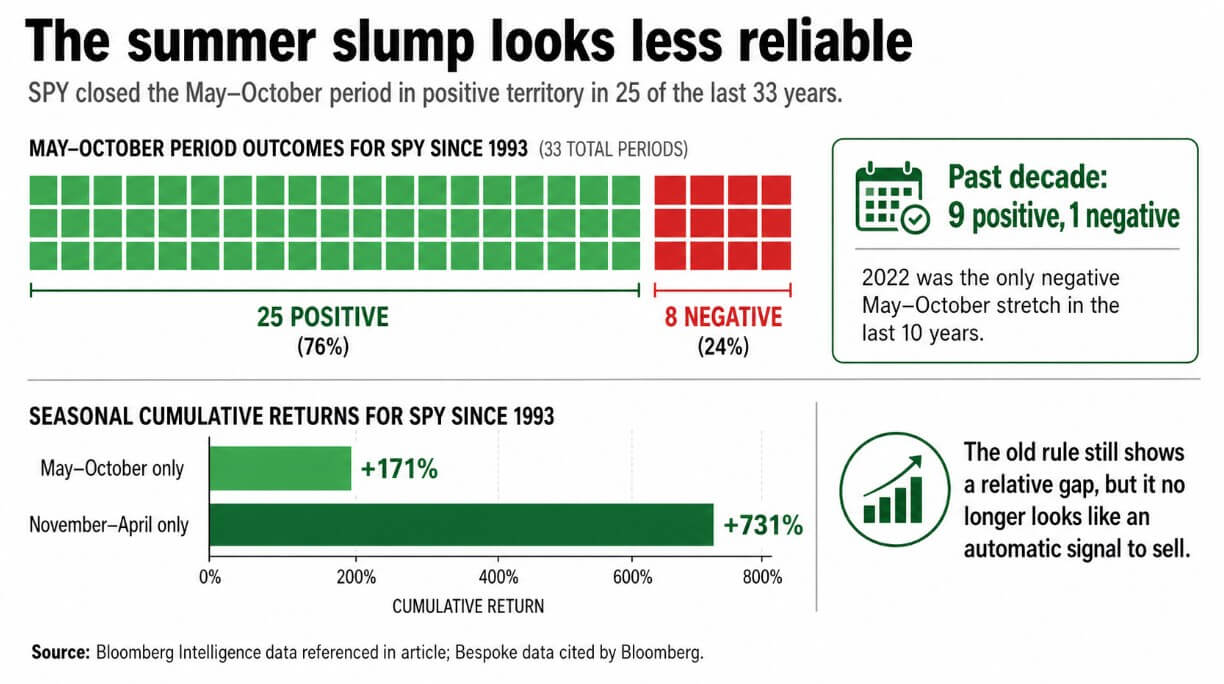

The S&P 500 ETF has finished in positive territory from May through October in 25 of the past 33 years, and has had just one negative summer period over the past 10 years, according to data from Bloomberg Intelligence.

According to custom data cited by Bloomberg, the cumulative return for owning SPY since the ETF’s debut in 1993 has been about 171% from May to October alone. This is a substantial amount and is only significantly less than the 731% I earned on my extended stay from November to April alone.

Despite seasonal differences in performance, the cliché that May automatically means a sell doesn’t hold true.

Rules that may no longer work

The logic behind this old adage is that corporate earnings are weak, trading desks are stretched thin, and investors turn to cash or bonds until the fall.

This strategy has worked well for decades and was built for a market where institutional money moves slowly and risk appetite follows a predictable rhythm.

Bitcoin has spent two years plumbing traditional portfolio flows directly. According to data from Pharcyde Investors, the US Bitcoin Spot ETF received approximately $1.5 billion in inflows from April 17 to April 24, bringing cumulative net inflows to approximately $58.3 billion.

This market structure puts Bitcoin into the same risk appetite mechanisms that drive stocks, giving it direct exposure to things that make institutional investors want to own it.

If institutional capital does not reflexively avoid risk heading into the summer, BTC could avoid one of the psychological headwinds that historically hit speculative assets in May.

The Fed’s own research shows that the bid-ask spreads of crypto ETPs are roughly equivalent to the spreads of similarly sized equity ETFs and ETPs, arguing that the NAV premium of crypto funds should be monitored as a measure of how interconnected crypto and equity markets are.

Bitcoin May Settings

Whether Bitcoin has a summer with fewer headwinds will depend almost entirely on what the next six weeks of data bring.

