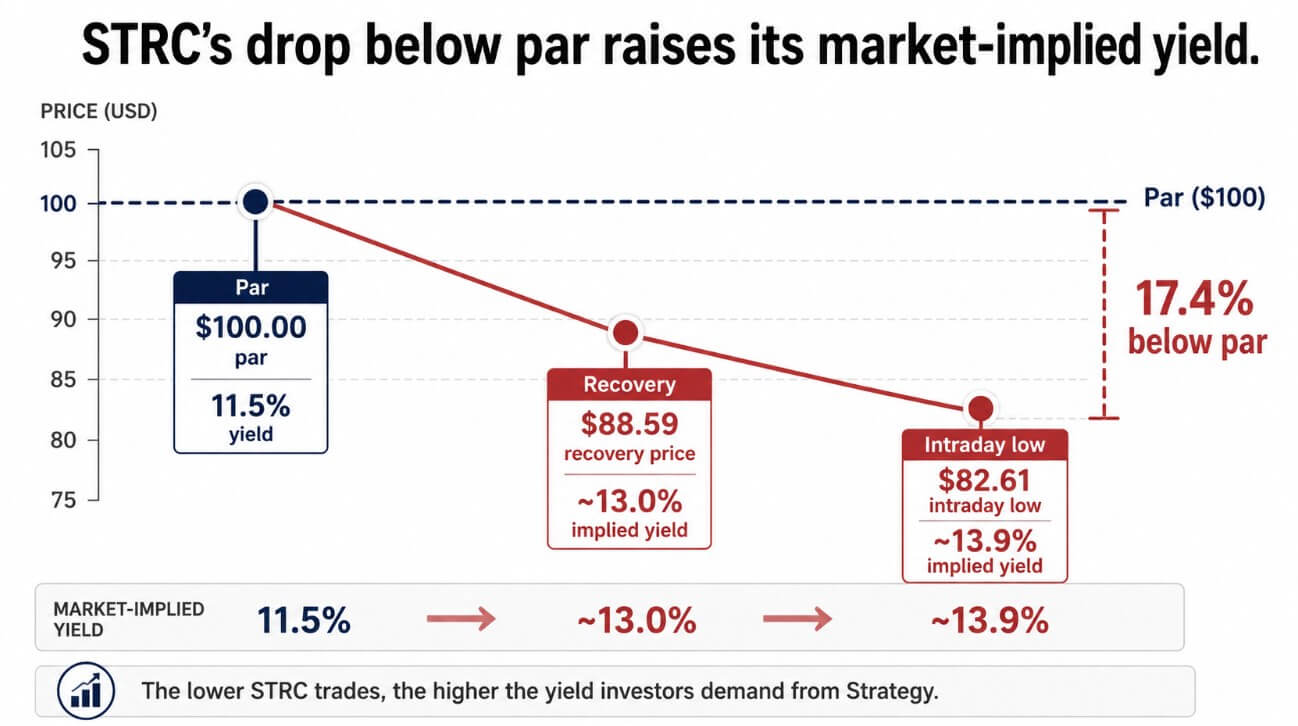

STRC, Strategy Inc.’s perpetual preferred stock, traded as low as $82.61 on June 18, before recovering to $88.59, nearly 17% below the $100 price established at that day’s low.

During the same session, MSTR fell 3.4% to $112.53, while Bitcoin fell about 2.5% to trade around $62,730.

The strategy is designed for STRC to hover around $100 through monthly dividend rate adjustments, currently set at 11.50% per annum, paid semi-annually in cash.

At $88.59, its 11.5% coupon means the real yield is about 13.0%, and the divergence between stated interest rates and market demand shows how much confidence has fallen.

Since STRC has a notional principal balance of approximately $10.5 billion, assuming an annual interest rate of 11.5%, the dividend cost for STRC alone would be approximately $1.21 billion.

If the market continues to price the company below par and Strategy responds by raising its tax rate to 14%, costs would rise to about $1.47 billion a year, a move critics have been warning about for months.

that the criticism was correct

The Ponzi-like characterization of STRC has been widely circulated, with Peter Schiff calling it “the most obvious Ponzi” and insisting that new capital funding payments would go to existing holders.

Strategy’s filing describes STRC as a perpetual preferred stock with disclosed risks and a discretionary dividend structure. The company has no legal obligation to keep STRC near $100, and its prospectus warns that raising the dividend may not restore the price if STRC trades below par.

Tyler Wellener, CSO at Tyr Capital, commented on the structural issues in a memo:

“Capital structures have become more complex over the past year, and the market is worried about being able to satisfy everyone and meet obligations.”

He added that STRC is not actually backed or collateralized by Bitcoin, so it is a trust game in management. The 2.5% Bitcoin drawdown resulted in STRC’s intraday volatility of 17%, as STRC’s stability relies on continued confidence in Saylor’s capital allocation.

Ryan Haczynski, Head of Protocol Partnerships at GlobalStake, identifies a second catalyst. On-chain STRC derivatives and tokenized equity products were buying and tokenizing stocks, while large participants were building large short positions.

STRC had been trading close to par for months, so investors treated it as low-volatility carry and added leverage to increase yield.

Margin calls triggered a series of liquidations as prices fell below key levels, amplifying the move.

