Strategy (formerly MicroStrategy) last week sold common stock to raise $335.5 million and moved nearly 90% of its proceeds into cash rather than Bitcoin as it moved to shore up its preferred securities that fund crypto purchases.

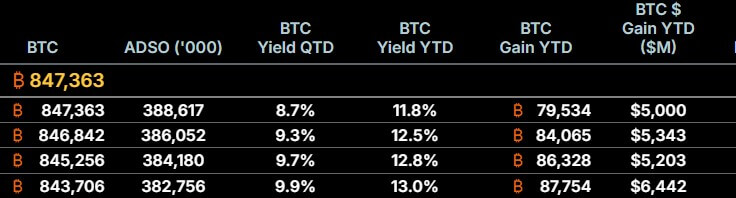

The company sold approximately 2.71 million MSTR shares between June 15 and June 21, adding $300 million to its U.S. dollar reserves and raising the fund to $1.4 billion. The remaining $34.9 million was spent on 520 Bitcoins.

The assignment was made after Strategy’s STRC Perpetual Preferred Stock fell sharply, dropping to an intraday low of $82.50. STRC is designed to trade around the official price of $100, making it one of the most important sources of funding for the company’s Bitcoin purchases.

Strategy relied entirely on its over-the-counter common stock program this week and did not sell any preferred stock. The move diluted MSTR shareholders, but made more cash available to cover dividends and interest across the company’s expanding capital structure.

Will MSTR common stock become a backstop for STRC?

This financing decision demonstrated how Strategy could leverage its common stock if demand for its preferred securities weakened.

STRC has an outstanding nominal value of approximately $10.5 billion and pays an annual dividend of 11.5%. Strategy typically sells new STRC shares when they trade above $100 and uses the proceeds to buy Bitcoin and meet other corporate needs.

Since STRC fell below the specified value, the channel was effectively closed. Selling the additional shares at a discount results in less cash, while adding to the dividend obligation calculated on the full $100.

Instead, Strategy issued MSTRs and used most of the proceeds to increase its liquidity reserves.

Quinn Thompson, chief investment officer at Wrecker Capital, said the decision is the first recent indication that Strategy understands investors’ concerns and is prepared to address them.

Mr. Thompson had asked the company to use common stock issuance to shore up cash and strengthen its balance sheet, rather than putting all of its new capital into Bitcoin. he said:

“This is exactly what we have been advocating: use the MSTR issuance to raise capital and strengthen our balance sheet.”

He added that the move supports preferred securities and other debt in excess of common stock in Strategy’s capital structure. It could also reduce the risk that companies will eventually have to sell Bitcoin to meet their obligations.

Mr. Thompson cautioned that Strategy still has work to do and additional common stock issuance could continue to put pressure on MSTR.

In fact, Strategy’s diluted share count has increased to approximately 388.6 million shares from 386.1 million a week ago, according to its latest filing. Year-to-date BTC yield, a corporate index that measures the change in Bitcoin holdings relative to diluted stock, fell to 11.8% from 13% four weeks ago.

This decrease reflects the cost of issuing common stock, with the majority of the proceeds going into cash rather than additional Bitcoin.

STRC recovers but pressure continues

STRC initially rallied above $91 following the reserve announcement, but closed Monday at $88.64. MSTR also rose in early market trading, but reversed and ended 2.7% lower at $109.52.

The move suggests that the cash increase has alleviated some of the near-term concerns without restoring STRC to a range where Strategy can safely resume issuing securities.

Bitwise Europe said forced liquidations by leveraged investors, rather than a sudden deterioration in Strategy’s ability to meet its obligations, contributed to the decline.

Nevertheless, the decline exposed investors’ concerns about preferred stocks’ sensitivity to Bitcoin prices, market liquidity, and interest rates. STRC has no expiry date and investors have no guarantee that it will return to $100.

Proponents argue that the discount itself could attract buyers because STRC’s $11.50 annual dividend represents a higher effective yield if the security trades below a stated price.

Samson Mo, CEO of Bitcoin company JAN3, described the feature as a “self-healing mechanism.” He said the strategy is avoiding new issuance of preferred stock below $100, but high yields and potential capital gains from an improving economy create incentives for buyers.

At a purchase price of $90, STRC’s annual dividend would be $11.50, for an effective yield of approximately 12.8%. If the stock returns to $100, investors would also receive an 11.1% capital gain.

This calculation assumes that the dividend remains unchanged and that STRC recovers within one year. No strategy is required to redeem shares at a set price.

Strategy CEO Von Leh said he bought $1 million in STRC during the decline and planned to hold the position until it hit $100, possibly longer.

The economic slowdown will also affect the Bitcoin market.

STRC’s status has implications beyond Strategy’s preferred shareholders, as this security funds the majority of the company’s Bitcoin purchases in 2026.

According to Bitwise estimates, the strategy has acquired approximately 174,300 Bitcoin this year. André Dragosch, head of research at Bitwise Europe, estimates that around 96,000 Bitcoins, or 55% of the total, were raised through STRC issuance. Most of the remainder was financed through the sale of common stock.

These purchases make Strategies one of the biggest sources of institutional demand for Bitcoin at a time when exchange-traded products around the world are recording net outflows.

Dragosh said the Strategic acquisition offset much of the negative institutional demand for Bitcoin investment products this year. Therefore, a prolonged decline in STRC could reduce purchases until preferred stocks recover, Strategy increases its dividend, or sovereign bond yields fall enough to make the securities competitive.

Notably, the company’s latest deal reflects that constraint. The strategy continued to buy Bitcoin, but only allocated about 10% of the funds raised that week to the cryptocurrency.

The purchase of 520 tokens was also significantly less than the 1,587 Bitcoin acquired a week ago.

The strategy maintains significant capital raising capacity. The company’s filings indicate approximately $25.4 billion is available under the MSTR issuance program and approximately $17.5 billion under the STRC program.

However, while the stock price is below $100, it is unlikely that STRC’s production capacity will be actively used.

Therefore, as long as common stock continues to trade at a sufficient premium to the value of Strategy’s assets, MSTR will be the company’s most immediate source of funding.

(Tag translation) Bitcoin