Banks are increasingly turning to tokenized deposits as they embrace blockchain technology to improve the way money moves through the financial system. A new report from Arcam Intelligence says regulated banks are creating digital versions of customer deposits that operate on blockchain networks but remain on the bank’s balance sheet.

This transition will allow banks to automate transactions faster and without disrupting the essential architecture of traditional banking. In contrast to stablecoins, tokenized deposits remain bank liabilities and are regulated according to banking regulations.

What tokenized deposits actually do

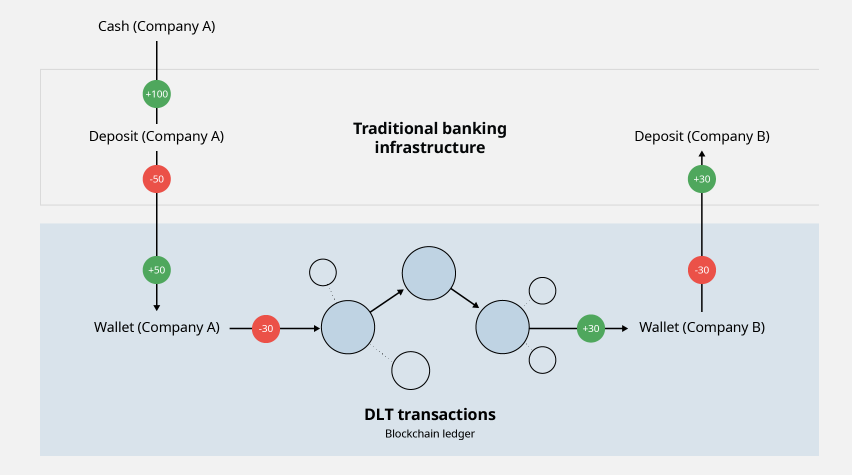

Tokenized deposits are a digital version of bank deposits that run on a blockchain network. The deposit remains with the regulated bank, but the customer receives a digital token representing the same value. This allows banks and businesses to move funds more quickly than traditional payment systems, which rely on bank business hours and often take longer to settle transactions.

The technology also allows banks to automate payments based on pre-agreed terms. For example, companies can move funds between subsidiaries at any time or automatically release payments after invoices are approved or liquidity targets are reached.

In September 2025, HSBC completed the first cross-border tokenized deposit transaction between Hong Kong and Singapore for Ant International, demonstrating how the technology works. The transaction reduces delays caused by time zone differences and allows the company to manage its financial operations more efficiently.

Why is it different from stable coins?

Tokenized deposits are often compared to stablecoins because they use blockchain technology to move digital money. However, according to Arkham Intelligence, the two work in very different ways.

Stablecoins such as USDT and USDC are issued by private companies that back their tokens with reserve assets. According to data from rwa.xyz, the outstanding amount of USD-denominated stablecoins to date is expected to reach nearly $300 billion by mid-2026.

In contrast, tokenized deposits are issued by regulated banks and represent customer deposits that those institutions already hold. It is also only available to authorized clients through permissioned blockchain networks.

A February 2026 report by the New York Fed highlighted that stablecoins are intended to serve as “safe money,” while tokenized deposits become part of the traditional banking system and are useful for bank lending.

Major banks drive industry adoption

A major global financial institution has launched a tokenized deposit system as it continues to adopt blockchain technology. Some of the industry’s biggest players include JPMorgan through its Kinexys system, formerly known as Onyx. Kinexys systems have executed more than $7 billion in transactions every day since its inception, with more than $3 trillion processed.

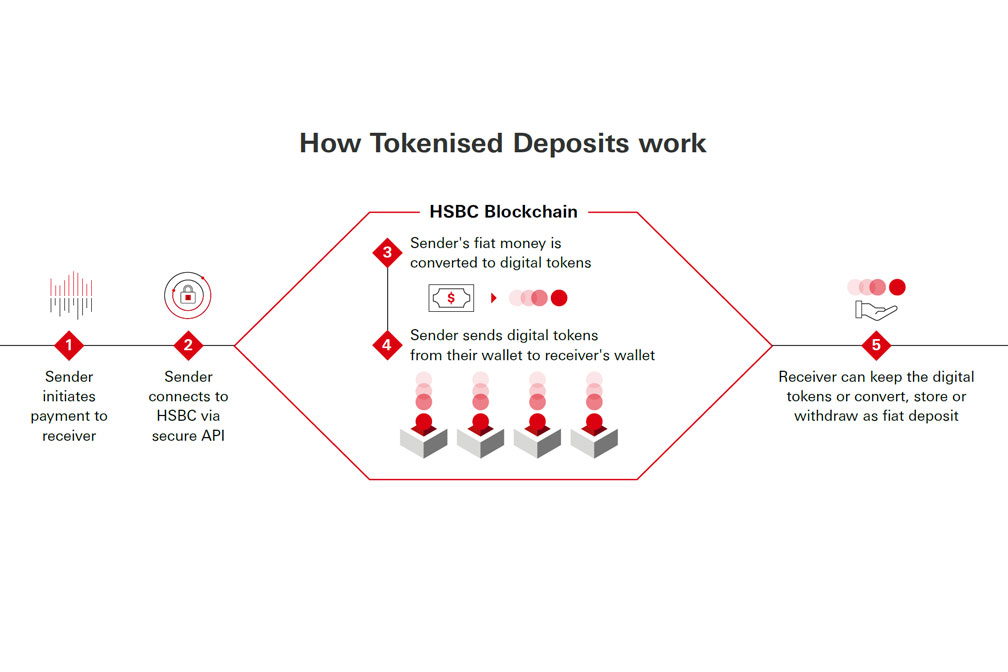

HSBC has expanded its tokenized deposits to Hong Kong, Singapore, UK, Luxembourg, and US territories. The system supports a variety of currencies and enables automated payments and settlement of tokenized deposits.

Another player that joined the industry in January 2026 was BNY Mellon, which launched a tokenized deposit product targeting institutions. We have also invested in blockchain infrastructure while taking on projects related to tokenized money market funds.

Challenges that still require solutions

Despite the growing popularity of tokenized deposits, the technology faces several hurdles. Currently, the platform runs within the ecosystem of one bank, and tokenized deposits cannot be transferred from one financial institution to another without leaving the system. To solve this problem, the clearinghouse plans to introduce a common network for tokenized deposits by the first half of 2027.

The International Monetary Fund said the impact of tokenization is likely to extend far beyond payments. Tobias Adrian, director of the IMF’s Department of Financial and Capital Markets, said future policy decisions will determine whether tokenization makes the financial system more efficient or creates new fragmentation.

related: $60 billion tokenized RWA market shows no on-chain activity, report finds