Haczynski also notes that Saylor recently acknowledged that ChatGPT played a role in the development of the STRC structure, a detail that added to selling pressure as the clip circulated as prices fell.

Why selling Bitcoin won’t solve the problem

Strategy revealed that it sold 32 BTC for $2.5 million between May 26th and May 31st, and the proceeds will be used to distribute preferred stock.

The company subsequently purchased 1,550 BTC for $101.3 million, bringing its total holdings to 845,256 BTC as of June 7, and raised its USD reserves to $1 billion.

Although the sale of 32 BTC was financially insignificant, at current rates about 1/482nd of STRC’s one-year dividend, it cracked the narrative that Saylor would never sell.

Mr. Wenner responded to a question regarding the sale of BTC as follows:

“Selling BTC would weaken the balance sheet and disrupt the market, as large BTC holders may seek to sell BTC to de-risk, and common stock holders may realize they are better off holding BTC directly or buying either an ETF.”

MSTR shareholders bought shares to accumulate Bitcoin per share, while STRC shareholders bought shares for yield. Selling Bitcoin for dividends will only appease one constituency, alarm the other, and do nothing to address whether Strategy can generate yield without continually refinancing with new capital.

Hudzinski said Strategy’s next move could be a combination of a higher dividend rate, an opportunistic buyback of STRC stock at a discount, or raising additional capital using MSTR or traditional debt.

Raising the dividend would increase the annual cost and give impetus to critics who warn of feedback loops. MSTR issuance preserves the Bitcoin stack, but dilutes common shareholders and reduces BTC per share growth, the central metric that MSTR buyers care about.

Share buybacks would be the strongest signal of confidence, as buying back STRC at a deep discount and reissuing it closer to par could benefit MSTR shareholders, but it would also consume cash that would otherwise be used for dividends or Bitcoin purchases.

| rescue options | How STRC can help | trade off | who will take the pain |

|---|---|---|---|

| Increase STRC dividend | Reduce the gap between prescribed dividends and market yields | Annual cash burden increases, raising concerns about feedback loops | strategic balance sheet |

| sell bitcoin | Provides cash for priority distribution | Weakening the “never sell” accumulation narrative | MSTR Holder / BTC Bull |

| Issue MSTR shares | Maintain your Bitcoin holdings while raising cash | Dilution of common shareholders and increase in BTC per share | MSTR holder |

| Buy back STRC | Show confidence and earn discounts worth your face value | Use cash that can fund dividends and BTC purchases | Strategy fluidity |

| Let STRC reset the price | Avoid putting money into market support | Acknowledging that STRC could be traded like a distressed Bitcoin credit | STRC holder/reputation |

Wellener shared what it takes for a reliable fix:

“The strategy’s ability to right the ship will depend on whether it can convince the market that it can generate more BTC per share without resorting to stock issuance or financial engineering.”

He added that going beyond buy-and-hold and using derivatives for yield generation, as commodity companies have done for two decades, could provide a path to real yields that is not dependent on access to capital markets or rising Bitcoin prices.

What will the next market price be?

STRC could recover toward the $95-$100 range if the strategy announces share buybacks, increases its USD reserves, or outlines a reliable derivatives-based yield strategy.

Hudzinski described the move as a liquidity unwind. As of June 7, the company held $1 billion in reserves for about a quarter of STRC’s $1.21 billion quarterly dividend obligation.

A properly structured share buyback at current prices would lead to accretion and demonstrate that the $100 par target is more than a marketing claim.

If STRC remains below $90 and the market starts pricing in a 14% effective yield as the new threshold, the feedback loop described by critics will become self-reinforcing.

Raising the dividend increases the cash burden without restoring par, issuing MSTR to fund the hike dilutes the value for public holders, and selling Bitcoin to make up for the shortfall undermines the accumulation theory.

This product will be repriced as a distressed Bitcoin credit due to investor expectations, differences in buyer demographics, and much higher hurdles to restoring confidence.

| scenario | trigger | Impact of STRC | Broader market impact |

|---|---|---|---|

| repairing confidence | Share buybacks, increased US dollar reserves, and a reliable yield strategy | STRC retreats towards $95-100 | Markets treat sharp declines as liquidity events |

| Controlled repricing | STRC is stable below par value, but the reliability of the dividend is still high | STRC trades as a high-yield Bitcoin-linked preferred stock | Investors demand higher fees but avoid panic |

| yield spiral | STRC stays below $90, Strategy raises dividend repeatedly | Cash burden increases without par value recovery | Criticism of the structure intensifies |

| BTC sell-off rebound | Strategy sells more Bitcoin to raise dividends | STRC may receive payment support, but MSTR will be weakened | The story of accumulation is further broken. |

| Sector repricing | Investors have widespread doubts about Bitcoin-based yield products | STRC is a case that requires attention. | Future BTC government bond products face higher collateral and yield scrutiny |

The broader implications extend beyond strategy, as a Bitcoin-based yield product becomes the first credit product to be stress-tested on a large scale.

If STRC cannot maintain parity with its 11.5% dividend, $10.4 billion in notional value, and 845,256 Bitcoins on its balance sheet, the next generation of Bitcoin government bond products will face more difficult questions about collateral structure, yield sustainability, and the implications of offering yield backed by non-yielding assets.

(Tag Translation)Bitcoin