Policy decisions were made at the Fed meeting held from April 28th to 29th, and on April 29th, Fed Chairman Jerome Powell held a press conference. The Bureau of Economic Analysis will release first quarter GDP and March PCE on April 30th.

The April employment report will be released on May 8th, the April CPI will be released on May 12th, the FOMC minutes from the April meeting will be released on May 20th, and the next full Fed meeting will be held on June 16th-17th.

| date | event | Latest reading/setup in article | Why does the market care? | BTC read through |

|---|---|---|---|---|

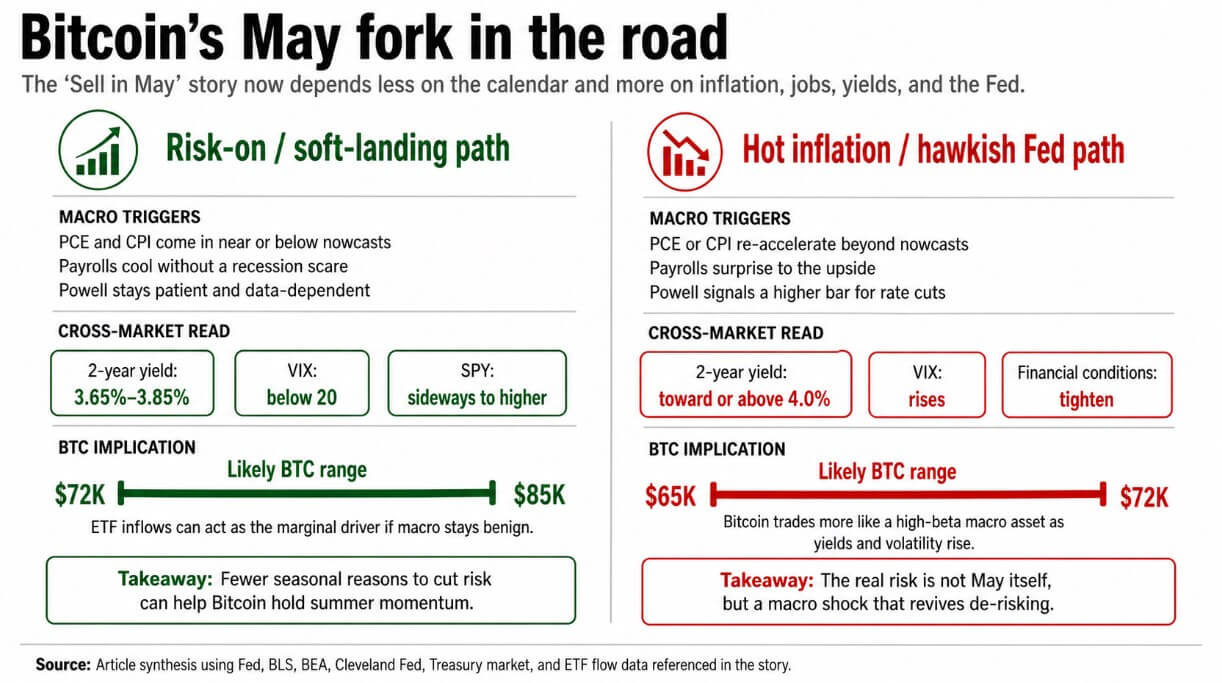

| April 28th-29th | Fed meeting + Powell press conference | Fed will remain stalled unless data forces a shift | Interest rates, liquidity, and how hard the Fed pushes back on rate cut expectations set the tone | Patient and data-dependent Fed supports risk appetite and helps Bitcoin avoid seasonal risk aversion narrative |

| April 30th | Q1 GDP + March PCE | GDPNow estimates first-quarter growth at 1.2% as of April 21st. PCE for February was 2.8% and core PCE was 3.0%. | Shows whether growth is slowing cleanly or sliding toward stagflation, and whether inflation has cooled enough to sustain expectations of easing. | Moderate but stable growth with subdued inflation is constructive for BTC. Slowing economic growth and persistent inflation are problems |

| May 8th | April payroll calculation | Labor market remained strong enough in March to make Fed cautious | If the employment situation improves, expectations for interest rate cuts can be maintained. Hot printing may improve yields | Cooling labor data without fear of recession is bullish for BTC. Reacceleration of hiring could weigh on BTC through rising yields |

