The surge in derivatives wiped out leveraged shorts

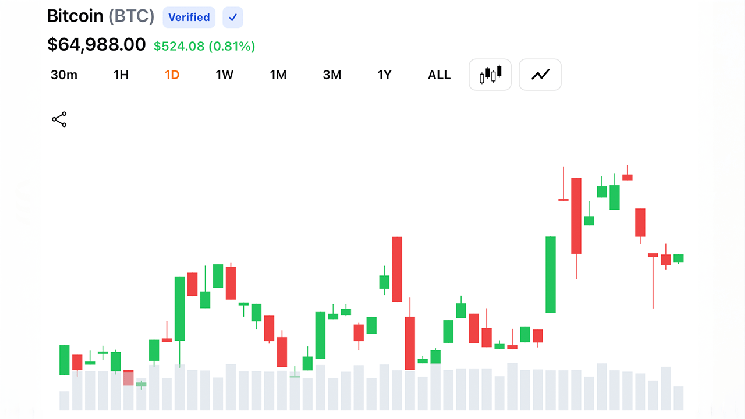

Building on the recovery that wiped out Monday’s losses, Bitcoin It comfortably passed the $65,000 threshold on Wednesday. This recent increase coincided with the release of US Producer Price Index (PPI) data. The unexpected 0.3% month-on-month deflation in the PPI surprised analysts, reflecting the release of the consumer price index (CPI) the previous day, although many had expected prices to remain flat.

Until the last test level was confirmed on June 22nd, the highest level was cryptocurrency I spent most of Tuesday evening and early Wednesday consolidating my money between $64,500 and $65,000. The deadlock was broken just after 8 a.m. ET, and a violent rally began. Bitcoin Intraday highs rose to $65,518. The stock then fell back to trade just above $64,800 as of 12:45 p.m. ET, securing a modest 24-hour gain.

BitcoinThe temporary increase of $65,500 pushed the market cap to over $1.3 trillion, an increase of about 10% since the beginning of the month. Nevertheless, the data also cryptocurrency It was still 3% below its June 16 price of about $67,000.

In the derivatives market, BitcoinThe price movement wiped out over $58 million in leveraged bets, with short positions accounting for nearly 85% of the total. Overall, the liquidation cryptocurrency The market reached $324 million, of which short bets accounted for $209 million.

The U.S. announcement comes as the ongoing clashes in the Middle East continue to make headlines since the beginning of this week. inflation Both CPI and PPI data appear to have given the market a much-needed boost. As both indexes fell, the probability that the Federal Reserve would raise interest rates at its next meeting fell to just 12% from more than 40% at the start of the week.

However, analysts caution that the data covers June and may not provide the most accurate picture, especially as reports and evidence of damage to critical oil infrastructure in the Middle East begin to emerge. Already, prices for Brent crude oil and West Texas Intermediate (WTI) have soared on higher prices, and this trend is expected to continue unless Washington and Tehran decide to give diplomacy another chance.

ETF inflows signal macro shift surrounding geopolitical noise

for BitcoinThe latest developments have failed to spark the panic seen in the early weeks of the war, at least according to Nansen research analyst Nikolai Sondergaard. Mr. Sondergaard focused on this point. Bitcoin The inflows into the Ether ETF on July 15 are clear evidence that Tuesday’s CPI results have significantly changed the near-term macroeconomic outlook. Headings were displayed in the report inflation Year-over-year growth slowed to 3.5% versus consensus 3.8%, and core inflation slowed to 2.6% versus 2.9% expected.

“DXY is trading near its lowest level in months at around 100.77, and the 10-year Treasury yield has fallen to 4.57% after briefly touching 4.61% before CPI. As a high-beta asset, this combination removes the near-term interest rate headwind that has been the dominant ceiling since May,” the analyst said.

From Sondergaard’s perspective, Nansen’s data shows that currency outflows are holding up despite geopolitical noise, meaning buyers are absorbing supply rather than retreating. “Headlines about the Iran blockade and the resulting oil surge, with WTI up about 14.6% in five days, did not change that pattern.”

Instead, Nansen analysts argue that on-chain data shows that the wallets that typically move the most in these settings initially are not migrating to stablecoins in a meaningful way. This is consistent with what was observed before the Middle East escalation, Sondergaard argues.

“Short-term leveraged longs are flushed and then accumulation resumes. Funding rates are currently hovering near zero. This removes the risk of an impending over-leveraged long and means we have a cleaner basis to work from if the next leg occurs,” Sondergaard explained.

The analyst also acknowledged that inflation and liquidity channels are playing more of a role here than the geopolitical hedging narrative. “MVRV is 1.205, with a realized price of about $53,000 and a long-term holder cost base of about $49,900, which defines the structural floor. This is not a market profile driven by geopolitical sentiment.”

For Sondergaard, the July 28 and 29 FOMC meetings are a real dual event. If CPI data holds and the Fed shows a reliable pivot path, conditions will once again be in place for sustained ETF inflows.