| May 12th | April consumer price index | March CPI was 3.3% year-on-year, and core CPI was 2.6%. The April CPI nowcast released by the Cleveland Fed was 3.56% year over year. | CPI is the cleanest short-term test to determine whether inflation is accelerating again | A softer print helps the risk-on case for BTC. High-profile print publications can revive “May Cell” through tight financial conditions |

| May 20th | FOMC Minutes | Markets want details on how concerned officials were about inflation and interest rate cuts | Minutes can either strengthen or soften the message of Powell’s press conference | BTC could trade like a high-beta macro asset if minutes indicate a high bar for rate cuts |

| June 16th-17th | Next Fed General Meeting | By then, the market will have GDP, PCE, salaries, CPI, and April minutes released. | This is the point where the May data run will confirm or break the summer risk-on theory. | If the macros remain favorable, BTC can maintain a range between $72,000 and $85,000 within this window. If inflation and yields rise, the downside to $65,000-$72,000 becomes more realistic. |

This sequence of events either confirms that “Sell in May” has lost its macro basis, or this time it will be rebuilt.

The Atlanta Fed’s GDPNow, as of April 21, puts the growth rate in the first quarter at 1.2%, while the official GDP for the fourth quarter of 2025 is 0.7%.

The CPI in March was 3.3% year-on-year, the core CPI was 2.6%, and the energy index rose 10.9% month-on-month. PCE for February was 2.8% and core PCE was 3.0%.

According to the Cleveland Fed’s nowcast as of April 28, April CPI was 3.56% year-on-year, and April PCE was 3.60%. The March Fed SEP raised both median 2026 PCE and core PCE to 2.7%, with 17 out of 19 participants marking inflation risks as skewed to the upside.

As of late April, the cross-market situation was under control. The 2-year government bond yield was 3.78%, the 10-year government bond yield was 4.31%, the VIX was 18.02, and BTC was in the $76,000 zone.

BlackRock’s Spring Outlook frames the current settings as a trade-off for benign stagflation, with the Fed remaining on pause and moving to gradual easing only if inflation continues to slow or growth remains moderate.

If April PCE and May CPI remain close to or weaker than current nowcasts, and April payrolls cool without triggering recession concerns, the Fed could certainly continue relying on the data.

This would lock the two-year bond yield into a range of approximately 3.65% to 3.85%, keep the VIX below 20, and keep the SPY flat to high. In this context, ETF inflows will be the marginal driver for Bitcoin.

Institutional allocators who have built Bitcoin positions through IBIT or peer funds have no clear seasonal reason to reduce their exposure.

Bitcoin could remain in the $72,000 to $85,000 range until the June Fed window. If core inflation turns out to be softer than feared, while the growth data remains unconcerned and the employment data is nicely underperformed, markets could re-price in a clearer easing path for the second half of 2025.

The markets in which SPY was positive in 25 of the 33 periods from May to October are markets where the basis for action to reduce risk in the summer is weakening year by year.

Inflation brings back “sell-in-may”

Treasury yields will rise if PCE and CPI reaccelerate above their nowcasts, if April payrolls show unexpected upside, or if Chairman Powell makes it clear in his April 29 press conference that the hurdles for cuts are higher than the market expects.

If the two-year bond yield rises above 4%, financial conditions will tighten, equity multiples will be compressed, and the liquidity background that supported Bitcoin’s rise in the ETF era will disappear.

In that environment, BTC trades as a high-beta macro asset. A pullback to the $65,000 to $72,000 range is likely, driven down by the same risk appetite that has been pushing it higher.

According to the Philadelphia Fed’s Concern Index, the first quarter survey showed that the probability of GDP decline in the second quarter was 20.9%, a level high enough to keep recession risk as a tail risk.

If GDP declines unexpectedly while inflation remains low, the Fed will be stuck in classic stagflation, where neither rate cuts nor rate hikes can solve the problem. That stagflation bind is actually the biting version.

Bitcoin absorbed Wall Street’s infrastructure and inherited its constraints along with its capital. Seasonal lore has always represented the idea that summer is a time when macro imbalances are priced in, liquidity thins, and investors reconsider what they want to own.

The next six weeks will test whether the macro regime that drove Bitcoin to all-time highs can weather the inflation data.

The next test is a direct one. If inflation subsides and yields remain subdued, Bitcoin may continue to treat May as a macro checkpoint rather than a sell signal. If the CPI, PCE, or jobs report forces the Fed to return to a more aggressive stance, seasonal warnings will return through tightening financial conditions and BTC’s ETF-era support will be tested through the June meeting.

(Tag translation) Bitcoin